Monday, May 11, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Please

not that we are introducing a revamped Chartbook report.

Have

a good week.

Marc

Bentin

Bentinpartner

GmbH

{kind=link}

{kind=link}

Trend

Status Update

We do not know what kind of letter shaped recovery, the deconfinement

will bring. What we do know is that things will not return to normal. They will

return to a to a new normal, at best. People will be zooming, netflixing,

hopefully walking, running, cycling, golfing maybe. They will most certainly go

into a shopping spree (as a revenge against the confinement). But who is going

to enjoy packed restaurants, planes or movie theatres? Most likely, way less

people than before.

Transporting (not traveling) was already an unpleasant experience in

many ways and things will only get worse. Take off your shoes, your belts, your

liquids... add to that the risk of being taken aside for a cold...wearing a

mask next to a sneezing fellow traveller and you’ll get a really unpleasant and

stressful experience that you will want to avoid. Furthermore, who is going to

want to return to floating cities for a cruise running the risk of staying

trapped for days and weeks? Not all these floating cities will be turned into

museums...and that is a good thing perhaps. After all, there were part of a big

ecological disaster.

Still, industries centred on tourism, hospitality and leisure (accounting

for 7.7mn job losses) are only supported at arms’ strength by governments and likely

not forever.

That is probably why W. Buffet stunned investors early last week, saying

he had turned tail on his four US airlines investments. This only plumbed the

market for one day before investors decided that this also shall pass.

There will be positive consequences like less pollution, an acceleration

of technological adoption but many job losses will turn permanent and things

might not play out as smoothly in the end as markets are keen to believe (Goldman

still believes lows will be revisited on the S&P500). Still, it took courage and

fortitude that we have been missing to fight this bulldozer of a rally last,

not least because it is also fuelled by hopes, expectations and rising odds of

the Fed going negative (on rates) before the end of the year.

This provided some comfort to succumb to the sirens of Tina last week… Fed

Chair Powell will speak on Wednesday and will be scrutinized for his stance on

negative interest rates which he has systematically so far rejected.

If the Fed pursues to bail out everything that can go down (its balance

sheet is set to treble from pre-corona outbreak) and if the US Treasury

abandons any sense of fiscal restraint on expectations that all new debt will

be monetized (a thinking gaining in popularity in certain countries of Europe

as well), there is not one single chance that we are not heading into a

currency crisis of some sort with serious inflation consequences down the road.

Germany will continue to play the adult in the room (see decision of the

Constitution court last week questioning the legality of the different QE

programs) and prevent excessive debt monetisation in Europe. But the Fed and

Treasury are going all in (either because they naively believe the dollar is

iron clad or because they do not mind dragging it down) and we think that the

odds are now high that the dollar will go down fairly significantly in a not

too distant future.

The best way to prepare is to hold large strategic overweighs on

precious metals (in conjunction with tactical long equity positioning in

Europe) held in gold and increasingly, in silver as well. We will never be able

to buy a bitcoin…

The European court of justice recalled last week that the ECB is

submitted to the European court of justice that supersedes the German court of

justice and the French Finance Minister and BdF Governor vociferously reminded this

last week. Still, if the German Court of Justice does not change its stance in

three months, in theory the Bundesbank might be forced to stop buying German

debt, leaving this mission to the BdF and other European central banks to buy

negatively yielding German bonds...

So, the ECB has got some PR and convincing work to do, and politicians

from de-complexed overindebted, ever-profligate and lecturing European nations

as well. Otherwise, the sacred unity will be broken and in the worst case,

infinitesimally small Gerxit probabilities could even resurface.

