Monday, June 22, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a good week.

Marc

Bentin

Bentinpartner

GmbH

{kind=link}

{kind=link}

Trend

Status Update

The sudden

(post covid) emergence of 10mn new day traders now active on the Robinhood

platform was best illustrated this month by traders driving the share price of Herz to treble from the moment the company had filed for

bankruptcy. While a judge had initially authorized the transaction, it only

took a late realisation by the SEC that issuing USD1bn worth of fresh equity to

quench the thirst of those traders would likely fail at providing the necessary

level of investor protection for the operation to be approved without asking

further questions. Last week brought another example of herd investing from

Robinhooders after a call to “Buy Black” (a legitimate pursuit if any) gapped

the price of a black community savings bank, Carver Bank, 7 times higher last Thursday, on 60mn shares exchanged (vs. a

previous daily average of 5k). This is reflective of a new power emerging on

Wall Street. It does not mean that these investors will not ultimately be

thrown off the road as the whole situation is also reminiscent of the

speculative excesses of day traders observed at the height of the internet

bubble. One of the influencers operating from Robinhood who, for his discharge,

claims he has no investment background and should not be followed …still has

got 1.5mn followers.

{kind=link}

{kind=link}

Lat week initial equity markets’ push came from Fed Chair Powell

testimony to Congress where he dampened the outlook for the US economy,

encouraged more fiscal support and hinted that he would be supportive of capping

yield levels, if necessary. On Monday the Fed also launched its “Main Street

Lending Program” whereby the Fed will offer up to USD600bn in loans to

companies that were in a good shape before the pandemic but now need financing

to continue their operation. Stronger

than expected US retails sales were the good economic news considered as such

as was the USD1trn fiscal infrastructure plan supported by D. Trump. Last

week’s jobless claims were however disappointing and more veteran investors

such as J. Grantham (“Uncertainty has seldom been higher”) or Howard Marks (“The Anatomy of a rally”) argued that the market is driven by Fomo and

liquidity despite the prospect of a sharp deterioration in earnings and a 15 to

20% decline in Q2 GDP. Retail investors (who are on the receiving end of

government benefits checks) are seemingly playing a major role driving equity

markets ever higher.

