Sunday, January 26, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice week ahead.

Marc

Bentin

Bentinpartner GmbH

{kind=link}

{kind=link}

Trend

Status Update

The consensus at the Davos Forum is often looked at as a contrarian

indicator. Some suggested that this year’s broadly shared opinion in Davos was the

exceptional resilience of equity markets to economic and political uncertainties

and disruptions, supported by the umbrella of extremely accommodative Central

Banks’ monetary policy. It is too early to judge but the outbreak of the corona

virus is an unexpected “curve ball” with the potential to unsettle the resilience

of consumers beyond China with their behaviour likely to be affected by a diminished

appetite to spend and travel. History also showed that the outbreak of SARS in

2003 caused a (temporary) 10% stock market correction before moving on… On the

other side of the coin, there is the possibility that these serious health (and

growth) related concerns will accelerate the Fed’s easing cycle, encouraging it

to cut rates, possibly all the way to zero (but not beyond). Last week brought

a dovish ECB and speculation that the yearly review could lead to a revision of

the ECB inflation objective (see FT article of this week end). The Fed will meet this week. The Wall Street Journal over the week end suggested the way forward for the

Fed could be to consider yield curve anchoring. This would likely imply further interest rate

cuts and the resumption of genuinely called QE, as the only question would then

be how far on the curve (but beyond Tbills!) the Fed

would be buying bonds in order to cap rates.