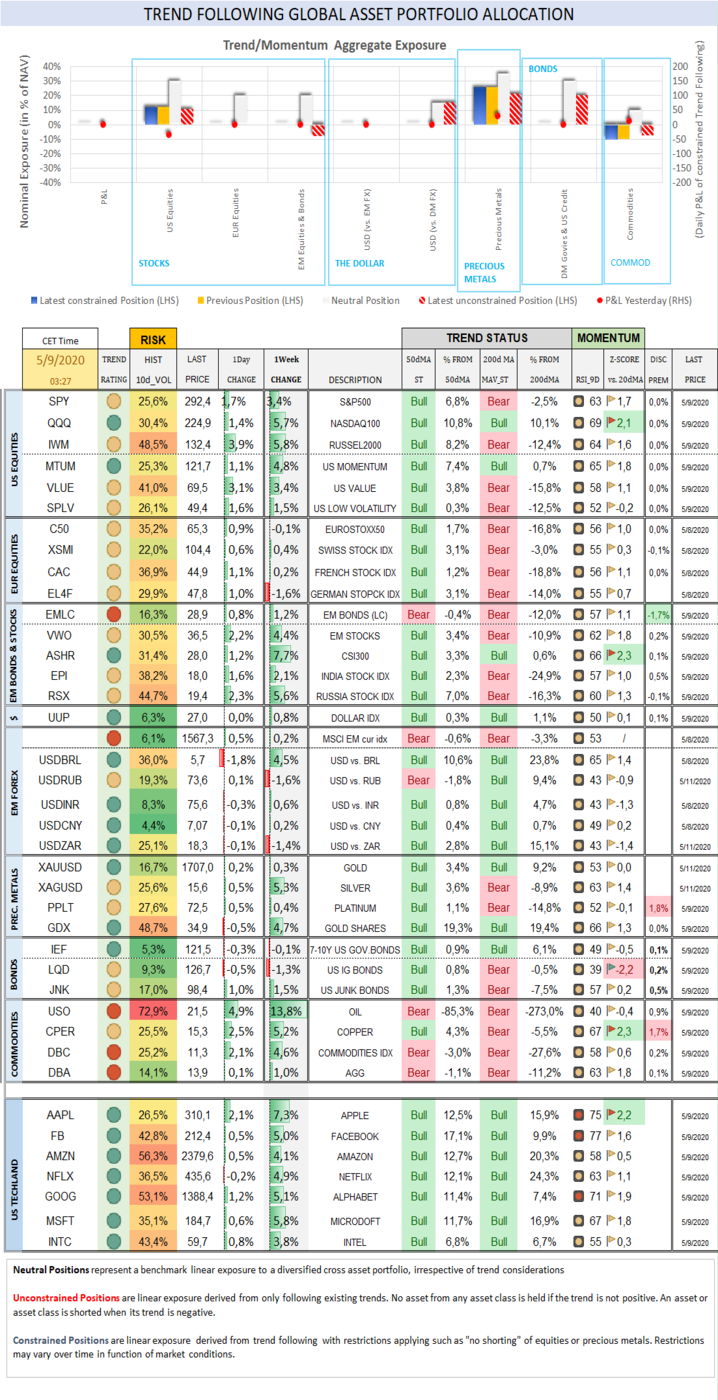

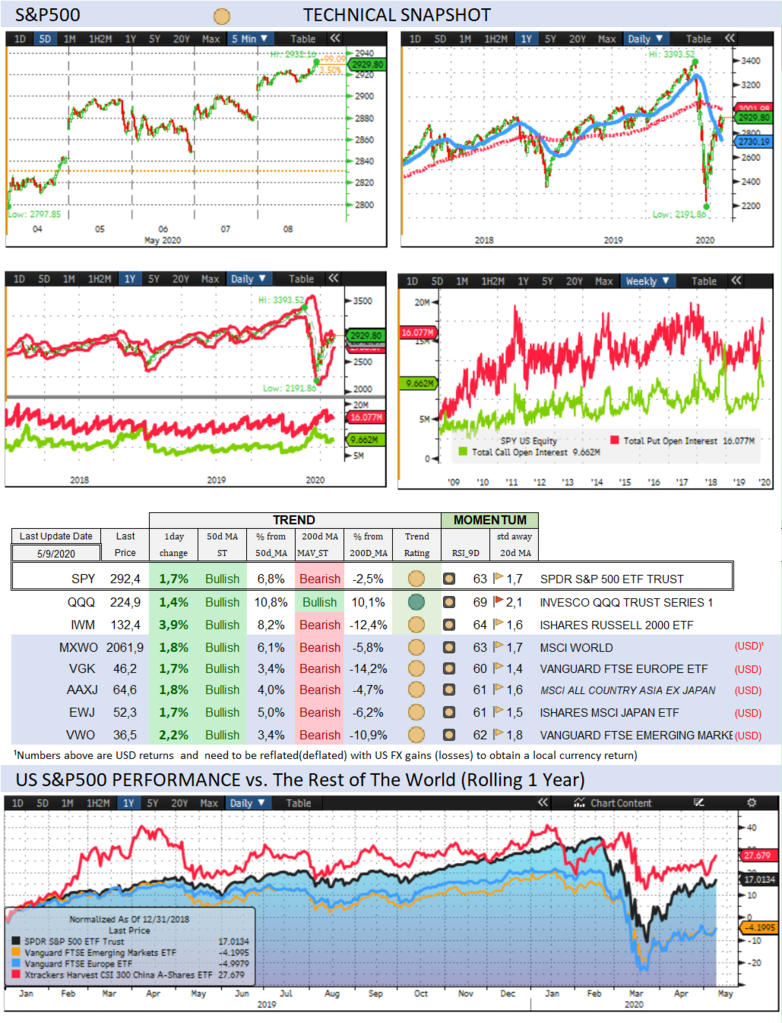

Over the past week, the S&P500 rallied 3,4% (-9,1% YTD) while the Nasdaq100 rallied 5,7% (5,8%

YTD, Z-score 2,1). The US small cap index rallied 5,8% (-20,1% YTD).

Cboe Volatility Index sold off by -24,8% (103,0% YTD) to 27,98.

The Eurostoxx50 dropped -0,1% (-21,5%), underperforming the S&P500

by-3,5%.

Diversified EM equities (VWO) rallied 4,4% (-17,9%), outperforming the

S&P500 by 1,0%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies gained 0,8% (4,1%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) gained 0,2% (-5,9%).

10Y US Treasuries underperformed with yields rising 6bps (-122bps) to

0,70%. 10Y Bunds climbed 5bps (-35bps) to -0,54%. 10Y Italian BTPs

underperformed rising 8bps (43bps) to 1,85%.

US High Yield (HY) Average Spread over Treasuries dropped -20bps (389bps)

to 7,25%. US Investment

Grade Average OAS climbed 10bps (115bps, Z-score 2,3) to 2,16%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -3bps

(53bps) to 1,05%.

Gold gained 0,3% (12,5%) while Silver rallied 5,3% (-12,9%). Major Gold

Mines (GDX) rallied 4,7% (19,1%). The argumentation of the bull case for silver

(in absolute and relative terms to its big brother gold) became more compelling

and was presented convincingly in this ZH article. Gold is technically in bull trend and supported

by solid fundamentals (the grandest global monetary experiment of all times,

negative real rates, soaring deficits, stable gold production, strong central

bank and soaring investment (etf) demand. However, a Gold/ silver ratio over

100 (120 now) has only been that high, going into historical recessions such as

the invasion of Poland by the Nazis, the great depression, or the 2008

financial crisis. We might be at a similar juncture... but in each and every

case, the gold/silver ratio ebbed back significantly from those peaks and stocks

are not pricing an Armageddon scenario for now. The risk of an engineered and

seasonal gold take-down of gold ahead of the futures settlement (to reduce or

prevent delivery) remains a possibility…but it will be bought. Bitcoin rallied

last Thursday after Paul Tudor Jones suggested it might keep pushing

higher.

