|

Accounting Weekly

September 2, 2016

|

|

|

|

|

Dear Professionals,

As we get ready to welcome Lord Ganesha with vigour, India Inc. too is probably observing Thanksgiving to the almighty for what has so far been a reasonably smooth introduction to the new Ind AS regime.

We are in the last leg of Q1 results and in this week's Results Tracker we analyse the Ind AS treatment given by 5 Companies in the Energy, Healthcare & Automobile sectors.

It seems environmental impact could soon become a trending topic in corporate reporting as well. A recent discussion paper by the International Auditing and Assurance Standards Board (IAASB) discusses the extensive use of Integrated Reporting globally. Eminent Expert Dolphy D’souza (Senior Partner and National Leader, IFRS in a member firm of Ernst & Young) ponders the future of corporate reporting and how corporates can adapt to integrated reporting.

The Institute donned its facilitator hat and issued 2 implementation guides to assist the auditing fraternity; first one being an Implementation guide for auditors reporting on Ind AS transition& relaxation of IFC rigours for smaller, lesser complex entities. FASB issued an Accounting Standard update for reporting on statement of Cash flows while PCAOB has released 35 inspection reports of audit firms including a couple of Big 4 firms.

From the editor’s desk, we bring you a note on the accounting principles to be followed for Service Concession Arrangements under Ind AS regime. We also get you another one of the recent opinions of the ICAI's Expert Advisory Committee, where the Committee guides a mining company on the accounting treatment of amounts paid for purchase of land & building.

Do not miss our special feature - 'Demystifying Ind AS' where our unique 'flowcharts' condense the verbose accounting standards into a single screen snapshot of the most relevant aspects of the standard. This week we get you an important para in Ind AS 113 - Fair Value Measurement.

We round off the Newsletter with an easy Quiz question!

Happy Reading!

Taxsutra Team

|

Our deep dive into Q1 Ind AS results continues unabated with analysis of numbers posted by 5 more companies. In the Energy Sector fair valuation of Investments dented the reported previous years profits of PSU biggie BPCL while another PSU giant IOC reported a positive impact mainly on account of fair valuation of derivative contracts.

Net adjustment to development revenue on applying Ind AS revenue standards eroded the previous years profits of real estate major DLF while Expected Credit Loss provision on receivables impacted the profits of Apollo Hospital. Tata Motors reported a positive Ind AS impact on account of deemed cost exemption relating to Property, Plant and Equipment and intangibles.

Click here to read our exclusive note analysing the above results for their Ind AS treatment.

|

The Future of Corporate Reporting - Key Messages for Indian Companies

Now that Ind AS is finally here, India is as close to global accounting standards as we have ever been. However the diminishing investor trust worldwide in corporate reporting has meant more reliance on non-traditional and non-audited information like analyst reports, online news and social media.

International Auditing and Assurance Standards Board (IAASB) recently issued a discussion paper titled “Supporting Credibility and Trust in Emerging Forms of External Reporting: Ten Key Challenges for Assurance Engagements.” This paper acknowledges the extensive use of Emerging Forms of External Reporting (EER) globally that is the use of non-financial reporting with financial reporting i.e. Integrated Reporting.

Eminent expert Dolphy D’Souza, (Senior Partner and National Leader, IFRS in a member firm of Ernst & Young), in his reflective piece, calls for Companies to adopt Integrated Reporting. He opines that “...the aim of integrated reporting is to provide more comprehendible information and a big picture of how companies create value by bringing together the different elements of reporting.” He also lays out for Indian companies the four mantras of non-financial reporting.

Click here to read this timely piece : The Future of Corporate Reporting - Key Messages for Indian Companies. |

FASB issues Accounting Standard Update: Statement of Cash Flows

FASB issues Accounting Standard Update (ASU): Statement of Cash Flow due to diverse practices for reporting on the statement of cash flows. This ASU is issued with the aim of reducing the prevailing diversity in practices. The ASU provides specific guidance for the cash flow issues relating to debt repayment or debt extinguishment costs, settlement of zero-coupon debt instruments, Contingent Consideration Payments Made after a Business Combination, Proceeds from the settlement of insurance claims, etc.

Click here to read the key takeaways from this FASB Update. |

ICAI relaxes Internal Financial Controls scrutiny of "smaller, less Complex" companies

ICAI has issued an Implementation Guide for the Auditors of Smaller, Less Complex Companies to help them cope with practical difficulties faced during the audit of Internal Financial Controls. The Guide states that auditors need to exercise professional judgement while determining scope of audit. Auditors need to work around inherent problems of smaller entities namely absence of documentation, management override of controls, and segregation of duties. Auditors could satisfy themselves by evaluating other corroborating evidences, compensatory controls, increased substantive testing, & absence of misstatements.

