Monday, July 13, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice week end.

Marc

Bentin

Bentinpartner

GmbH

{kind=link}

{kind=link}

Trend

Status Update

Overall, markets focussed on the intensifying economic recovery (the US economic surprise index going parabolic shows most

metrics of recovery beating expectations) and declining mortality rather than

on rising infection rates. The IPO market seemed to be catching a bid as well

as companies rushed to bolster their balance sheet.

{kind=link}

After wobbling for two days, US stocks squeezed on Friday despite

Chinese stocks ebbing back this time on official comments tempering the

week-long rabid enthusiasm for Chinese stocks. A parallel was drawn with what happened in 2015 with the last

Chinese stocks rally that ended in tears. Today’s situation is fundamentally

different, with China on a firm path to assert its financial, technological and

geopolitical clout while only coming off from three years of underperformance.

That being said, there are causes for concern regarding Beijing which

has moved to de facto seize control of Hong Kong. It also mobilised its

military against Taiwan threatening of an invasion and it made several military

incursions into India that killed several Indians in borders incidents, in all

impunity and no fear of retorsion. No doubt that China is in an accelerating

power grab and that Western powers have been naive to think that China shared

more democratic than hegemonic inclinations. The covid situation proves to be a

catalyst for this but it started with Western consumers buying Chinese goods,

Western companies producing locally and accepting technology transfers in

exchange for a (sometimes) elusive access to the promised land and the pursuit

of higher profits. It continued with Western shareholders accepting to sell

out, most often to government controlled public companies, hundreds of billions

worth of Western companies and key technology with freshly printed Chinese

money (Syngenta being a USD50bn case in point).

Where does that leave us as an investor? Should we refrain from

investing in China or Russia which are both rising and increasingly dominant

geopolitical and economic powers? Just like we should filter out anything that

is not 100% ESG compliant?

Each and every one should decide for herself/himself ...but as a

European I feel more comfortable owning a mix of stocks including EM names from

Russia and China because the disorderly action on US tech is not reassuring

either (not to speak about the way the US has been treating its traditional

“allies”). Perhaps, there are only two genuine monopolies worth their dollars;

Microsoft and Google with everything else more or less beatable, breakable and

replicable.

In any case and before even considering that Chinese shares could be in

a “bubble”, we should look at investors piling over each other to buy Tesla, an

average quality car producer sold and priced as a perfect software company with more “silly” valuation a distinct

possibility in the future, now that the company seems set to enter the S&P500

with trillions of passive investment following this equity benchmark.… For what

it is worth, Tesla added 28% last week, accruing month to date gains to +51%

and YTD gains to 269%.

