Monday, July 06, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Our

apologies for the irregularity of comments last week caused by our server’s

problems (which we think and hope are resolved).

Have

a nice week.

Marc

Bentin

Bentinpartner GmbH

{kind=link}

{kind=link}

Trend

Status Update

For a more complete explanation of where we we stand, we recommend

listening to last week’s 30’ Bloomberg

interview from Ray Dalio where he said that we are now facing three major

risks;

- the mature state of a long-term debt cycle

similar to the one encountered in the 30’s, 1945 and 1971 (which all led to

currency devaluations of their own).

- an historic wealth gap leading to the rise to a “value”

(serial bubbles fed by central banks) and “political” gaps (from electing populist

leaders).

- the rise of a great power challenging the

existing one (leading to trade, cold and sometimes hot wars).

In this interview, he also said that free markets have ceased to preside

the allocation of capital as central banks de facto became the new market

makers. When asked about the “limit” of this state of affairs, he said that

there is none (in sight), that central banks’ balance sheets are set to (further)

explode with no limiting factor, beyond a currency implosion. On that topic, he

made a point that we made earlier (in all humility) debunking the “big dollar

short” argument resulting from the foreign stock of USD labelled debt (which

only needs to be defaulted on to disappear…).

He opined that equity markets’ PE could rise as high as 50 (just to give

a number) and that this metric should not be used as a point of reference in

the traditional sense anymore.

From an investment perspective, he repeated that the only valid “reflation

trades” are primarily equities and gold, not cash or bonds that are essentially

taxed to the tune of a large negative real interest rate.

Also worth listening to was N. Roubini’s interview (dubbed “perma bear” for a reason) from two

weeks ago. The major take away there was that the

world economy is facing a supply shock from deglobalisation and productivity losses

coming from the separation of the internet, 5G and technological standards

between the US and China. The investment conclusion was the same that the time

has come to protect oneself from inflation of goods, assets and ultimately a looming

currency crisis.