Click here to read the key takeaways from this implementation guide. |

ICAI's implementation guidance for auditors reporting on Ind AS transition

The Guide deals with first time adoption adjustments made and auditors’ responsibilities on reporting of corresponding figures. In case prior year financial statements were audited by another auditor, either the incoming auditor can audit the corresponding figures for Ind AS transition adjustments or the predecessor auditor can audit the adjustments and give an audit opinion on the same. If the incoming auditor audits the transition adjustments, it is implied that auditor will perform requisite procedures as per SA 710. Auditors can use work of an expert for dealing with complexities, however they cannot refer to work of the expert in an unmodified opinion.

Click here to read the key takeaways from this important implementation guide. |

Umpire's Verdict - ICAI Advisory |

The ICAI’s Expert Advisory Committee guides a mining Company who paid huge sums of money to acquire land and building with the aim to extract minerals. The Company had capitalised the Land under Fixed Assets.

The Statutory Auditor and the Comptroller and Auditor General (C&AG) raised an objection on the treatment followed by the Company. In their view, ‘Land’ should have been treated as ‘Current Assets’ as the motto of the Company is extraction of the minerals. Also, the building cost should be shown separately as ‘Fixed Assets’ and the same should be written off in the Statement of Profit and Loss account once the building is demolished.

The Company worried over the financial impact of this proposed accounting treatment, approached the EAC for their opinion. The Company contended that Land would not be “used” or consumed under the mining process and could be restored back to its original state and could be sold. Also, the costs of demolishing the building and rehabilitation costs paid were incidental to the acquisition of the land and have to be included in the cost of Land capitalised.

Does the EAC concur with the Company or finds logical reasoning with the Auditors contentions?

Click here to read the rationale of the Expert Advisory Committee and summary of the opinion. |

From the Editors' Desk... |

Service Concession Arrangements (SCA)

Service Concession Arrangements are arrangements between public sector entity and private sector Company for construction of infrastructure assets. In IGAAP, there was no specific accounting standard for this topic. Appendix A to Ind AS 11 sets out the accounting requirements for service concession arrangements, while Appendix B to Ind AS 11 contains disclosure requirements. Service Concession Arrangements are arrangements between public sector entity and private sector Company for construction of infrastructure assets. In IGAAP, there was no specific accounting standard for this topic. Appendix A to Ind AS 11 sets out the accounting requirements for service concession arrangements, while Appendix B to Ind AS 11 contains disclosure requirements.

Click here to read more about how Ind AS has changed the accounting for SCA?

|

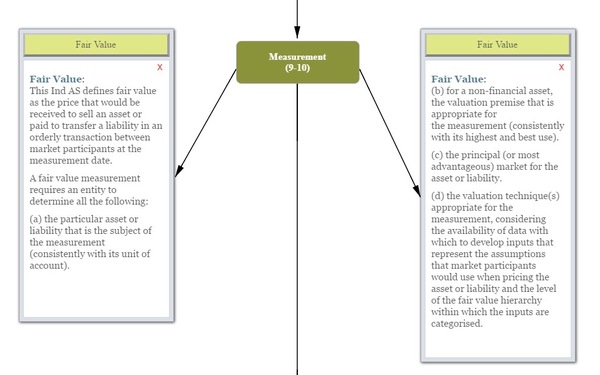

Demystifying Ind AS 113 - Fair Value Measurement |

|

Para 9 of Ind AS 113 Fair Value Measurement defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Fair Value Measurement is an important standard since most of the other Ind AS refers back to this standard for measurement of fair value. Over the past few weeks, we have noticed that most of the Companies applying Ind AS have been impacted by Fair Valuation one way or the other.

Click here to read the provisions of this all important Standard in detail.

|

Ind AS Quiz Latest from the World of Accounting

|

As per Ind AS 36, when an impairment loss recognised has to be reversed, which of the following adjustments have to be made?

1. Recognise reversal in the income statement and adjust the depreciation for future periods

2. Recognise reversal in the income statement without adjustment to the depreciation for future periods

3. Recognise reversal in the statement of changes in equity and adjust the depreciation for future periods

4. Recognise reversal in the statement of changes in equity without adjustment to the depreciation for future periods

|

|

veteran Natraj Ramkrishna to join EY

|

|

|

|

Readers can activate their Free Trial to our Accounting Portal now! For subscription enquiries and limited period discount offers, drop a mail to: sales@taxsutra.com.

|

|

|

|