Monday, December 02, 2019

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice week end.

Marc

Bentin

{kind=link}

{kind=link}

{kind=link}

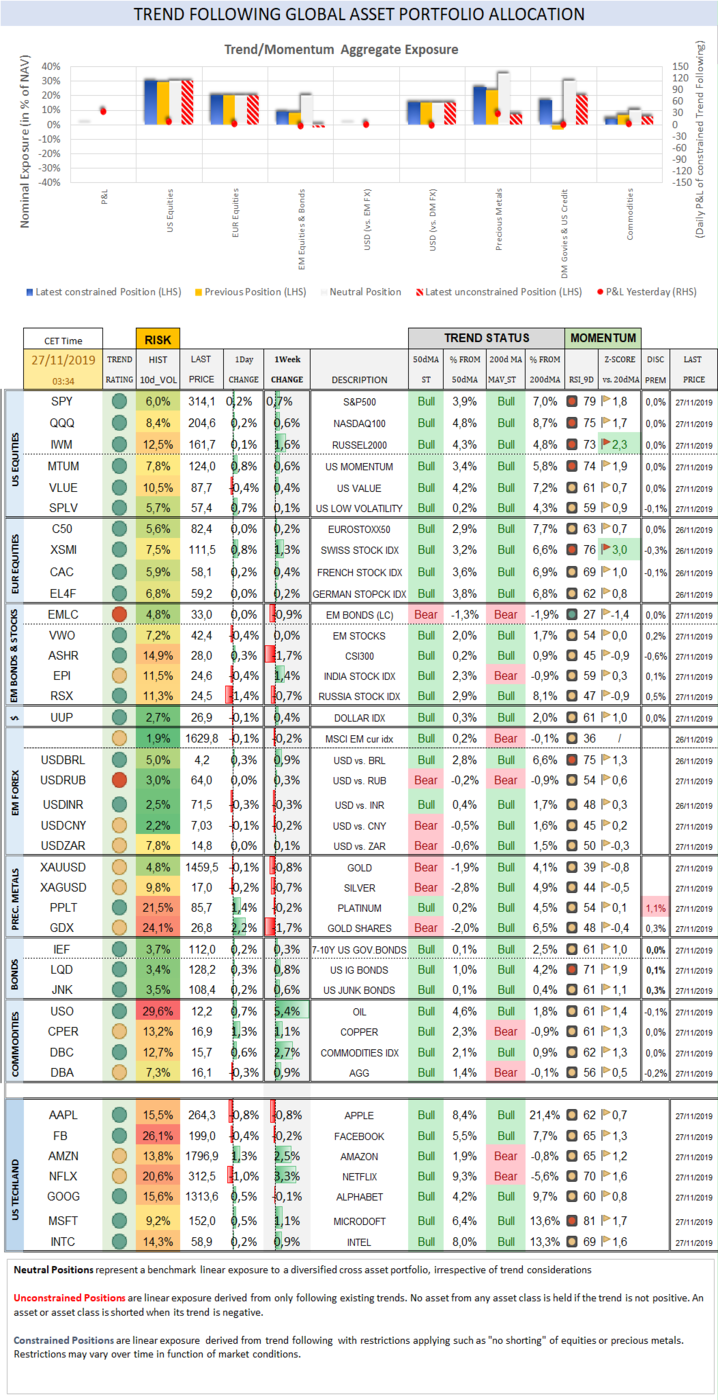

Trend

Status Update

The Eurostoxx50 gained 0,6% (26,3%), underperforming the S&P500

by-0,7%. Diversified EM equities (VWO) dropped -0,6% (10,4%), underperforming

the S&P500 by a larger -1,9%. CSI300 Chinese equity index (ASHR) dropped

-1,9% (25,8%) as investors fretted about the deteriorating health of smaller lenders,

their mounting (around 40%) bad debt and liquidity problems as more than 13% of

the 4379 small lenders are now considered “high risk” by the central bank.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies gained 0,3% (5,7%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) dropped -0,1% (1,0%). EURUSD gained

0,1% (-3,9%). EURCHF gained 0,4% (-2,1%). EURJPY gained 0,6% (-4,1%). EURGBP

dropped -0,1% (-5,1%). JPY weakened last week as Japan’s industrial output dropped

