Sunday, May 24, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice evening.

Marc

Bentin

Bentinpartner GmbH

{kind=link}

{kind=link}

Trend

Status Update

XLI (INDUSTRIAL SELECT SECT SPDR) rallied 7,4% (-21,6%), XLE (ENERGY

SELECT SECTOR SPDR) rallied 6,9% (-35,9%), KBE (SPDR S&P BANK ETF) rallied

8,4% (-38,9%), suggesting some revival in the cyclical value segment.

Most of the gains came from early in the week on

expectations for more liquidity provisions and fiscal support, comforted by hopes (and mostly hype) that Moderna was about to deliver a vaccine (which was

downplayed on Thursday). The Federal Reserve’s balance sheet increased to $7.09

trillion for the week, up from $6.98 trillion the week before. Democrats and

Republicans cooperated to deliver the initial $2 trillion CARES Act (supplemented

by $484 billion in funding for small businesses). Negotiations have now moved

to the HEROES Act that would provide in a few weeks’ time $3 trillion (worth

15% of GDP) in additional relief funding, answering the call for more fiscal

support by the Federal Reserve last week.

While Senate Republicans have not expressed much interest in the bill,

senior White House officials have indicated that D. Trump would support the

distribution of further stimulus checks and N. Pelosi expressed confidence over

the week end for a bipartisan support. Treasury Secretary Mnuchin also explained

how the distribution of money will work next time.

Cboe Volatility Index sold off by -11,7% (104,4% YTD)

to 28,16.

The Eurostoxx50 rallied 5,0% (-21,3%), outperforming the S&P500 by

1,8%, jolted by the EUR500bn Franco-German plan for joint issuance (more than

the amount, it was the principle of joint issuance that was cheered) aimed at

aiding post-coronavirus economic recovery.

Diversified EM equities (VWO) gained 1,0% (-18,8%), underperforming the

S&P500 by -2,2%. ASHR (XTRACKERS HARVEST CSI 300 CH) dropped -1,4% (-9,3%).

Larry Kudlow said nobody can invest confidently in Chinese companies and

that the U.S. needs to protect investors from the country’s lack of

transparency and accountability. ‘We have learned that Chinese companies are

not transparent,’ Kudlow said. ‘They do not meet the norms, the regulations.’

Kudlow pointed to potential lawsuits related to the coronavirus, saying ‘until

that stuff is sorted out, nobody really can invest with confidence in China.’

The discussion to restrict Chinese shares trading on US exchanges intensified

as well, bringing the trade war to the financial scene. China is no saint and

does not even claim to be a democracy. But for an international investor seeking long

term appreciation and diversification, it would be a mistake, in our view, not

to be invested in China’s markets for its currency, stock and bond markets are

bound to appreciate over the coming years if not in absolute then in relative

terms to the rest of developed markets as the world seeks to diversify away

from Western and US markets to accommodate the emergence of a more multipolar

world likely to sever its dependency and excessive reliance on the USD for

conducting trade (the petrodollar is being challenged as well) and managing

world reserves (60% + invested in USD). There will be efforts to torpedo Chinese

markets that will lead Chinese stocks to delist from US markets, going to Hong

Kong, Singapore, London, Frankfurt or Paris. There will be efforts to force US

pensions out of them on political ground and that is ok. But it will make

little difference in the end.

There will be efforts to keep the weights of CNY in the SDR low at each

quinquennial reweighing (the SDR is a basket of USD, EUR, JPY, GBP and CNY used

as an allocation by some key supranational organisations but not only). The

last reweighing of the SDR was made mostly at the expense of the euro, rather

than out of the USD which was at least in some ways, politically motivated. Ditto

for international equity and bond indices. There is and will be pressures to

keep the weight of Chinese assets disproportionately low to their economic

importance. That might be an increasingly difficult posture to hold in the

future as well as China’s economic power and importance keep climbing.

Financial repression will take many forms and this will be one of them;

preventing or discouraging investors to go where the potential for gains

outside of zero yielding government bonds and even US stocks will be the

highest. Governments are “sacrificing” savers on the altar of necessity to

remain solvent (you cannot run debt/GDP ratio in excess of 150%, pay a decent

interest and stay solvent, as Japan running on a 250% debt/GDP ratio and 0%

interest rates, has learned a long time ago. Those free of political

constraints should also be invested in China on pure investing considerations,

in our view. At the very least, they should be mindful that L. Kudlow who is

never shy of financial prognostication is most reliable as a contrarian

indicator (his bearish call on gold being his major and least prescient calls).