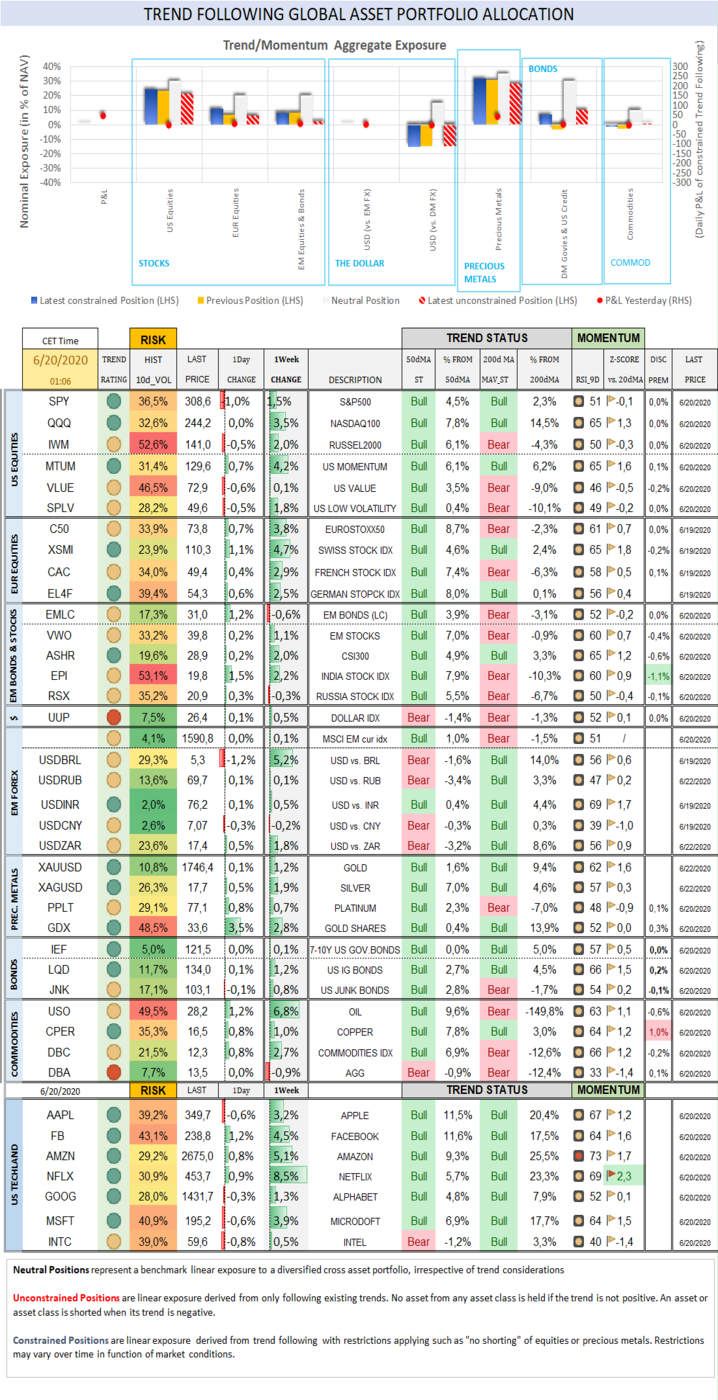

Over the past week, the S&P500 gained 1,5% (-4,1% YTD) while the

Nasdaq100 rallied 3,5% (14,9% YTD). The US small cap index gained 2,0% (-14,9%

YTD). XBI (SPDR S&P

BIOTECH ETF) rallied 8,6% (14,4%, Z-score 2,4).

Cboe Volatility Index sold off by -2,7% (154,9% YTD) to 35,12.

The Eurostoxx50 rallied 3,8% (-11,3%), outperforming the S&P500 by

2,3%.

Diversified EM equities (VWO) gained 1,1% (-10,5%), underperforming the

S&P500 by-0,4%. The Dollar DXY Index (UUP) measuring the USD performance

vs. other G7 currencies recouped 0,5% (1,6%) while the MSCI EM currency index

(measuring the performance of EM currencies vs. the USD) gained 0,1% (-4,5%).

Speculative traders, as reported by last Friday’s COT report, turned bearish on the USD for the first time since 2018. Chances are that

the drawdown imposed on dollar bears since last week’s COT report “cut off”

(dating from Tuesday evening) time reduced speculative dollar bearishness

somewhat intraweek but it remains that sentiment turned negative on the dollar

(and we are adamant about forthcoming dollar weakness as well).

{kind=link}

10Y US Treasuries rallied -1bps (-122bps) to 0,69%. 10Y Bunds climbed

2bps (-23bps) to -0,42%. 10Y Italian BTPs rallied -9bps (-6bps) to 1,36%,

outperforming Bunds by -1bps.

US High Yield (HY) Average Spread over Treasuries dropped -33bps

(242bps) to 5,78%. US Investment Grade Average OAS dropped -14bps (49bps) to

1,50%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -6bps

(24bps) to 0,76%.

Gold gained 1,2% (15,1%) while Silver gained 1,9% (-0,8%). Major Gold

Mines (GDX) rallied 2,8% (14,6%). Goldman revised its forecast for Gold to

USD2’000 for the next year.

Goldman Sachs Commodity Index rallied 3,3% (-31,8%). WTI Crude rallied

6,7% (-35,1%).

Over the week end….

Ø China announced the details of its security law

that will override Hong Kong’s legal system, also setting up a new security

building in Hong Kong.

Ø As Russians prepare to vote sweeping changes to the

nation’s constitution, V. Putin said he’ll consider running for a fifth

presidential term in 2024 if the necessary amendment to the constitution are

approved on July 1st.

Ø US futures gapped 1% lower overnight following the

week end news of a revival in covid cases (including in Tusla where D. Trump

held a meeting on Saturday that drew less attendees than expected) but the dip

was bought and it is now trading +0.5% higher along with gold while silver

gained +1.5% as risk appetite remains boxed in between second waves and the Fed

going all in.

Trend Score Card

Click here for

technical terminology.