Goldman Sachs Commodity Index rallied 6,5% (-41,3%). WTI Crude rallied

17,7% (-60,7%).

Over the week end…

Nikkei +1.4%; CSI300 +0.4%; S&P500 future +10 points

Stocks climbed in Asia this morning, recouping some early losses in thin

volumes.

The PBOC pledged more help to counter the virus impact in China. U.S. VP

Mike Pence is self-isolating away from the White House after an aide tested

positive.

Regional Federal Reserve Presidents J. Bullard, J. Mester and P. Harker are due to speak at

events on Tuesday.

Trend Score Card

Click here for

technical annotations.

{kind=link}

US

& International Equities

Check out US and International Stocks’ Technical Trend

Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and

when they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their trend,

expected Fed rate moves and speculative positioning in 10-year Treasury Futures.

{kind=link}

US

Recession Risk Radar

A comprehensive list of economic

indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs. G7 and EM counterparts.

{kind=link}

Precious Metals

Check out where precious metals

stand Trendwise and Breakoutwise. Get a sense of options

(cumulative open interests on calls and puts) and futures traders’ sentiment

(non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the Stock

market correlate with each other and speculative futures positioning on

Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and

rule-based trend following investment approach can serve as an effective

portfolio insurance technique.

To receive a Daily Trend Status

Update and round the clock market and economic instant notifications, join the

free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery

preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio Management and Advisory Services

BentinPartner GmbH is a Swiss registered

independent financial adviser. We offer four different portfolio management

mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an

optimized strategic benchmark. This allocation delivers the “beta” (or markets

related) performance of your portfolio while we seek to generate additional

“alpha” (“skills related) performance with tactical adjustments, using a

predefined maximum “value at risk” envelope. Most of the portfolio’s

performance is derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or

benchmark) and pursues a “total” as opposed to “relative” return objective.

With this mandate, we seek to beat the best of “cash” or of the MSCI World

Equity index, applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage

(not exceeding 100% of NAV). You control the portfolio allocation (which can be

a pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at +41615444310.

We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the list,

please send us an email by clicking here, mentioning “unsubscribe” in

the title.

To ensure that our emails reach

your inbox and not your spam folder, please consider adding Marc.Bentin@BentinPartner.ch,

Marc.Bentin@BentinPartners.ch and our alternate address Bentinpartner@gmail.com

to your safe address book. If you are using Microsoft Outlook, simply right

click on our email address, choose "add to Outlook contacts" and then

"save".

Important Disclaimer

© Copyright by BentinPartner llc. This communication is provided for

information purposes only and for the recipient's sole use. Please do not

forward it without prior authorization. It is not intended as a recommendation,

an offer or solicitation for the purchase or sale of any security or underlying

asset referenced herein or investment advice. Investors should seek financial

advice regarding the suitability of any investment strategy based on their

objectives, financial situation, investment horizon and particular needs. This

report does not include information tailored to any particular investor.

It has been prepared without any regard to the specific investment objectives,

financial situation or particular needs of any person who receives this report.

Accordingly, the opinions discussed in this Report may not be suitable for

all investors. You should not consider any of the content in this report as

legal, tax or financial advice. The data and analysis contained herein are

provided "as is" and without warranty of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss sustained

by anyone who has relied on the information contained in any publication

published by BentinPartner llc. The content and views expressed in this report represents

the opinions of Marc Bentin and should not be construed as guarantee

of performance with respect to any referenced sector. We remind you that past

performance is not necessarily indicative of future results. Although BentinPartner llc

believes the information and content included in this report have

been obtained from sources considered reliable, no representation or

warranty, express or implied, is provided in relation to the accuracy,

completeness or reliability of such information. This Report is also not

intended to be a complete statement or summary of the industries, markets or

developments referred to in the Report.

#fx #forex #investing #markets

#riskmanagement #bankingindustry #finances #money #traders #quants