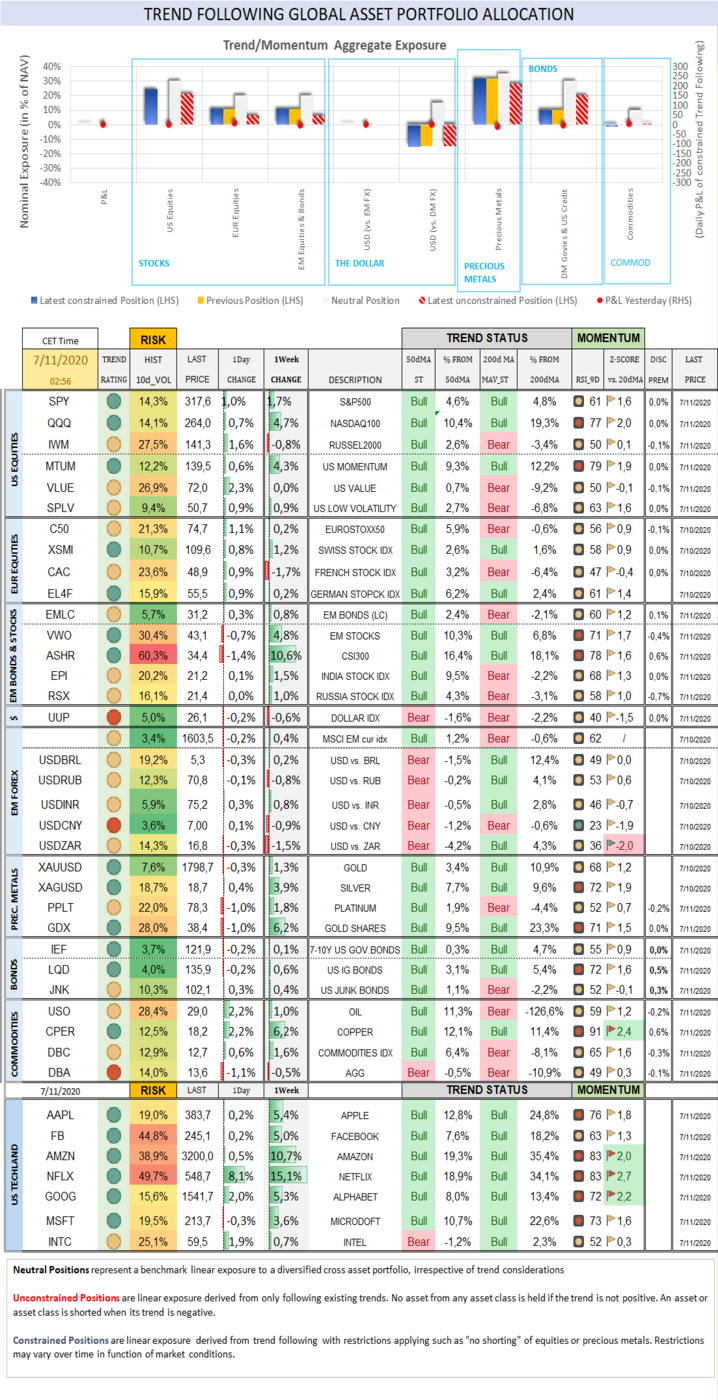

Over the past week, the S&P500 gained 1,7% (-1,3% YTD) while the

Nasdaq100 rallied 4,7% (24,2% YTD). The US small cap index dropped -0,8%

(-14,7% YTD).

Cboe Volatility Index dropped -1,4% (98,0% YTD) to 27,29.

The Eurostoxx50 gained 0,2% (-10,2%), underperforming the S&P500

by-1,5%.

Diversified EM equities (VWO) rallied 4,8% (-3,1%), outperforming the

S&P500 by 3,1%. CSI300

Chinese equity index (ASHR) rallied 10,6% (16,2%). Indian shares (EPI)

gained 1,5% (-15,0%). Russian shares (RSX) gained 1,0% (-14,2%).

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies dropped -0,6% (0,5%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) gained 0,4% (-3,7%).

10Y US Treasuries rallied -2bps (-127bps) to 0,64%. 10Y Bunds dropped

-3bps (-28bps) to -0,47%. 10Y Italian BTPs dropped -3bps (-19bps) to 1,23%,

outperforming Bunds by 0bps.

US High Yield (HY) Average Spread over Treasuries dropped -3bps (261bps)

to 5,97%. US Investment Grade Average OAS climbed 0bps (47bps) to 1,48%.

In European credit markets, EUR 5Y Senior Financial Spread climbed 1bps

(25bps) to 0,77%.

Gold gained 1,3% (18,5%) while Silver rallied 3,9% (4,9%). Major Gold Mines (GDX) rallied 6,2%

(31,1%).

Goldman Sachs Commodity Index gained 1,3% (-29,9%). WTI Crude dropped

-0,2% (-33,6%).

Over the week end…

Ø Asia tracking Wall Street's advance (Nikkei +1.8%;

CSI300 +0.95%) and U.S. futures (+16 points) is rising ahead of the earnings

season.

Ø The earnings season kicks off this week with

JPMorgan, Citi and Wells reporting before the US open on Tuesday along with a

few consumer names and Netflix.

Ø The pace of new virus infections in the U.S. slowed

to 1.7%, below the seven-day average, but Florida reported 15,299 new cases,

its biggest one-day rise, as Disney World reopened its gates.

Ø OPEC+ meets on Wednesday to consider curbs of 9.6

million barrels a day or taper to 7.7 million as planned. The aim is to avoid a

"taper tantrum" of the sort the Fed faced when it proposed tightening

monetary policy in 2013.

Ø Business

optimism and consumer prices are due out on Tuesday, Industrial production on

Wednesday and June retail sales on Thursday (expected at -4.5% mom).

Ø Several Fed speeches including from New York Fed

President Williams and St. Louis Fed President Bullard are due.

Ø EU leaders

will meet in Brussels on Thursday for a summit to formalize agreement on the

EUR750bn pandemic recover plan.

Ø D. Trump is trailing in the polls; caught between

the scissor’s effects of a pandemic (he was seen wearing a mask this week end)

and a radical drift. The former largely has been detrimental to him but the

latter is largely positive. Should equity markets hold (or inflate further)

with anything but a total disaster unwinding on the sanitary front, D. Trump

will gather his political instincts to capitalize on the repulsion caused among

“a majority” of Americans by a movement that attacks American national symbols.

The more statues will fall, the more votes he will grab…

Trend Score Card

Click here for technical

terminology.

