Sunday, January 19, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice week end.

Marc

Bentin

Bentinpartner GmbH

|

Global Chartbook PDF |

{kind=link}

Trend

Status Update

This year is starting like 2019

ended, in “melt up” mode. Bullish sentiment and possible excess was evidenced

last week by the lowest mutual funds’ cash allocation on record, a five-year

low in the US put-to-call ratio, NAAIM, AAII, Hulbert Sentiment, RYDEX

bull-to-bear ratio standing at their highest in history, speculative call

buying volume as a percentage of total NYSE volume also at its highest in

history, not to speak about the parabolic formation taking place in most of the Fangs where the FOMO (fear of missing out) expressed

itself best. Google joined the 1 trillion market cap on Thursday. On the other

side of the coin, “old economy” Alcoa stumbled 12% on weaker than expected

results and despite the company saying the order book for 2020 is

improving.

{kind=link}

The IIF reported a further (some would argue parabolic) rise global debt

to 322% of World GDP affecting household, corporate, government and financials across

both the DM and EM space, “spurred by low interest rates and loose financial

conditions”. US Economic data came out mostly stronger last week with retail

sales ex autos reporting a 0.7% monthly increase (climbing for the third

straight month) and December new home sales surging to a 13 year high on

Friday, up 16.9% annualized. It is not only low rates that are boosting sales

or a strong US job market (new openings dropped rather sharply last Friday however

following up to a weaker job report the week before), but looser mortgage

underwriting standards that eased considerably over the past two years. The

largest US originators are now offering jumbo mortgage loans of USD1mn with

only 10% down payment. Those who can bring a 30% down payment are able to

receive up to USD3mn in loans. No problem except that those loans could be the

prelude to jumbo problems later on…when things normalize which they may never

do, the more these excesses are allowed to accumulate. JPMorgan took note of

this state of affairs (excess positioning and optimism) last week already in

its Global Liquidity report and referred again over the week end to a “yellow

warning” signal but none of this seems actionable on a contrarian basis, just

yet, even if it suggests speculative excess behaviour fostered by the lack of

an immediate catalyst for a possible reversal. Talking about JPMorgan, the

company reported its most profitable year ever last week, propelled by consumer

borrowing and a rebound in investment banking (during the Sino/US phase I deal

signing ceremony at the White House on Wednesday, D. Trump asked JPM CEO J. Dimon to thank him for it). December industrial production data showed a

downturn, but that was largely blamed on a 5.6% decrease in utilities due to

the unseasonably warm winter weather.

Catalysts (for a setback) could later on come from Democrats’ Primaries

in February-March or Central Banks recognizing more frequently and openly (as Dallas

Fed President Kaplan hinted on Thursday) that their action now likely support and

fuels speculative excesses. The Fed is expected to trim its balance sheet,

albeit only slightly (after increasing it by USD400bn via repo’s) in the coming

months, but remains until now and for the most part still “anesthetized” or

“hypnotized”, held at gunpoint from Trump’s Twitter feed. Other major Central

Banks are in wait and see mode. As for geopolitical risks, nobody seems to care

about them and in particular not since Iran shot itself in the foot with the accidental

downing of a Ukrainian airliner.

Central Banks likely hold the key to support or diffuse the “melt up”

phase observed in financial markets today and in particular the excessive

leverage held by Hedge Funds.

Perhaps the best way to assess whether Central Banks do play a role in

what is happening is to look at how and why asset managers delivered their

performance last year. Asset managers were split in four categories:

·

The first one

was afraid of a repeat of 2018, of the inversion of the curve, of the collapse

in world trade and the likely upcoming recession. Those played it safe and

bought bonds and corporate bonds all the way to negative territory … They made

a killing last year and that is where the flows went last year for the most

part.

·

The second

category believed that Trump holds the holy grail of economic and central bank management

(and of stock markets manipulation), hanging over Trump’s highly manipulative Tweeter

feed. They somehow played it safe

(holding their nose and eyes closed), going and staying overweighed stocks…They

made a killing last year as well (or at least recovered their loss from 2018).

·

The third category

got really nervous about the risks of monetary disorder that might result from

massive “non-QE” liquidity injections. They played it safe as well, buying gold

and precious metals… They also made a killing last year.

·

The fourth

category was evenly split, weighing probabilities for the three scenarios above.

They bought bonds, stocks and precious metals, leveraging these three bets,

encouraged by historically low volatilities and presupposed diversification

benefits. Those included “risk parity” portfolios. And they made a killing “cubed”.

