Monday, May 04, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice week end.

Marc

Bentin

Bentinpartner

GmbH

{kind=link}

{kind=link}

Trend

Status Update

“In terms of fiscal concern…, for many years, I've

been, before the Fed, I have long time been an advocate for the need for the

United States to return to a sustainable path from a fiscal perspective at the

federal level. We have not been on such a path for some time which just means

that the debt is growing faster than the economy. This is not the time to act

on those concerns. This is the time to use the great fiscal power of the United

States to do what we can to support the economy and try to get through this

with as little damage to the longer run productive capacity of the economy as

possible. The time will come, again, and reasonably soon, I think, where we can

think about a long-term way to get our fiscal house in order. And we absolutely

need to do that. But this is not the time to be, in my personal view, this is

not the time to let that concern, which is a very serious concern, but to let

that get in the way of us winning this battle…”

Chances are that there is no turning back on this monetary stimulus and

that the normalisation will be replaced by something else… Congress is also and

already evaluating the opportunity of another USD1trn stimulus.

A former President of the Federal Reserve Bank of Minneapolis, N.

Kocherlatoka was interviewed last week by Tom Keene (Bloomberg) and said he was

favouring negative interest rates for the Fed making some other (and more) jaw

dropping observations;

“One of the

roles of economists like myself that are in academia … is to really try to push

us into a much better place. I really believe that fifty years from now people

are going to look back – economists are going to look back – at the existence

of cash much like we look back at the gold standard. We look back at the gold

standard as a period which really hamstrung monetary policy and created huge

amounts of unemployment as a result during the Great Depression. People are

going to look back at the existence of cash and the zero lower bound – the

inability to go much below zero with interest rates – in the same way,

hamstringing the ability of central banks to provide sufficient support to the

economy – and thereby creating excessive unemployment and robbing people of

their jobs.”

I do not know what he wants to replace cash with (bitcoins?) but I

thought the quote to be quite insightful.

Last week, the ECB also expanded its loans to banks saying it would lend

money to banks at rates as low as minus 1% through a planned programme and launched

a separate round of fresh lending. The ECB’s governing council said it was

‘fully prepared’ to increase the size of its recently launched €750bn pandemic

emergency purchase programme and to ‘adjust its composition, by as much as

necessary and for as long as needed’.”

In Japan, “The Bank of Japan… ramped up risky asset purchases and

pledged to buy unlimited amounts of government bonds to combat the economic

fallout from the coronavirus epidemic. At the rate review, the central bank

pledged to accelerate purchases of corporate bonds and commercial paper until

the combined balance of its holdings reaches 20 trillion yen ($186bn). It also

pledged to aggressively buy government bonds to keep the yield curve low in a

stable manner.” The FT wrote a comprehensive article asking the question of debt sustainability (which is a bit too theoretical when interest

rates are set to be anchored at 0% or below for years to come). Foreign policy also reviewed the Japanese fiscal situation in an

article (dating from two weeks ago), that should get traders inclined to believe

JPY is a genuine safe haven currency, puzzled.

Among the risks that resurfaced last week (beyond the fact that WHO

warned that it was possible to be infected twice by Covid19 which reduced the

interest of establishing certificates of immunity), was D. Trump saying… his

hard-fought trade deal with China was now of secondary importance to the

coronavirus pandemic as he threatened new tariffs on Beijing. Trump’s sharpened

rhetoric against China reflected his growing frustration with Beijing over the

pandemic… Two U.S. officials… said a range of options against China were under

discussion. Reuters also reported that D. Trump said… he was confident the

coronavirus may have originated in a Chinese virology lab, ratcheting up

tensions with Beijing over the origins of the deadly outbreak.