-4.2% from the previous month in October and at the fasted pace in one year,

exposing the economy’s decline in domestic and foreign demand. Whilst Japan has

been the trend setter in slashing rates to historical lows coupling those with

QE and as Japan gears up to “reembrace the power of public spending” following

an increase in the sales tax (expectations for a politically motivated fiscal

stimulus in Japan rose from JPY5trn to JPY20trn,

double the largest stimulus enacted after the tsunami of 2011), the previous BoJ Governor Kuroda regretted not to have hiked rates to 1% and admitted

he hated QE. Japan’s economy is expected to shrink by 2.7%

this quarter. This could be a good enough set of reasons (next to the relentless

equity market rally) to question JPY current valuation before that of the USD

going into next year.

10Y US Treasuries dropped 1bps (-91bps) to 1,78%. 10Y Bunds were unchanged

(-60bps) at -0,36%. 10Y Italian BTPs climbed 5bps (-151bps) to 1,23%, matching

Bunds.

US High Yield (HY) Average Spread over Treasuries dropped -21bps

(-156bps) to 3,70%. US Investment Grade Average OAS dropped -3bps (-57bps) to

1,15%. In European credit markets, EUR 5Y Senior Financial Spread dropped -3bps

(-54bps) to 0,57%. EMLC (VANECK JPM EM LOCAL CCY BOND) dropped -0,8% (-0,2%).

Gold gained 0,1% (14,2%) while Silver closed unchanged on the week

(9,9%) after a strong and unexpected metals’ rally on Friday which coincided

with selling on the dollar index. Major Gold Mines (GDX) gained 1,0% on the

week (28,4%).

Goldman Sachs Commodity

Index sold off by -2,3% (7,9%, Z-score -2,6). WTI Crude sold off by -5,8%

(21,5%, Z-score -2,1) with Natgas also blasting off (below its 50d and

200d ma) to the bottom of its Bollinger band.

Over the week end

Asian

shares rose this morning supported by strong Chinese (and Taiwanese) manufacturing

data and Global Times reporting that China wants tariffs to be rolled back as

part of the phase I trade deal with the US. A gauge of China’s manufacturing

sector jumped unexpectedly in November back into expansion (to 50.2 from 49.3) after

a year of contraction and may help validating investor optimism that the global

economic slowdown has bottomed. The non-manufacturing PMI also rose strongly to

54.4 from 52.8 in October, beating the consensus forecast of 53.1. S&P500

+10 points

Sales

on the internet reportedly rose 18%. Today comes “ciber” Monday…in the steps of Black Friday.

US

ISM manufacturing and construction spending are due out today and the job

report on Friday (expected to show non-farm payrolls rose by 190’000 in

November).

D.

Trump will be landing in London today…and B. Johnson must be hoping that the

expected support he will get from the US President will not play in the hands

of J. Corbyn (a recent poll suggested Labour is slowly eating into the

Conservatives’ lead before for Dec. 12’s vote).

Trend Score Card

Click here for technical annotations.