The very fact that all asset classes delivered an excellent performance all by themselves last year in

the aftermath of the Fed historic pivot (from tightening to easing in March),

whilst restarting “non-QE” balance sheet expansion, was a textbook illustration

of what monetary policy stimulus can do when pushed towards extremes; lifting

all boats indiscriminately. Their purchase brought bonds in the silly land of

negative yields, coupled to artificially compressed credit spreads, while stock

valuation rose well above their 30 year historic average, kickstarting a wave

of central bank buying in the metals markets, from those fearful of a

rekindling of inflation and those interested to de-anchor their economy away

from an increasingly weaponized USD.

Asking the question of the role of Central banks in what is happening is

answering it and it is up to them to decide what is next, considering that

animal spirits are wild and sometimes need to be tamed also to fulfil the

important Central bank responsibility of fostering long-term stability and

sustainability (inconsistent with melt up conditions).

The ongoing runaway rally in stocks is leading to a concentration of

wealth never seen before with 1% of the population now controlling 50% of the US equity market cap and 10% of the population controlling 90% of it

while the vast majority of the population held on to cash deposits yielding mediocre

to negative returns (they were also net sellers of stocks last year). Those holding

the short straw are the same ones that will suffer if/when pension funds

obligations start to be defaulted upon for lack of yield. In that case, the

only solution will be in the universal salary (and pension), printed out of

thin air… Structural issues should also be tackled like taming hedge funds

leverage (irrespective of the level of interest rates!), unless that is deemed inconsistent with a

smooth funding of a ballooning US fiscal deficit at the same time as foreign

appetite for US treasuries is dwindling. Forbidding share buybacks (which are

taking the blood out of public markets while increasing credit risk in the

system) is another measure that should be worth considering as a “non-monetary

policy” related decision as the maintenance of zero or sub zero rates has

ingrained in its DNA the forced evaporation of public markets (or its substitution

by toxic non-earning producing assets like most of the Unicorns) to the benefits

of more opaque private markets, only accessible to the happy fews.

The Eurostoxx50 gained 0,4% (1,9%), underperforming the S&P500 by

-1,5% although it did manage to close some of last week’s underperformance on

Friday on hopes that Trump will not follow through with a trade tariff

escalation with Europe that seems to have caved in to Trump’s blackmail regarding Iran. Or else it was because of Germany’s decision to

roll over an additional EUR30bn on infrastructure and climate change

investments, slowly opening the purse strings for useful purposes. VGK (VANGUARD FTSE EUROPE ETF) gained 1,5% (0,8%, Z-score 2,1).

Diversified EM equities (VWO) gained 1,4% (3,2%), underperforming the

S&P500 by -0,5%. RSX (VANECK RUSSIA ETF) rallied 2,2% (6,4%). ASHR

(XTRACKERS HARVEST CSI 300 CH) gained 1,1% (3,3%).

The Dollar DXY Index (UUP) rose 0,4% (1,3%) while the MSCI EM currency index

(measuring the performance of EM currencies vs. the USD) gained 0,1% (0,3%).

10Y US Treasuries were unchanged (-10bps) to 1,82%. 10Y Bunds dropped

-2bps (-3bps) to -0,22%. 10Y Italian BTPs underperformed rising 6bps (-4bps) to

1,38%, outperforming Bunds by -6bps. US consumer prices rose slightly in

December with the CPI accelerating 2.3% in 2019, the largest rise since 2011.

US High Yield (HY) Average Spread over Treasuries dropped -7bps (-16bps)

to 3,20%. US Investment Grade Average OAS dropped -3bps (1bps) to 1,02%. The rally in dubious high yield credit accelerated last week. While the amount of negatively yielding

securities declined further to a still whopping USD11.2trn (from >15trn last

year), the credit picture showed the nominal outstanding in BBB (last investment

graded bonds before switching to junk) rated debt securities kept increasing at

an accelerating pace. The credit spread between BB (best high yield) and BBB

(worst investment graded bonds) also shrank to its lowest level since 2006,

just prior to the great financial crisis. In European credit markets, EUR 5Y

Senior Financial Spread was unchanged (-1bps) to 0,51%. More than 60% of total

high yield issuance last week were corporate bonds from energy (shale) companies

with lower credit ratings.