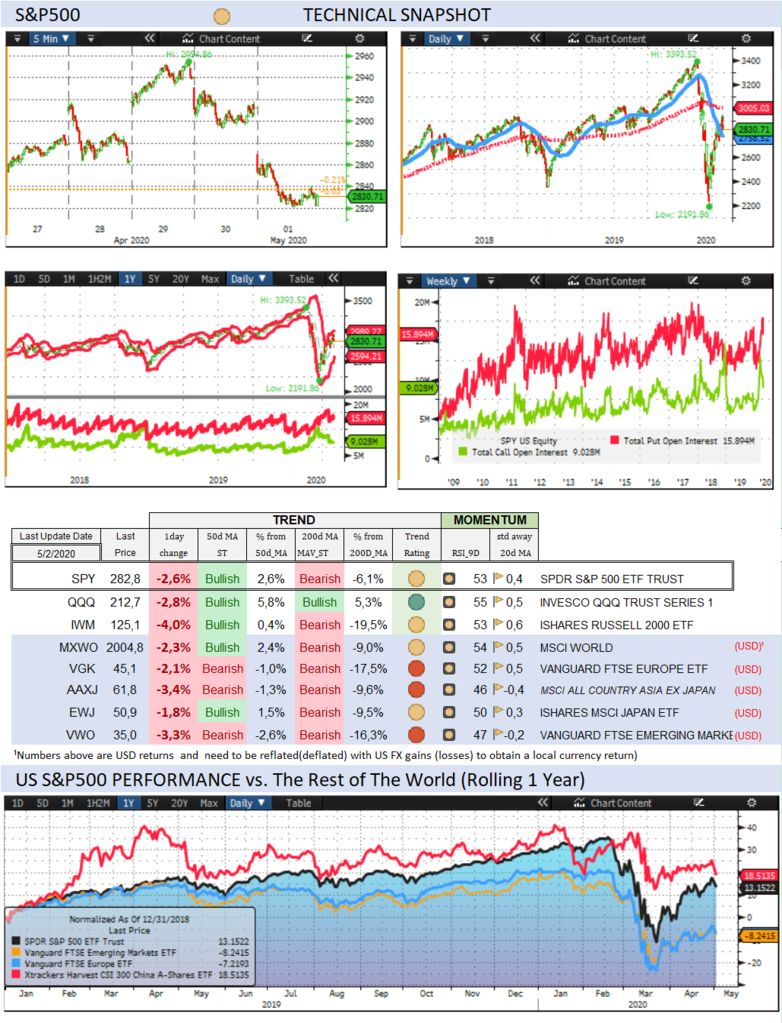

Over the past week, the S&P500 dropped -0,1% (-12,1% YTD) while the

Nasdaq100 dropped -0,5% (0,1% YTD). The US small cap index rallied 2,2% (-24,5%

YTD).

CBOE Volatility Index rallied 3,5% (169,9% YTD) to 37,19.

The Eurostoxx50 rallied 2,7% (-21,4%), outperforming the S&P500 by

2,7%.

Diversified EM equities (VWO) dropped -0,4% (-21,4%), outperforming the

S&P500 by -0,3%. The tech picture became more blurred; AAPL rallied 2,2%

(-1,6%). FB rallied 6,4% (-1,5%). LYFT

sold off by -7,4% (-31,2%). AMZN sold off by -5,2% (23,7%).

NFLX sold off by -2,3% (28,3%). GOOG rallied 3,2% (-1,2%). MSFT was unchanged

(10,7%). INTC sold off by -3,0% (-4,0%).

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies dropped -1,3% (3,3%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) gained 0,9% (-5,8%).

The euro was mostly stronger. EURUSD gained 1,5% (-2,1%) EURCHF gained

0,2% (-2,8%). EURJPY gained 0,8% (-3,6%). EURGBP gained 0,3% (3,8%).

10Y US Treasuries dropped 1bps (-131bps) to 0,61%. 10Y Bunds dropped

-11bps (-40bps) to -0,59%. 10Y Italian BTPs rallied -8bps (35bps) to 1,76%,

outperforming Bunds by 0bps.

US High Yield (HY) Average Spread over Treasuries dropped -30bps

(409bps) to 7,45%. US Investment Grade Average OAS dropped -1bps (105bps) to

2,06%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -5bps

(52bps) to 1,04%.

Gold dropped -1,7% (12,1%) while Silver dropped -1,8% (-16,1%). Major

Gold Mines (GDX) dropped -1,9% (13,7%).

Goldman Sachs Commodity Index gained 4,3% (-45,4%). WTI Crude rallied

16,8% (-67,6%). The Saudi Arabian Monetary Authority’s net foreign assets

dropped by 100bn riyals ($27bn) in March to SAR465bn, the lowest levels since

2011 and the fastest decline in two decades, the FT reported.