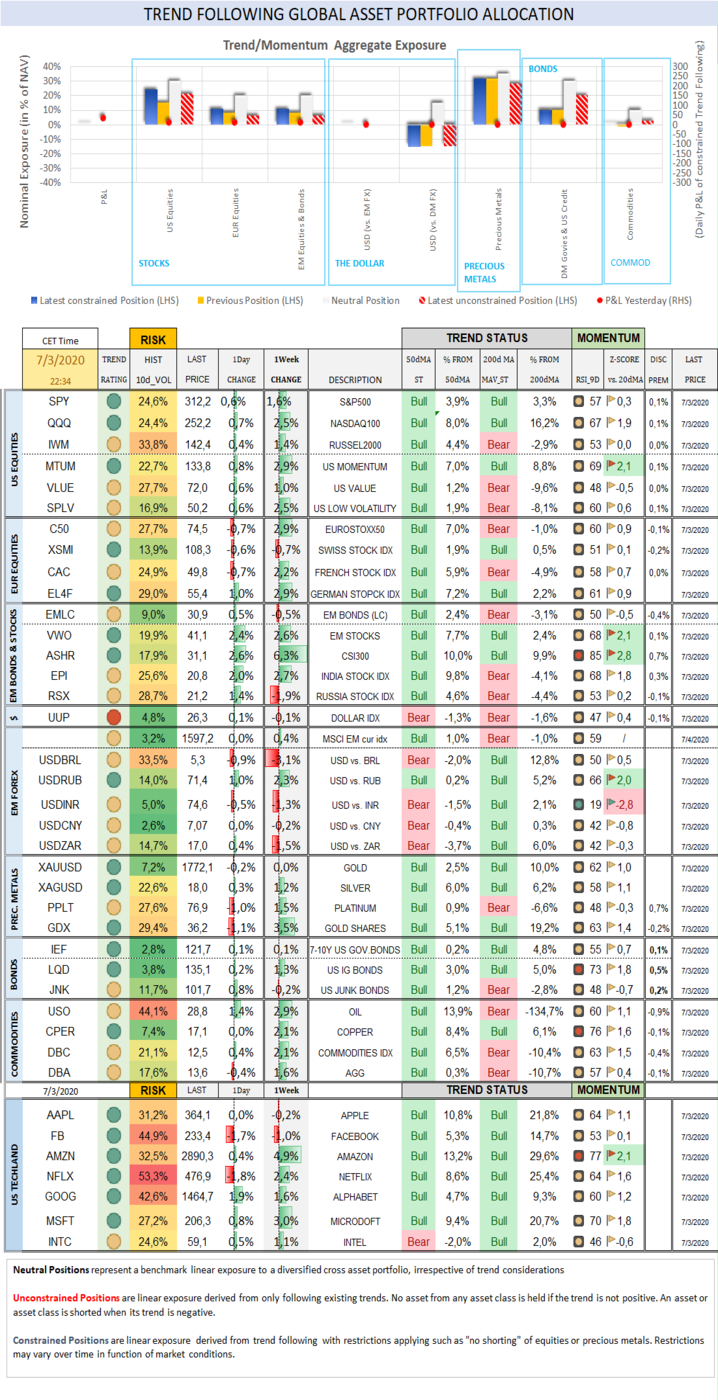

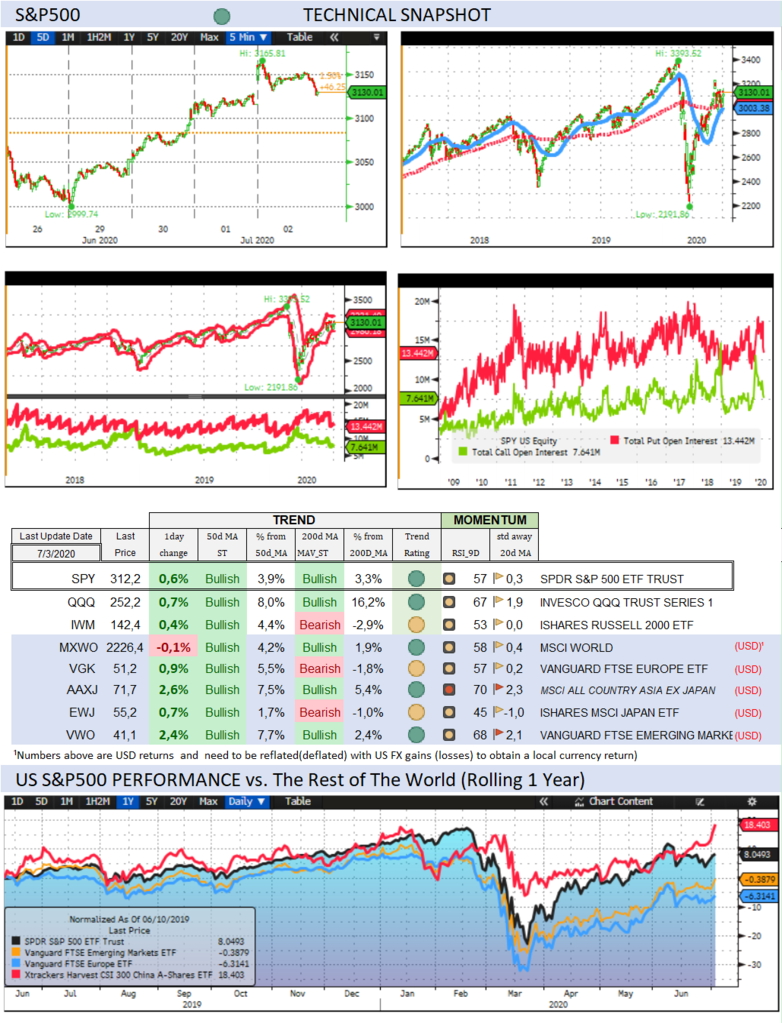

Lat week, the S&P500 gained 1,6% (-3,0% YTD) while the Nasdaq100

rallied 2,5% (18,6% YTD). The US small cap index gained 1,4% (-14,0% YTD).

Tech remained market leaders amidst a resurgence of Covid

19 cases in the US and around the world. AAPL dropped -0,2% (24,0%). FB dropped -1,0% (13,7%). LYFT sold off by

-4,1% (-26,0%). AMZN

rallied 4,9% (56,4%, Z-score 2,1). NFLX rallied 2,4% (47,4%). GOOG gained

1,6% (9,5%). MSFT rallied 3,0% (30,8%). INTC gained 1,1% (-1,2%).

CBOE Volatility Index sold off by -14,1% (100,9% YTD) to 27,68.

The Eurostoxx50 added strong gains last week, gaining 2,9% (-10,4%),

outperforming the S&P500 by 1,3%. European markets were supported by a

solidifying support in Germany for more fiscal stimulus and the vote on

Thursday closing the controversy on the Constitutional Court Ruling that had

deemed the ECB asset purchase program unconstitutional and against the statutes

of the ECB.

Diversified EM equities

(VWO) rallied 2,6% (-7,6%, Z-score 2,1), outperforming the S&P500 by 1,1%, mainly led

by Chinese markets which reacted positively to the golden cross formation that was

comforted by surprisingly strong Chinese data later last week. With this latest

burst, Chinese stocks took the lead on the score card for the year, at the same time as it broke technical key

resistance levels on Friday. CSI300

Chinese equity index (ASHR) rallied 6,3% (5,1%, Z-score 2,8) for the

week.