{kind=link}

US

& International Equities

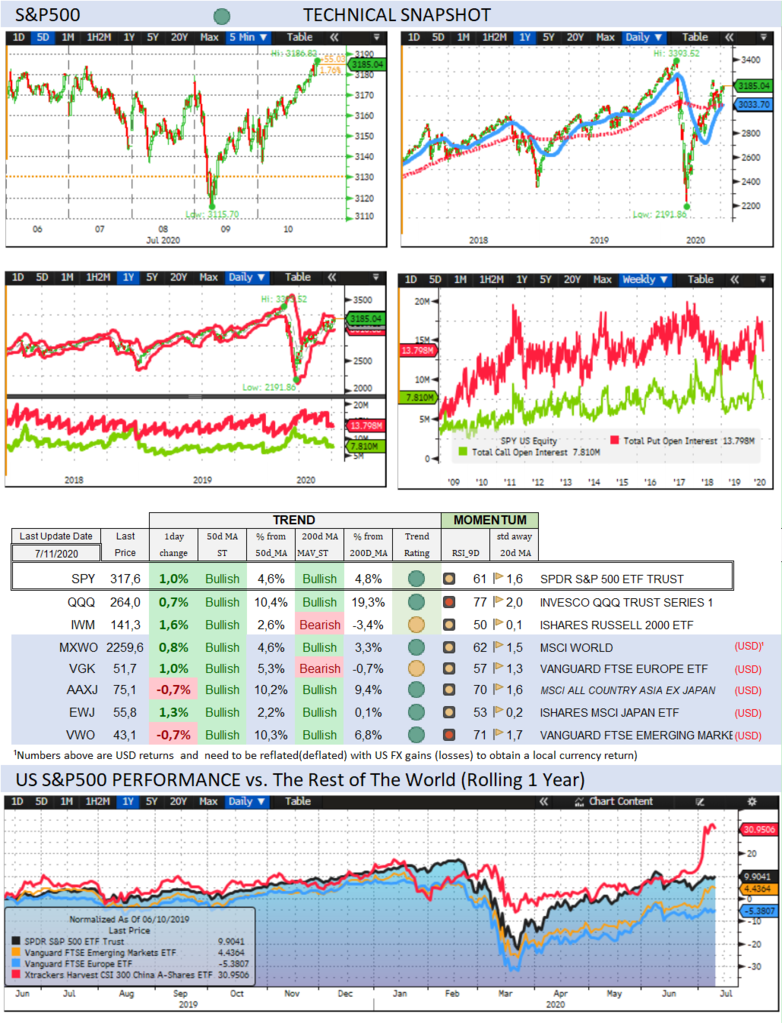

Check out US and International Stocks’ Technical Trend

Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and

when they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their trend,

expected Fed rate moves and speculative positioning in 10-year Treasury Futures.

{kind=link}

US

Recession Risk Radar

A comprehensive list of economic

indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs. G7 and EM counterparts.

{kind=link}

Get the Score card of all major currency pairs in

terms of Trend, Momentum, Carry, GDP and Current account differential

Precious Metals

Check out where precious metals

stand Trendwise and Breakoutwise. Get a sense of options

(cumulative open interests on calls and puts) and futures traders’ sentiment

(non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the Stock

market correlate with each other and speculative futures positioning on

Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and

rule-based trend following investment approach can serve as an effective

portfolio insurance technique.

To receive a Daily Trend Status

Update and round the clock market and economic instant notifications, join

the free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery

preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio Management and Advisory Services

BentinPartner GmbH is a Swiss registered

independent financial adviser. We offer four different portfolio management

mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an

optimized strategic benchmark. This allocation delivers the “beta” (or markets

related) performance of your portfolio while we seek to generate additional

“alpha” (“skills related) performance with tactical adjustments, using a

predefined maximum “value at risk” envelope. Most of the portfolio’s

performance is derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or benchmark)

and pursues a “total” as opposed to “relative” return objective. With this

mandate, we seek to beat the best of “cash” or of the MSCI World Equity index,

applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage

(not exceeding 100% of NAV). You control the portfolio allocation (which can be

a pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at +41615444310.

We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the list,

please send us an email by clicking here, mentioning “unsubscribe” in

the title.

To ensure that our emails reach

your inbox and not your spam folder, please consider adding Marc.Bentin@BentinPartner.ch,

Marc.Bentin@BentinPartners.ch and our alternate address Bentinpartner@gmail.com

to your safe address book. If you are using Microsoft Outlook, simply right

click on our email address, choose "add to Outlook contacts" and then

"save".

Important Disclaimer

© Copyright by BentinPartner llc. This communication is provided for

information purposes only and for the recipient's sole use. Please do not

forward it without prior authorization. It is not intended as a recommendation,

an offer or solicitation for the purchase or sale of any security or underlying

asset referenced herein or investment advice. Investors should seek financial

advice regarding the suitability of any investment strategy based on their

objectives, financial situation, investment horizon and particular needs. This

report does not include information tailored to any particular investor.

It has been prepared without any regard to the specific investment objectives,

financial situation or particular needs of any person who receives this report.

Accordingly, the opinions discussed in this Report may not be suitable for

all investors. You should not consider any of the content in this report as

legal, tax or financial advice. The data and analysis contained herein are

provided "as is" and without warranty of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss sustained

by anyone who has relied on the information contained in any publication

published by BentinPartner llc. The content and views expressed in this report represents

the opinions of Marc Bentin and should not be construed as guarantee

of performance with respect to any referenced sector. We remind you that past

performance is not necessarily indicative of future results. Although BentinPartner llc

believes the information and content included in this report have

been obtained from sources considered reliable, no representation or warranty,

express or implied, is provided in relation to the accuracy, completeness or reliability

of such information. This Report is also not intended to be a complete

statement or summary of the industries, markets or developments referred to in

the Report.

#fx #forex #investing #markets #riskmanagement

#bankingindustry #finances #money #traders #quants