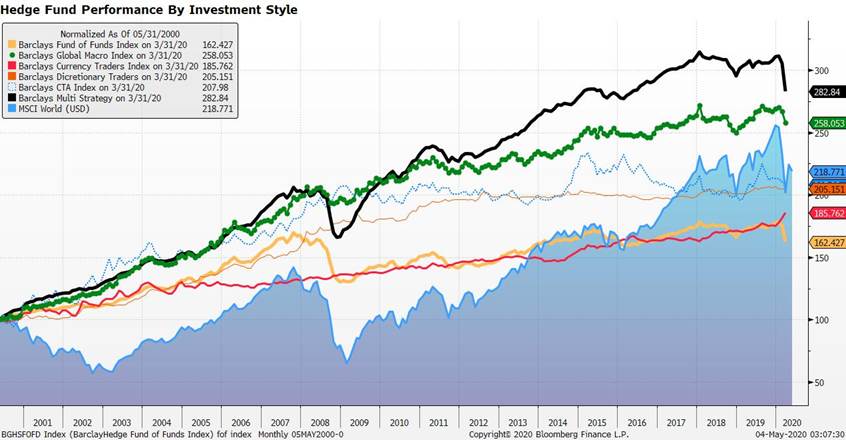

Hedge funds’ April results still need to be posted for April but up to March,

currency and macro funds were reported to be doing relatively well given the

circumstances and could well remain the place to be in this space for the next

few quarters.

Over the week end…

W. Buffet initiated a turnaround on a previous call, announcing over the

week end that he had sold his stakes in all US airlines; “I don’t know if two or three years from now if

as many people will fly as many passenger miles as they did last year,” he

said. “If the business comes back 70 or 80 per cent, the aircraft doesn’t

disappear. You've got too many planes.” Mr Buffett also said that he had

decided against lending large sums as he did during the depths of the financial

crisis because Berkshire was not finding enticing opportunities.” This is bad

omen for the transport sector today which more often than not tend to lead the

rest of the tape (Dow Theory). He also considers he is no competition to outbid

the Fed in supporting credit markets (not at that price…).