{kind=link}

Gold dropped -0,3% (2,6%) while Silver dropped -0,4% (1,1%). Major Gold

Mines (GDX) dropped -0,1% (-2,9%). Up 34% since Christmas and climbing as much

as 10% Friday, Palladium went parabolic as well, reflecting how raw materials in shortage

act if both the demand and supply side are price inelastic (about 85% of

palladium ends up in cars’ exhaust systems, where it helps turn toxic

pollutants into less-harmful carbon dioxide and water vapor). Platinum was on

the move last week as well.

{kind=link}

Goldman Sachs Commodity Index dropped -0,8% (-2,1%). WTI Crude dropped

-0,8% (-4,1%).

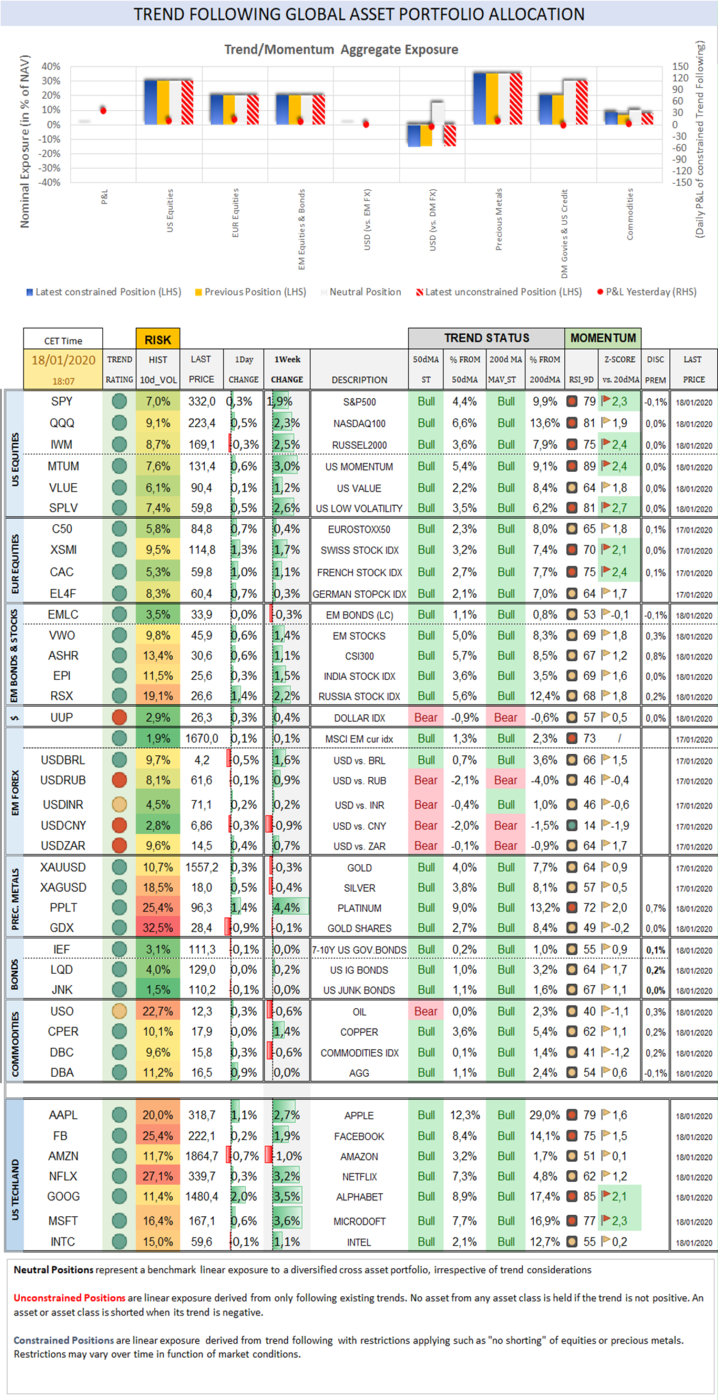

Trend Score Card

Click here for technical annotations.