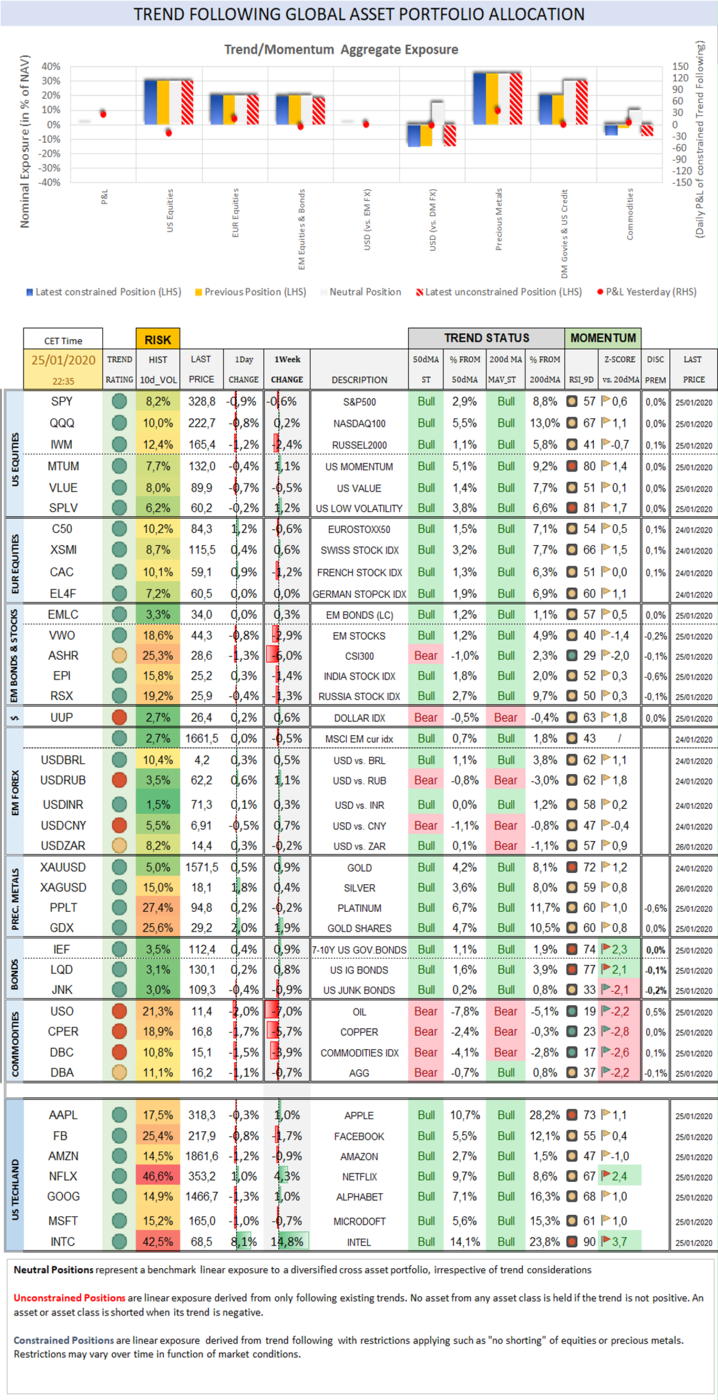

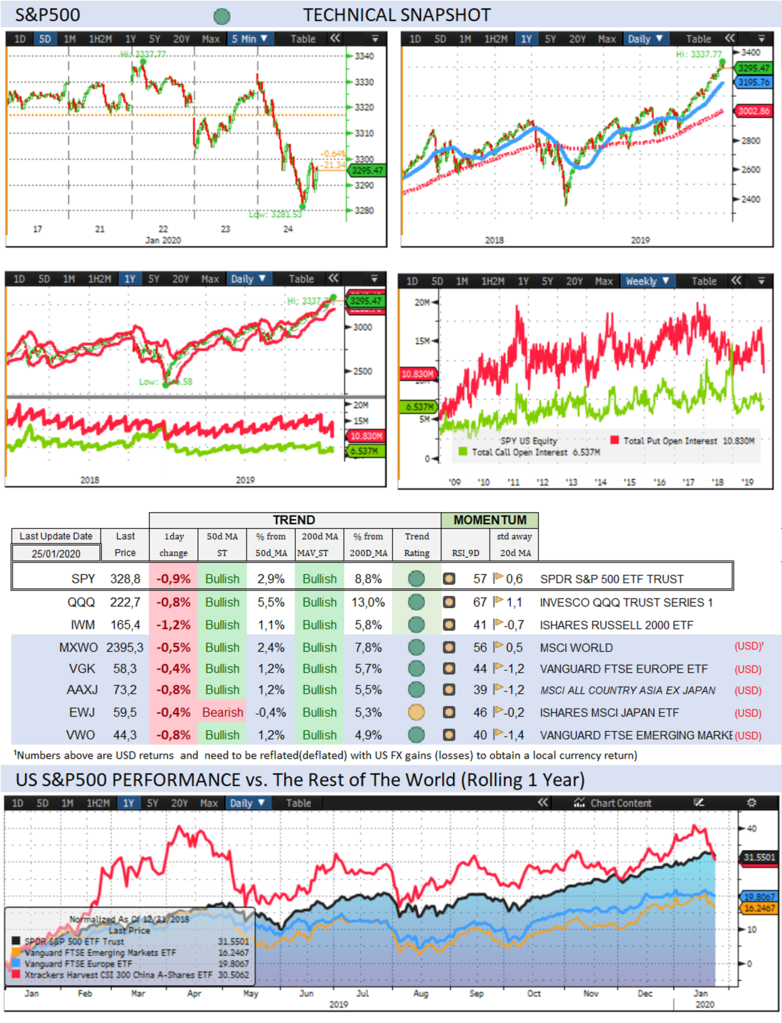

Over the past week, the S&P500 dropped -0,6% (2,1% YTD) while the

Nasdaq100 gained 0,2% (4,7% YTD). The US small cap index sold off by -2,4%

(-0,2% YTD). CBOE Volatility Index rallied 18,2% (5,7% YTD) to 14,56. AAPL gained 1,0% (8,4%). FB dropped -1,7% (6,2%). AMZN dropped -0,9% (0,7%). NFLX rallied 4,3% (9,1%, Z-score

2,4). GOOG gained 1,0% (9,7%). MSFT dropped -0,7% (4,7%). INTC rallied 14,8% (14,4%,

Z-score 3,7). IBB

(ISHARES NASDAQ BIOTECHNOLOGY) sold off by -4,5% (-3,0%, Z-score -2,5). On the macro side, in the latest indication that

lower mortgage rates are helping the housing market, US home sales jumped in

December to a 2 years high while existing home sales that make up 90% of US

home sales, jumped 10% in December on a year over year basis. The Eurostoxx50

dropped -0,6% (1,3%).

Diversified EM equities (VWO) sold off by -2,9% (-0,4%), underperforming

the S&P500 by-2,3% with Chinese shares understandably, hit the hardest by

the outbreak of the corona virus. On the week, CSI300 Chinese equity index

(ASHR) sold off by -6,0% (-3,4%). Indian shares (EPI) dropped -1,4% (1,3%). Russian

shares (RSX) dropped -1,3% (3,6%).

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies gained 0,6% (1,6%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) dropped -0,5% (-0,2%).

Including with this morning’s move, 10Y US Treasuries rallied -18bps (-28bps, Z-score -2,5)

to 1,64%. 10Y Bunds

dropped -12bps (-15bps, Z-score -2,2) to -0,34%. 10Y Italian BTPs rallied -14bps (-18bps, Z-score

-2,7) to 1,23%, underperforming Bunds by 2bps.

Quite noticeably, US High

Yield (HY) Average Spread over Treasuries climbed 36bps (20bps, Z-score 3,0) to

3,56%. US Investment Grade Average OAS climbed 2bps (3bps)

to 1,04%. In European credit markets, EUR 5Y Senior Financial Spread climbed

2bps (2bps) to 0,53%.

