Monday, July 20, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice week end.

Marc

Bentin

Bentinpartner GmbH

{kind=link}

{kind=link}

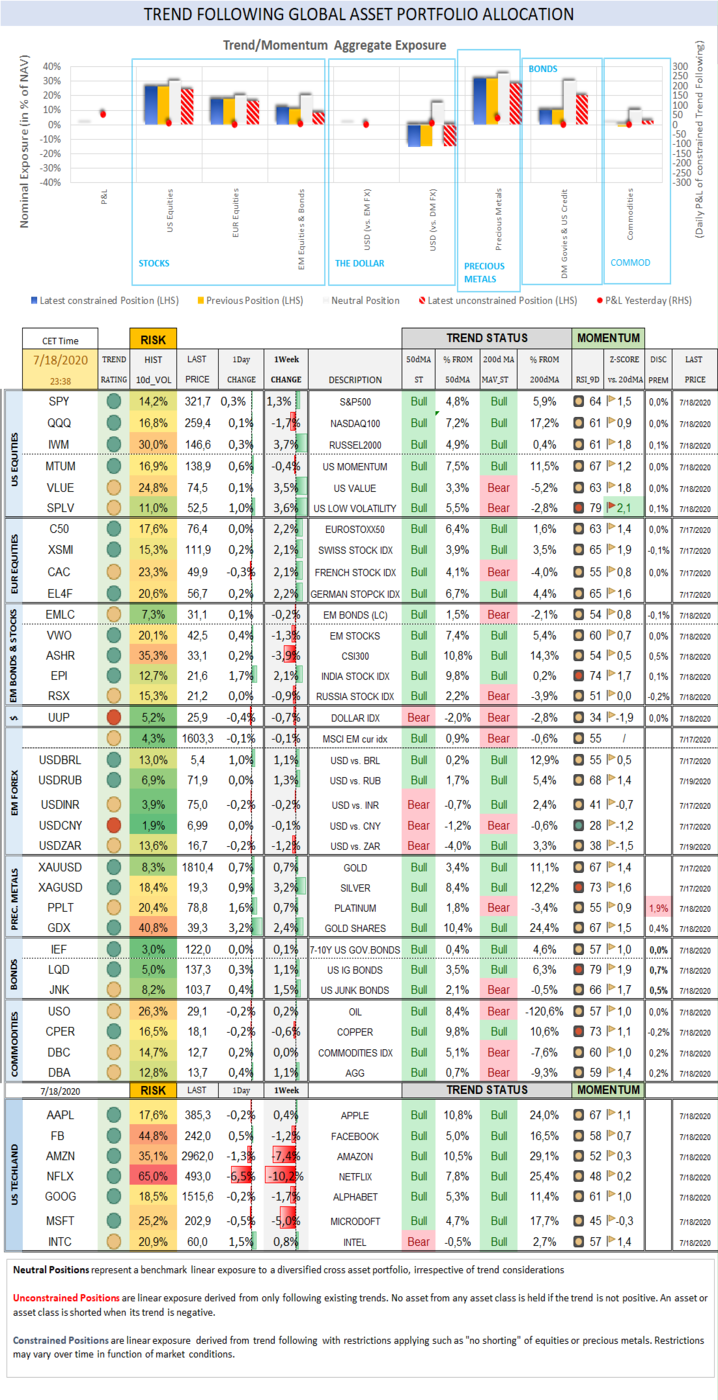

Trend

Status Update

Over the week end and in a pattern that has become familiar, financial

markets chose to ignore the bad news of the unfolding second wave of corona

infections to focus on the imbedded good news resulting from the bad news which

is the prospect of more global central banks and fiscal stimulus.

There was some good news reported with a widening range of potential

vaccines in 2d and 3d stage. It is difficult to report on accumulating evidence

that do not seem to have any lasting market impact but the risks of a second

wave are becoming hard facts. The number of infections around the world hit

13mn, with 1mn added in just five days. WHO warned there would be no return to the

“old normal” for the foreseeable future and that many countries were heading in

the wrong direction. This applied to several key US states such as California,

Texas and Florida that are being forced to partially unwind the reopening of

their economy. There were also some disturbing new revelations that permanent

immunity to the corona may not be possible, jeopardizing vaccine developments with

several international studies indicating that the human body does not retain

the antibodies building up during the infections, meaning serial contamination

are a risk to contend with.