S&P500 futures -25 points; Hang Seng -3.5%; Japan closed

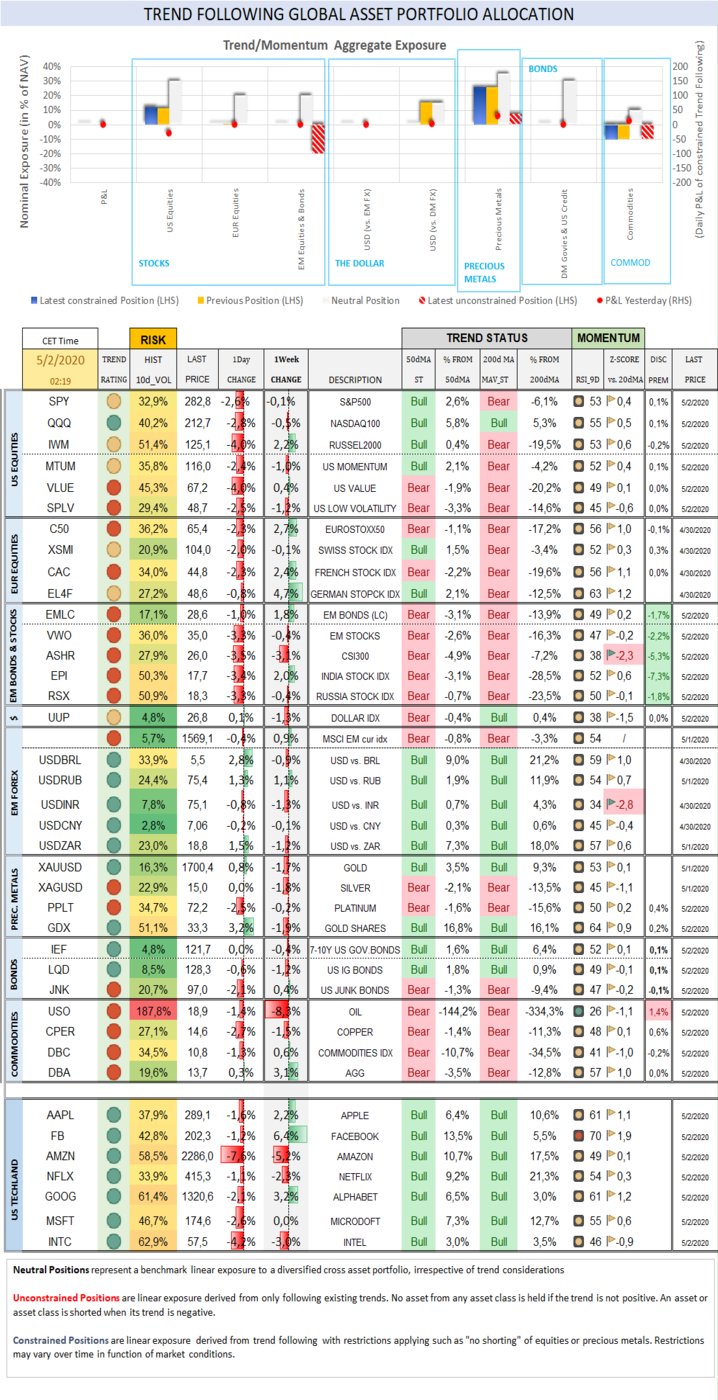

Trend Score Card

Click here for

technical annotations.

{kind=link}

US

& International Equities

Check out US and International Stocks’ Technical Trend

Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and

when they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their trend,

expected Fed rate moves and speculative positioning in 10-year Treasury Futures.

{kind=link}

US Recession

Risk Radar

A comprehensive list of economic

indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs. G7 and EM counterparts.

{kind=link}

Precious Metals

Check out where precious metals

stand Trendwise and Breakoutwise. Get a sense of options (cumulative

open interests on calls and puts) and futures traders’ sentiment (non-commercials

open positions).

{kind=link}

Check out how precious metals, the dollar and the Stock

market correlate with each other and speculative futures positioning on

Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and

rule-based trend following investment approach can serve as an effective

portfolio insurance technique.

To receive a Daily Trend Status

Update and round the clock market and economic instant notifications, join the

free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery

preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio Management and Advisory Services

BentinPartner GmbH is a Swiss registered

independent financial adviser. We offer four different portfolio management

mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an

optimized strategic benchmark. This allocation delivers the “beta” (or markets

related) performance of your portfolio while we seek to generate additional

“alpha” (“skills related) performance with tactical adjustments, using a

predefined maximum “value at risk” envelope. Most of the portfolio’s

performance is derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or

benchmark) and pursues a “total” as opposed to “relative” return objective.

With this mandate, we seek to beat the best of “cash” or of the MSCI World

Equity index, applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage

(not exceeding 100% of NAV). You control the portfolio allocation (which can be

a pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at +41615444310.

We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the list,

please send us an email by clicking here, mentioning “unsubscribe” in

the title.

To ensure that our emails reach

your inbox and not your spam folder, please consider adding Marc.Bentin@BentinPartner.ch,

Marc.Bentin@BentinPartners.ch and our alternate address Bentinpartner@gmail.com

to your safe address book. If you are using Microsoft Outlook, simply right

click on our email address, choose "add to Outlook contacts" and then

"save".

Important Disclaimer

© Copyright by BentinPartner llc. This communication is provided for information

purposes only and for the recipient's sole use. Please do not forward it

without prior authorization. It is not intended as a recommendation, an offer

or solicitation for the purchase or sale of any security or underlying asset

referenced herein or investment advice. Investors should seek financial advice

regarding the suitability of any investment strategy based on their objectives,

financial situation, investment horizon and particular needs. This report does

not include information tailored to any particular investor. It has been

prepared without any regard to the specific investment objectives, financial

situation or particular needs of any person who receives this report. Accordingly,

the opinions discussed in this Report may not be suitable for all

investors. You should not consider any of the content in this report as legal,

tax or financial advice. The data and analysis contained herein are provided "as

is" and without warranty of any kind. BentinPartner llc, its employees, or

any third party shall not have any liability for any loss sustained by anyone

who has relied on the information contained in any publication published by

BentinPartner llc. The content and views expressed in this report represents

the opinions of Marc Bentin and should not be construed as guarantee

of performance with respect to any referenced sector. We remind you that past

performance is not necessarily indicative of future results. Although

BentinPartner llc believes the information and content included in

this report have been obtained from sources considered reliable,

no representation or warranty, express or implied, is provided in relation to

the accuracy, completeness or reliability of such information. This Report is

also not intended to be a complete statement or summary of the industries,

markets or developments referred to in the Report.

#fx #forex #investing #markets #riskmanagement

#bankingindustry #finances #money #traders #quants