His duty is understandably to be a cheerleader but as an advisor, he will be

wrong again in the future.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies dropped -0,7% (3,9%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) gained 0,3% (-5,9%).

The euro strengthened following the agreement by A. Merkel to concede

some joint issuance for the EUR500bn covid fund.

EURUSD gained 0,7% (-2,8%). EURCHF gained 0,7% (-2,4%). EURJPY gained 1,1% (-3,7%).

EURGBP gained 0,3% (5,9%).

The dollar weakened selectively

vs. certain EM currencies. USDBRL dropped by -5,5% (37,5%). USDRUB sold off by -2,6%

(15,5%). USDMXN sold off by -5,1% (20,1%, Z-score -2,3). USDZAR

sold off by -5,2% (25,9%, Z-score -2,3).

10Y US Treasuries dropped 2bps (-126bps) to 0,66%. 10Y Bunds climbed 4bps

(-30bps) to -0,49%. 10Y Italian BTPs rallied -27bps (19bps) to 1,60%,

outperforming Bunds by -3bps.

US High Yield (HY) Average Spread over Treasuries dropped -77bps

(344bps) to 6,80%. US Investment Grade Average OAS dropped -24bps (87bps) to

1,88%. The full action of the Fed program in the corporate sector was in full

display on LQD last week , rallying 1,7% (2,1%) having now

recouped most of a 25% loss. Risk reversals went from -30 at the peak crisis to

just over the 3-year average of -2.2 at the close of last week. Official investment flows and % of AUM growth

YTD climbed to +30%). The Fed challenge

will be to sustain the effort and keep underwriting an entire corporate debt

index as M. El Arian suggested here, while still praising, like W. Buffet, the decisive

action of the Fed in a time of crisis. Now, besides the urge to copycat the

Fed’s action (a strategy that many advocate including Blackrock mandated by the

Fed), it might be a less desirable investment to buy an entire asset class populated

by an ever larger percentage of fallen angels (see Economist article) and zombie companies vs. owning a barbell of

solid cash flow producing equities, some high yields, EM market debt (in local

currencies), Gold and silver, in our view.

{kind=link}

In European credit markets, EUR 5Y Senior Financial Spread dropped

-16bps (43bps) to 0,95%.

Gold dropped -0,5% (14,3%) while Silver rallied 3,6% (-3,6%), continuing

to outperform and breaking higher. Major Gold Mines (GDX) sold off by -2,8%

(21,4%).

Some of the world’s most-prominent investors raised alarm bells over the

looming threat of inflation, and turning to gold for protection. Hedge fund

managers Paul Singer, David Einhorn, and Crispin Odey

are among those bullish on gold… So are large asset managers like Blackrock (which

are also implementing the Fed’s asset buying program).

No surprise that we stumbled last week however. It is a pattern that each

approaching future expiration is a near term challenge that needs to be

overcome before prices can move higher.

Goldman Sachs Commodity Index rallied 4,6% (-37,6%). WTI Crude rallied 13,0%

(-45,5%). XLE (ENERGY SELECT SECTOR SPDR)rallied 6,9%

(-35,9%).

As a conclusion to this week’s letter, we would like to refer our

readers to a most interesting essay from R. Dalio on

the “Big Cycle of the Life of an Empire” covering 500 years of monetary history in just a

few pages. It is straightforward to see what part of the cycle we are in and

what might come next, even if history does not repeat itself and just rhythms.

This is particularly insightful reading in support of the discussion above on

the opportunity (or not) to keep at least a foot in China as an investor.