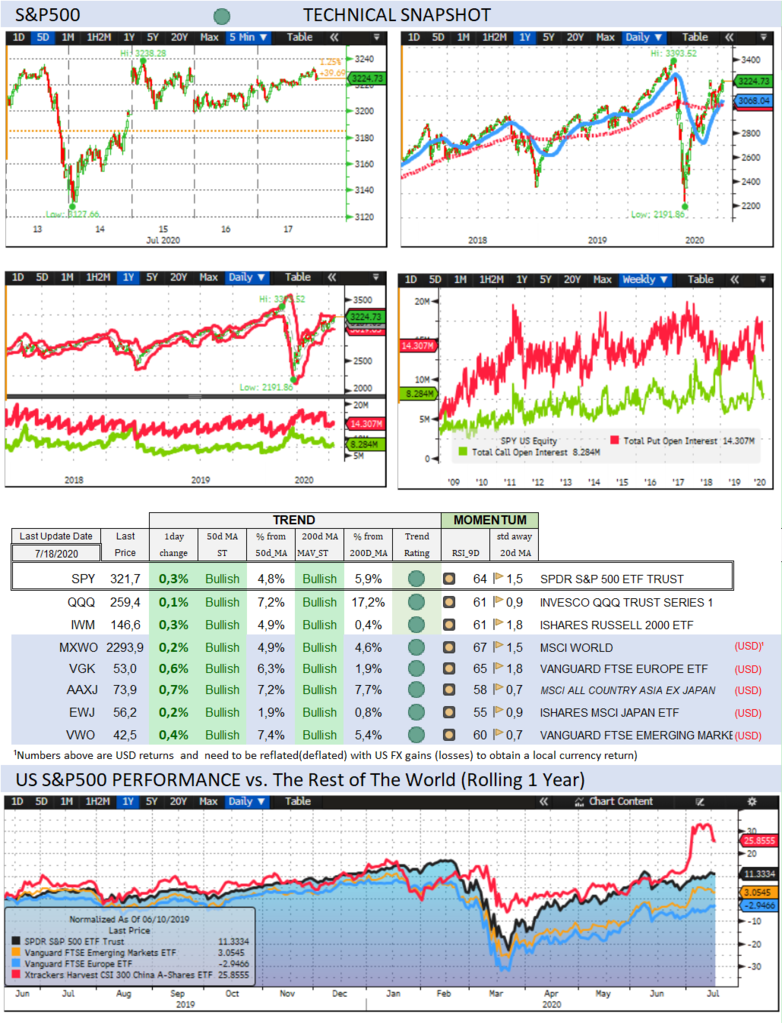

Over the past week, the S&P500 gained 1,3% (0,0% YTD) breaking even

for the year while the Nasdaq100 dropped -1,7% (22,0% YTD). The US small cap

index rallied 3,7% (-11,5% YTD).

While US stocks rose further, there were signs of nervousness with tech

underperforming last week, as Netflix, one of the darlings of “stay at home”

tech names, suffered a 7% correction (reducing its YTD gains to a still comfortable

high double digit gain after new account openings only reached half of Wall Street estimates). The

absurdity of Tesla trading at 350+ times earnings continued nonetheless as short

sellers got and keep getting squeezed. Let’s see what Wednesday brings when the

company reports earnings. Before the company joins the S&P500 it will have

to print four consecutive quarters of profits but the talk is already that the

S&P is ready to make an exception for Tesla. The best time to lighten up on

Tesla (for lack of better word) will be (in our admittedly perma-bear view) when

it enters the S&P. At that point, the hoard (millions) of passive investors

holding their one or two shares at distorted prices… will hold that share at an

insane top plus the 40’000 new account holders at Robin Hood who reportedly added

to their Tesla holdings during a single four-hours span on Monday as well. Smart

money is already lightening up on tech and these new holders will have no

lasting power when the correction genuinely starts…(imho).

Last week’s Banks results were mixed with large loan loss provisions contrasting

with an explosion in investment banking results (for those banks involved in

this activity).

Another illustration that markets have become detached from reality came

with loss making “small caps” now outperforming money making ones by a large margin. “As insolvency risk subsides, investors have flocked

to unprofitable companies. As of the end of last year, 38% of Russell 2000

constituents were losing money. Since the market’s trough in March, their

stocks have rallied about 79% on average. That compares with 47% for those that

are profitable.”, Bloomberg wrote.

CBOE Volatility Index sold off by -5,9% (86,4% YTD) to 25,68.

The Eurostoxx50 rallied 2,2% (-8,2%), outperforming the S&P500 by 0,9%.

Diversified EM equities (VWO) dropped -1,3% (-4,4%), underperforming the

S&P500 by-2,6%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies dropped -0,7% (-0,2%) turning the dollar red for the year while the

MSCI EM currency index (measuring the performance of EM currencies vs. the USD)

dropped -0,1% (-3,7%).

The US Federal deficit incurred its largest monthly deficit in history

reaching USD864mn in June, exceeding most “annual” deficits of the nation’s

history. The 12month deficit came at 14% of GDP last month (beating the second

largest 10.1% deficit of February 2010). That is without counting the new round

of emergency stimulus being discussed by Congress and the White House at the

moment. Technically, although EM currencies had a rough week, the Dollar index further

weakened technically last week. Ray Dalio and Hugh Henry gave two recent interesting interviews on why they

think the dollar is set to fall. We share their view that FX volatility is too

low and set to rise.

10Y US Treasuries rallied -2bps (-129bps) to 0,63%. 10Y Bunds climbed

2bps (-26bps) to -0,45%. 10Y Italian BTPs rallied -6bps (-24bps) to 1,17%, outperforming

Bunds by -4bps.

The number of Americans filing for jobless claims last week rose more

than expected (+1.3mn last week, the 17th straight week when jobless

claims rose more than 1mn). American Airlines warned it could furlough up to

29% of their workforce (while some others reported a larger 50% planned job

cuts).