{kind=link}

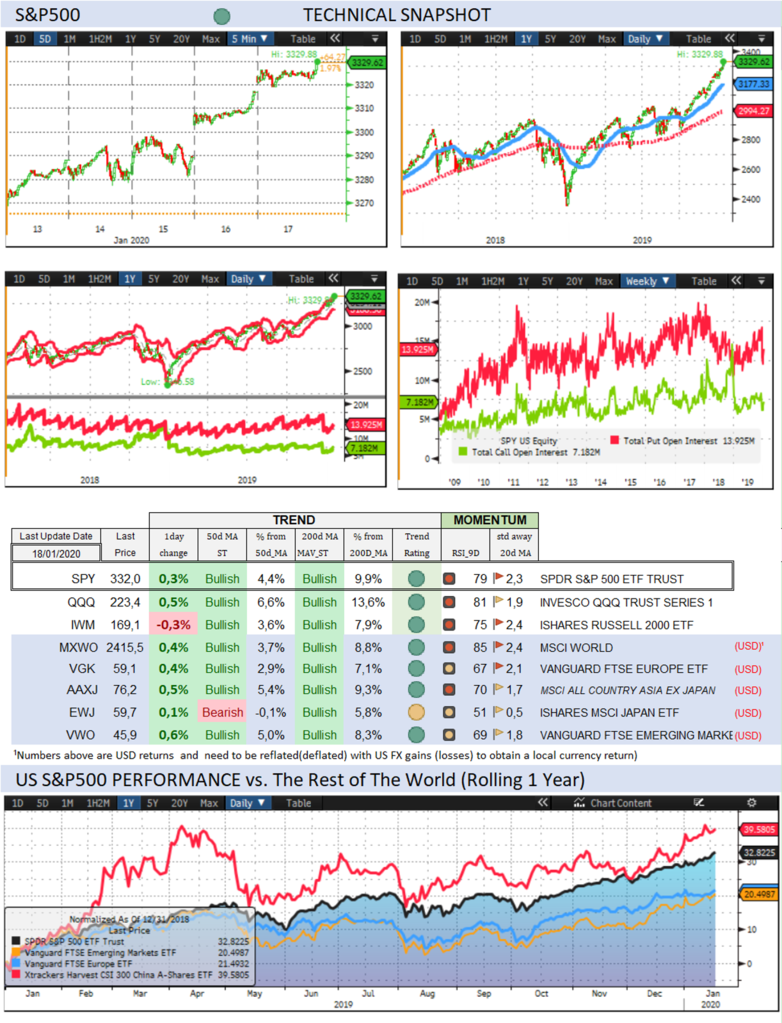

US

& International Equities

Check out US and International Stocks’ Technical

Trend Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and when

they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their

trend, expected Fed rate moves and speculative positioning in 10-year Treasury

Futures.

{kind=link}

US Recession

Risk Radar

A comprehensive list of

economic indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs. G7

and EM counterparts.

{kind=link}

Precious Metals

Check out where precious

metals stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and

futures traders’ sentiment (non-commercials open positions).

{kind=link}

Why Trend Following Matters and How It Can Help

You?

Trend following offers

guidance as to when to join and when to leave an asset class with changing

trend characteristics. A disciplined and rule-based trend following investment

approach can serve as an effective portfolio insurance technique. Our purpose,

beyond tracking economic, political and monetary developments is to assist

readers investing in global markets with a keen focus on trend formation

covering major asset classes.

To receive a Daily Trend

Status Update and round the clock market and economic instant messages, join a

free trial of our premium research.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery preferences:

https://www.bentinpartners.ch/subscribe

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the

recipient's sole use. Please do not forward it without prior authorization. It

is not intended as a recommendation, an offer or solicitation for the purchase

or sale of any security or underlying asset referenced herein or investment

advice. Investors should seek financial advice regarding the suitability of any

investment strategy based on their objectives, financial situation, investment

horizon and particular needs. This report does not include information tailored

to any particular investor. It has been prepared without any regard to the

specific investment objectives, financial situation or particular needs of any

person who receives this report. Accordingly, the opinions discussed in

this Report may not be suitable for all investors. You should not consider any

of the content in this report as legal, tax or financial advice. The data and

analysis contained herein are provided "as is" and without warranty

of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss

sustained by anyone who has relied on the information contained in any

publication published by BentinPartner llc. The content and views expressed in this report

represents the opinions of Marc Bentin and should not be construed as

guarantee of performance with respect to any referenced sector. We remind you

that past performance is not necessarily indicative of future

results. Although BentinPartner llc believes the information and content included in

this report have been obtained from sources considered reliable,

no representation or warranty, express or implied, is provided in relation to

the accuracy, completeness or reliability of such information. This Report is

also not intended to be a complete statement or summary of the industries,

markets or developments referred to in the Report.

#fx #forex

#investing #markets #riskmanagement #bankingindustry #finances #money #traders #quants