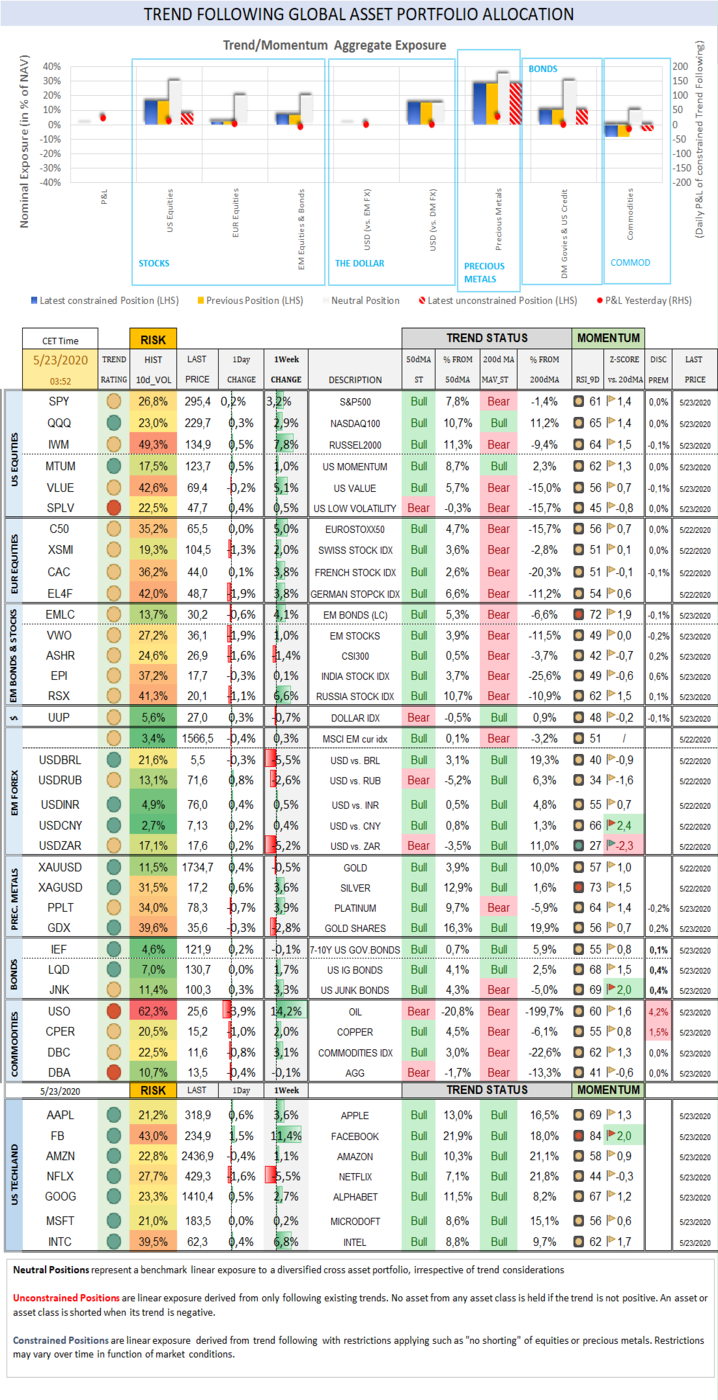

Trend Score Card

Click here for

technical annotations.