{kind=link}

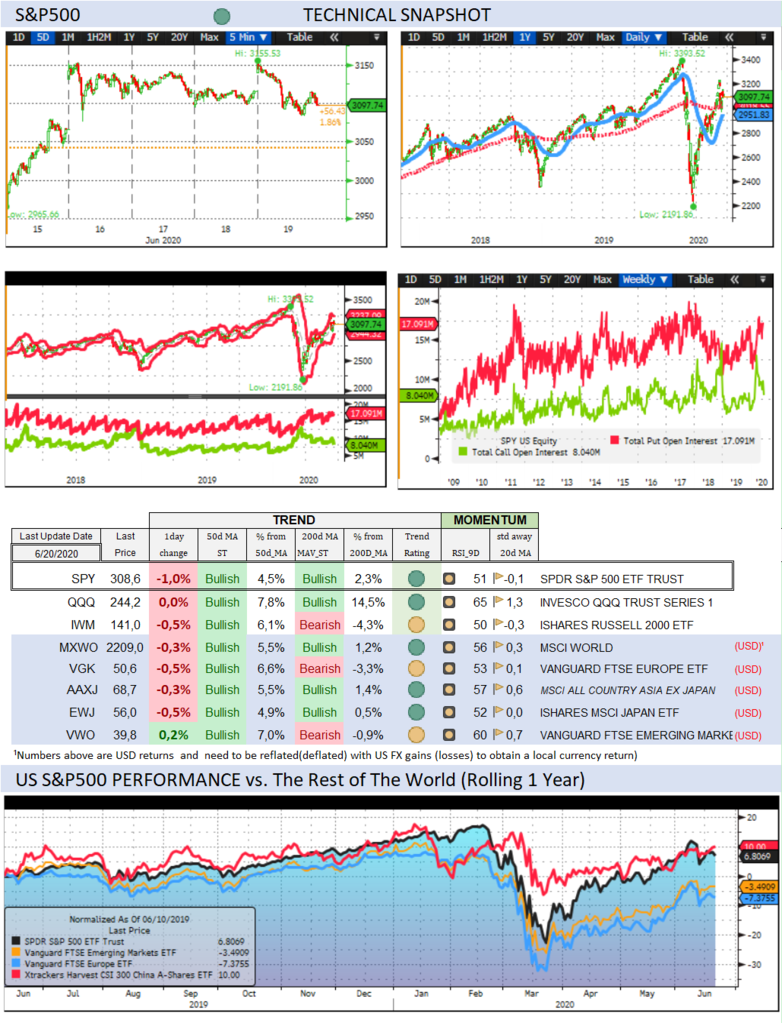

US

& International Equities

Check out US and International Stocks’ Technical

Trend Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and when

they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their

trend, expected Fed rate moves and speculative positioning in 10-year Treasury

Futures.

{kind=link}

US Recession

Risk Radar

A comprehensive list of

economic indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs. G7 and EM counterparts.

{kind=link}

Get the Score card of all major currency pairs in terms

of Trend, Momentum, Carry, GDP and Current account differential

Precious Metals

Check out where precious

metals stand Trendwise and Breakoutwise. Get a sense of options

(cumulative open interests on calls and puts) and futures traders’ sentiment

(non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the

Stock market correlate with each other and speculative futures positioning

on Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and rule-based

trend following investment approach can serve as an effective portfolio

insurance technique.

To receive a Daily Trend

Status Update and round the clock market and economic instant notifications, join the

free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio Management and Advisory Services

BentinPartner GmbH is a Swiss registered

independent financial adviser. We offer four different portfolio management

mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an optimized

strategic benchmark. This allocation delivers the “beta” (or markets related)

performance of your portfolio while we seek to generate additional “alpha”

(“skills related) performance with tactical adjustments, using a predefined

maximum “value at risk” envelope. Most of the portfolio’s performance is

derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or

benchmark) and pursues a “total” as opposed to “relative” return objective.

With this mandate, we seek to beat the best of “cash” or of the MSCI World

Equity index, applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage

(not exceeding 100% of NAV). You control the portfolio allocation (which can be

a pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc. This communication is provided for

information purposes only and for the recipient's sole use. Please do not

forward it without prior authorization. It is not intended as a recommendation,

an offer or solicitation for the purchase or sale of any security or underlying

asset referenced herein or investment advice. Investors should seek financial

advice regarding the suitability of any investment strategy based on their

objectives, financial situation, investment horizon and particular needs. This

report does not include information tailored to any particular investor.

It has been prepared without any regard to the specific investment objectives,

financial situation or particular needs of any person who receives this report.

Accordingly, the opinions discussed in this Report may not be suitable for

all investors. You should not consider any of the content in this report as

legal, tax or financial advice. The data and analysis contained herein are

provided "as is" and without warranty of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss

sustained by anyone who has relied on the information contained in any

publication published by BentinPartner llc. The content and views expressed in

this report represents the opinions of Marc Bentin and should not be

construed as guarantee of performance with respect to any referenced sector. We

remind you that past performance is not necessarily indicative of future

results. Although BentinPartner llc believes the information and

content included in this report have been obtained from sources

considered reliable, no representation or warranty, express or implied, is

provided in relation to the accuracy, completeness or reliability of such

information. This Report is also not intended to be a complete statement or

summary of the industries, markets or developments referred to in the

Report.

#fx #forex #investing #markets

#riskmanagement #bankingindustry #finances #money #traders #quants