There was intensifying talks of the Fed contemplating some anchoring of

the yield curve, not least supported by former Fed Chairmen B. Bernanke and J.

Yellen.

US High Yield (HY) Average Spread over Treasuries dropped -41bps (220bps)

to 5,56%. US Investment Grade Average OAS dropped -7bps (40bps) to 1,41%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -3bps

(19bps) to 0,71%.

Gold gained 0,4% (19,2%) while Silver continued to catch up adding 1,4%

(8,4%). Major Gold Mines (GDX) rallied 2,4% (34,3%). The slow grind higher in

precious metals seems relentless. An interesting development emerged with

investors in the gold futures market, reducing positions (some brokers also

suspended trading in the gold emini future that

allows to trade a smaller size than the full CME contract due to dwindling open

interest and rising illiquidity) while investors continued to expand physical

gold hoarding, suggesting a shift in the balance of power in the gold market.

Gold ETF holdings rose to their highest level ever exceeding 3’000 tons while

Gold in dollars still traded (for a little while) below its all-time highs.

Goldman Sachs Commodity Index gained 0,2% (-30,1%). WTI Crude gained

1,1% (-33,6%).

Over the week end…

After EU Leaders argued on how to roll out their recovery fund of

EUR750bn. European Council President floated a proposal reducing handouts to EUR400bn

(from EUR500bn originally). Dutch and Austrian Prime Ministers rejected

the new offer, standing by a pledge to limit grants to EUR350bn.

Some polls are showing Biden leads by 14%...which had D. Trump irate…and

branding polls showing him trailing as "fake". "Biden can't put

two sentences together," Trump said when he was told about the poll. "They

wheel him out. He goes up – he repeats – they ask him questions. He reads a

teleprompter and then he goes back into his basement." Ugly enough not to

relate what he said next….

Overnight action

Ø Nikkei -0.3%;

CSI300 +1%; S&P500 -11 points

Ø Three Tech IPO’s stocks debuts soared (some of them

more than 200%) in China overnight.

Ø Export data in Japan declined -26.2% in June (vs.

-24.7% expected) while imports dropped -14.4% (from -17.6% expected).

Next week…

Ø IBM will report on Monday and Tesla on Wednesday

Trend Score Card

Click here for

technical terminology.

{kind=link}

US

& International Equities

Check out US and International Stocks’ Technical

Trend Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and when

they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their

trend, expected Fed rate moves and speculative positioning in 10-year Treasury

Futures.

{kind=link}

US Recession

Risk Radar

A comprehensive list of

economic indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs. G7

and EM counterparts.

{kind=link}

Get the Score card of all major currency pairs in terms

of Trend, Momentum, Carry, GDP and Current account differential

Precious Metals

Check out where precious

metals stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and futures

traders’ sentiment (non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the

Stock market correlate with each other and speculative futures positioning

on Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and rule-based

trend following investment approach can serve as an effective portfolio

insurance technique.

To receive a Daily Trend

Status Update and round the clock market and economic instant notifications, join the

free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio Management and Advisory Services

BentinPartner GmbH is a

Swiss registered independent financial adviser. We offer four different

portfolio management mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an

optimized strategic benchmark. This allocation delivers the “beta” (or markets

related) performance of your portfolio while we seek to generate additional

“alpha” (“skills related) performance with tactical adjustments, using a

predefined maximum “value at risk” envelope. Most of the portfolio’s

performance is derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or benchmark)

and pursues a “total” as opposed to “relative” return objective. With this

mandate, we seek to beat the best of “cash” or of the MSCI World Equity index,

applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage

(not exceeding 100% of NAV). You control the portfolio allocation (which can be

a pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the recipient's

sole use. Please do not forward it without prior authorization. It is not

intended as a recommendation, an offer or solicitation for the purchase or sale

of any security or underlying asset referenced herein or investment advice.

Investors should seek financial advice regarding the suitability of any investment

strategy based on their objectives, financial situation, investment horizon and

particular needs. This report does not include information tailored to any

particular investor. It has been prepared without any regard to the specific

investment objectives, financial situation or particular needs of any person

who receives this report. Accordingly, the opinions discussed in this

Report may not be suitable for all investors. You should not consider any of

the content in this report as legal, tax or financial advice. The data and analysis

contained herein are provided "as is" and without warranty of any

kind. BentinPartner llc, its

employees, or any third party shall not have any liability for any loss

sustained by anyone who has relied on the information contained in any

publication published by BentinPartner llc. The content and views expressed in this report

represents the opinions of Marc Bentin and should not be construed as

guarantee of performance with respect to any referenced sector. We remind you

that past performance is not necessarily indicative of future

results. Although BentinPartner llc believes the information and content included in

this report have been obtained from sources considered reliable,

no representation or warranty, express or implied, is provided in relation to

the accuracy, completeness or reliability of such information. This Report is

also not intended to be a complete statement or summary of the industries,

markets or developments referred to in the Report.

#fx #forex #investing #markets

#riskmanagement #bankingindustry #finances #money #traders #quants