{kind=link}

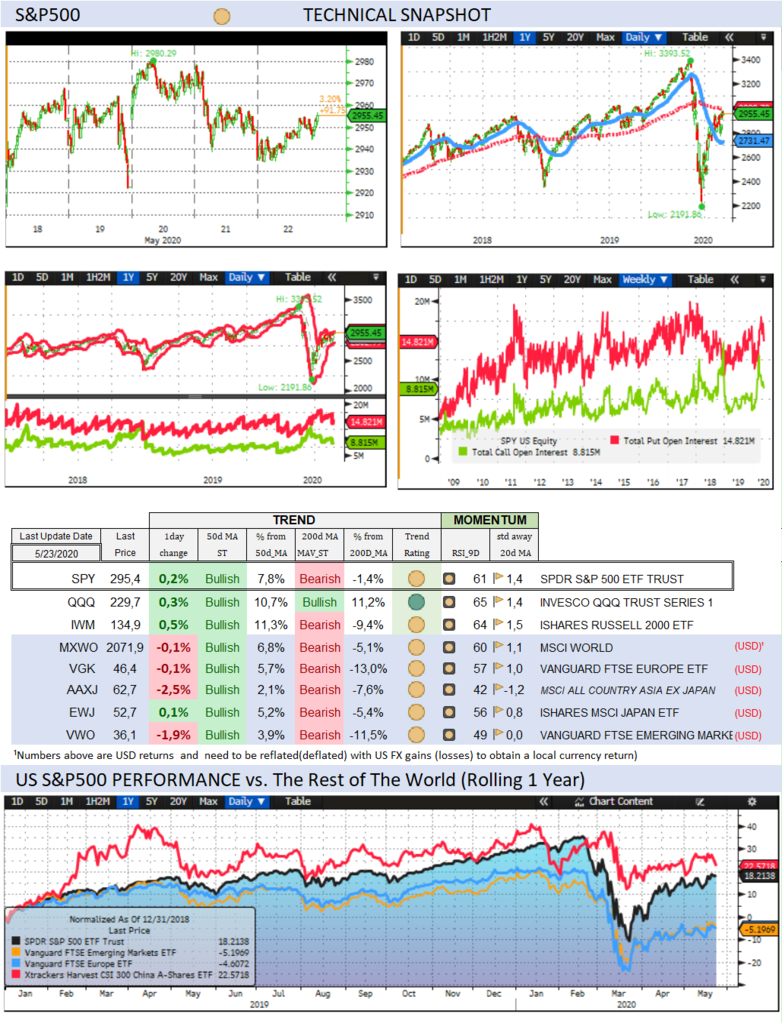

US

& International Equities

Check out US and International Stocks’ Technical Trend

Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and

when they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their trend,

expected Fed rate moves and speculative positioning in 10-year Treasury Futures.

{kind=link}

US

Recession Risk Radar

A comprehensive list of economic

indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs.

G7 and EM counterparts.

{kind=link}

Precious Metals

Check out where precious metals

stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and

futures traders’ sentiment (non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the Stock

market correlate with each other and speculative futures positioning on

Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and

rule-based trend following investment approach can serve as an effective

portfolio insurance technique.

To receive a Daily Trend Status

Update and round the clock market and economic instant notifications, join the

free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery

preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio Management and Advisory Services

BentinPartner GmbH is a

Swiss registered independent financial adviser. We offer four different

portfolio management mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an

optimized strategic benchmark. This allocation delivers the “beta” (or markets

related) performance of your portfolio while we seek to generate additional

“alpha” (“skills related) performance with tactical adjustments, using a

predefined maximum “value at risk” envelope. Most of the portfolio’s

performance is derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or benchmark)

and pursues a “total” as opposed to “relative” return objective. With this

mandate, we seek to beat the best of “cash” or of the MSCI World Equity index,

applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage

(not exceeding 100% of NAV). You control the portfolio allocation (which can be

a pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at +41615444310.

We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the list,

please send us an email by clicking here, mentioning “unsubscribe” in

the title.

To ensure that our emails reach

your inbox and not your spam folder, please consider adding Marc.Bentin@BentinPartner.ch,

Marc.Bentin@BentinPartners.ch and our alternate address Bentinpartner@gmail.com

to your safe address book. If you are using Microsoft Outlook, simply right

click on our email address, choose "add to Outlook contacts" and then

"save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the

recipient's sole use. Please do not forward it without prior authorization. It

is not intended as a recommendation, an offer or solicitation for the purchase

or sale of any security or underlying asset referenced herein or investment

advice. Investors should seek financial advice regarding the suitability of any

investment strategy based on their objectives, financial situation, investment

horizon and particular needs. This report does not include information tailored

to any particular investor. It has been prepared without any regard to the

specific investment objectives, financial situation or particular needs of any

person who receives this report. Accordingly, the opinions discussed in

this Report may not be suitable for all investors. You should not consider any

of the content in this report as legal, tax or financial advice. The data and

analysis contained herein are provided "as is" and without warranty

of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss sustained

by anyone who has relied on the information contained in any publication

published by BentinPartner llc.

The content and views expressed in this report represents the opinions

of Marc Bentin and should not be construed as guarantee of

performance with respect to any referenced sector. We remind you that past

performance is not necessarily indicative of future results. Although BentinPartner llc believes

the information and content included in this report have been

obtained from sources considered reliable, no representation or

warranty, express or implied, is provided in relation to the accuracy,

completeness or reliability of such information. This Report is also not

intended to be a complete statement or summary of the industries, markets or

developments referred to in the Report.

#fx #forex

#investing #markets #riskmanagement #bankingindustry #finances #money #traders #quants