{kind=link}

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies dropped -0,1% (1,2%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) gained 0,4% (-4,1%). USDRUB rallied 2,3% (15,2%, Z-score 2,0) last week despite a

further rally in oil prices and risk appetite with RUB adversely hit by

seasonal weakness as Russian companies sold RUB to pay for dividends (according

to a JPM report). RUB may still be slightly over-owned as a convenient “carry

trade” but remains fundamentally (and grossly) undervalued. We are reinstating

the RUB overweight closed last week in our paper model FX overlay. The USD

traded erratically vs. G7 counterparts and remained in a trading range (with

downside potential in our view). There is no real FX safe haven anymore

(besides CHF to a point) as FX volatility increases and we remained

underweighted JPY (in what remains largely a contrarian trade).

10Y US Treasuries dropped 3bps (-125bps) to 0,67%. 10Y Bunds climbed

5bps (-25bps) to -0,43%. 10Y Italian BTPs dropped -4bps (-16bps) to 1,26%,

underperforming Bunds by 4bps.

US High Yield (HY) Average Spread over Treasuries dropped -5bps (264bps)

to 6,00%. US Investment Grade Average OAS dropped -10bps (47bps) to 1,48%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -9bps

(24bps) to 0,76%.

Gold was unchanged on the week (16,8%) while Silver further played

further catch up, adding 1,2% (0,9%). Major Gold Mines (GDX) rallied 3,5%

(23,5%).

Goldman Sachs Commodity Index rallied 3,9% (-30,7%). WTI Crude rallied

4,8% (-34,0%). Despite all the (now convenient) talks about deflation,

technically at least, the floor could be in sight for commodities in general.

Most cyclical up-moves in commodities have in the past started with Gold, then

followed by silver (which has recently turned the corner vs. gold as suggested

by the gold/silver ratio). Even copper which has recovered 36% from its lows is

supported by revival expectations in China.

Overnight…

Nikkei +1.2%; CSI300 +3.3%;

S&P500 future +37 points

Trend Score Card

Click here for

technical terminology.

{kind=link}

US

& International Equities

Check out US and International Stocks’ Technical

Trend Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and when

they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their

trend, expected Fed rate moves and speculative positioning in 10-year Treasury

Futures.

{kind=link}

US

Recession Risk Radar

A comprehensive list of

economic indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs.

G7 and EM counterparts.

{kind=link}

Get the Score card of all major currency pairs in terms

of Trend, Momentum, Carry, GDP and Current account differential

Precious Metals

Check out where precious

metals stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and

futures traders’ sentiment (non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the

Stock market correlate with each other and speculative futures positioning

on Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and rule-based

trend following investment approach can serve as an effective portfolio

insurance technique.

To receive a Daily Trend

Status Update and round the clock market and economic instant notifications, join the

free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio Management and Advisory Services

BentinPartner GmbH is a

Swiss registered independent financial adviser. We offer four different

portfolio management mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an

optimized strategic benchmark. This allocation delivers the “beta” (or markets

related) performance of your portfolio while we seek to generate additional

“alpha” (“skills related) performance with tactical adjustments, using a

predefined maximum “value at risk” envelope. Most of the portfolio’s

performance is derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or

benchmark) and pursues a “total” as opposed to “relative” return objective.

With this mandate, we seek to beat the best of “cash” or of the MSCI World

Equity index, applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage (not

exceeding 100% of NAV). You control the portfolio allocation (which can be a

pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the

recipient's sole use. Please do not forward it without prior authorization. It

is not intended as a recommendation, an offer or solicitation for the purchase

or sale of any security or underlying asset referenced herein or investment

advice. Investors should seek financial advice regarding the suitability of any

investment strategy based on their objectives, financial situation, investment

horizon and particular needs. This report does not include information tailored

to any particular investor. It has been prepared without any regard to the

specific investment objectives, financial situation or particular needs of any

person who receives this report. Accordingly, the opinions discussed in

this Report may not be suitable for all investors. You should not consider any

of the content in this report as legal, tax or financial advice. The data and

analysis contained herein are provided "as is" and without warranty

of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss

sustained by anyone who has relied on the information contained in any

publication published by BentinPartner llc. The content and views expressed in this report

represents the opinions of Marc Bentin and should not be construed as

guarantee of performance with respect to any referenced sector. We remind you

that past performance is not necessarily indicative of future results. Although

BentinPartner llc believes

the information and content included in this report have been

obtained from sources considered reliable, no representation or

warranty, express or implied, is provided in relation to the accuracy,

completeness or reliability of such information. This Report is also not

intended to be a complete statement or summary of the industries, markets or

developments referred to in the Report.

#fx #forex #investing #markets

#riskmanagement #bankingindustry #finances #money #traders #quants