Gold gained 1,2% (4,1%) while Silver gained 0,8% (2,1%). Major Gold

Mines (GDX) gained 1,9% (-0,2%).

Commodities were the hardest hit sector last week. Goldman Sachs Commodity Index

sold off by -4,8% (-6,8%, Z-score -2,5). WTI Crude sold off by -7,4% (-11,3%,

Z-score -2,2).

While we cut most of our FX Model’s risks last week, we are sticking

with an overweight on RUB (vs. USD) as RUB

remains likely to benefit from its higher yielding status, Russia’s solid

fiscal stance and the rising backing of its currency by Gold which itself remains

supported by an array of reasons going well beyond the current corona virus crisis

(those were outlined in Ray Dalio’s and P. Tudor Jones interviews last week in Davos). IMF’s Georgieva warned about

the debt build-up reaching a danger point while US Treasury S. Mnuchin talked

about the Trump’s plan for tax cut 2.0 (targeting the middle class), positing that

growth would pay for it.

Over the week end…

The headlines on the spreading of the corona virus were not particularly

reassuring with the death toll rising to 80 and global cases brought to 2500 with

increased concerns that the 8 days incubation period during which contamination

occurred (and can still occur) without detection (and prior to China’s decision

to quarantine 13 cities ), significantly increased the risks of spreading the virus.

The initial market response overnight is for the S&P futures to drop

of 1.3%, 1%, 0.8% (and counting) from

Friday’s close with bonds, gold and safe haven currencies slightly higher and

EURUSD mostly stable (despite having suffered a technical setback last week

more as a result of a dovish ECB than following USD safe haven purchases). Oil

is marked 2% lower and is more unlikely to rebound (unlike stocks perhaps).

Trend Score Card

Click here for technical annotations.

{kind=link}

US

& International Equities

Check out US and International Stocks’ Technical Trend

Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and

when they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their trend,

expected Fed rate moves and speculative positioning in 10-year Treasury Futures.

{kind=link}

US

Recession Risk Radar

A comprehensive list of economic

indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs. G7

and EM counterparts.

{kind=link}

Precious Metals

Check out where precious metals

stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and futures

traders’ sentiment (non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the Stock

market correlate with each other and speculative futures positioning on

Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

Trend following offers guidance

as to when to join and when to leave an asset class with changing trend

characteristics. A disciplined and rule-based trend following investment approach

can serve as an effective portfolio insurance technique. Our purpose, beyond tracking

economic, political and monetary developments is to assist readers investing in

global markets with a keen focus on trend formation covering major asset classes.

To receive a Daily Trend Status

Update and round the clock market and economic instant messages, join a

free trial of our premium research.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery

preferences:

https://www.bentinpartners.ch/subscribe

Please visit our web site or call us at +41615444310.

We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the list,

please send us an email by clicking here, mentioning “unsubscribe” in

the title.

To ensure that our emails reach

your inbox and not your spam folder, please consider adding Marc.Bentin@BentinPartner.ch,

Marc.Bentin@BentinPartners.ch and our alternate address Bentinpartner@gmail.com

to your safe address book. If you are using Microsoft Outlook, simply right

click on our email address, choose "add to Outlook contacts" and then

"save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the recipient's

sole use. Please do not forward it without prior authorization. It is not

intended as a recommendation, an offer or solicitation for the purchase or sale

of any security or underlying asset referenced herein or investment advice.

Investors should seek financial advice regarding the suitability of any investment

strategy based on their objectives, financial situation, investment horizon and

particular needs. This report does not include information tailored to any

particular investor. It has been prepared without any regard to the specific

investment objectives, financial situation or particular needs of any person

who receives this report. Accordingly, the opinions discussed in this

Report may not be suitable for all investors. You should not consider any of

the content in this report as legal, tax or financial advice. The data and analysis

contained herein are provided "as is" and without warranty of any

kind. BentinPartner llc, its

employees, or any third party shall not have any liability for any loss sustained

by anyone who has relied on the information contained in any publication

published by BentinPartner llc.

The content and views expressed in this report represents the opinions

of Marc Bentin and should not be construed as guarantee of

performance with respect to any referenced sector. We remind you that past

performance is not necessarily indicative of future results. Although BentinPartner llc believes

the information and content included in this report have been obtained from

sources considered reliable, no representation or warranty, express or

implied, is provided in relation to the accuracy, completeness or reliability

of such information. This Report is also not intended to be a complete

statement or summary of the industries, markets or developments referred to in

the Report.

#fx #forex #investing

#markets #riskmanagement #bankingindustry

#finances #money #traders #quants