{kind=link}

{kind=link}

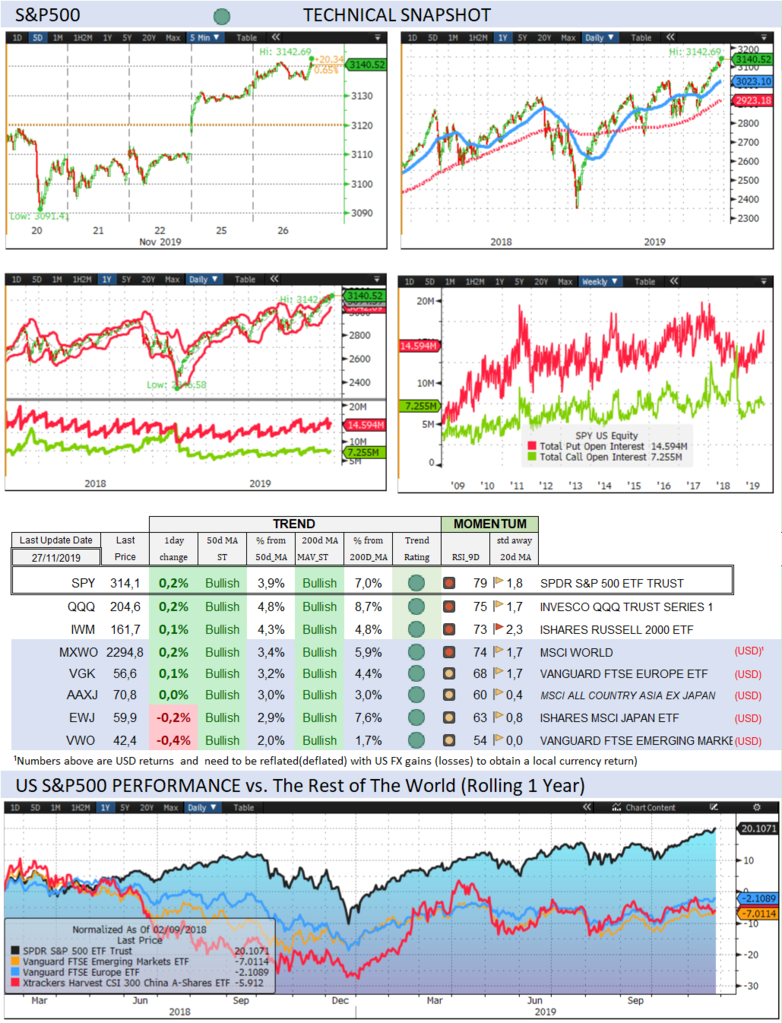

US

& International Equities

Check out US and International Stocks’ Technical Trend

Status.

{kind=link}

Sector

Trend & Momentum (revised)

Check out equity sectors’ trend and performance …and

when they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their trend,

expected Fed rate moves and speculative positioning in 10-year Treasury Futures.

{kind=link}

US Recession

Risk Radar

A comprehensive list of economic

indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs. G7 and EM counterparts.

{kind=link}

Precious Metals

Check out where precious metals

stand Trendwise and Breakoutwise. Get a sense of options

(cumulative open interests on calls and puts) and futures traders’ sentiment

(non-commercials open positions).

{kind=link}

Why Trend Following Matters and How It Can Help

You?

The last months of 2018 illustrated

how fast and furious markets can fall. Trend following offers guidance as to

when to join and when to leave an asset class with changing trend

characteristics. A disciplined and rule-based trend following investment approach

can serve as an effective portfolio insurance technique. Our purpose, beyond

tracking economic, political and monetary developments is to assist readers

investing in global markets with a keen focus on trend formation covering all

important asset classes.

To receive a Daily Trend Status

Update and much more, join a

free trial of our premium research.

To learn more about our premium research:

https://www.bentinpartners.ch/research

Feel free to join our free trial and choose your delivery

preferences:

https://www.bentinpartners.ch/subscribe

Please visit our web site or call us at +41615444310.

We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the list,

please send us an email by clicking here, mentioning “unsubscribe” in

the title.

To ensure that our emails reach

your inbox and not your spam folder, please consider adding Marc.Bentin@BentinPartner.ch,

Marc.Bentin@BentinPartners.ch and our alternate address Bentinpartner@gmail.com

to your safe address book. If you are using Microsoft Outlook, simply right

click on our email address, choose "add to Outlook contacts" and then

"save".

Important Disclaimer

© Copyright by BentinPartner llc. This communication is provided for

information purposes only and for the recipient's sole use. Please do not

forward it without prior authorization. It is not intended as a recommendation,

an offer or solicitation for the purchase or sale of any security or underlying

asset referenced herein or investment advice. Investors should seek financial advice

regarding the suitability of any investment strategy based on their objectives,

financial situation, investment horizon and particular needs. This report does

not include information tailored to any particular investor. It has been

prepared without any regard to the specific investment objectives, financial

situation or particular needs of any person who receives this report.

Accordingly, the opinions discussed in this Report may not be suitable for

all investors. You should not consider any of the content in this report as

legal, tax or financial advice. The data and analysis contained herein are

provided "as is" and without warranty of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss sustained

by anyone who has relied on the information contained in any publication

published by BentinPartner llc. The content and views expressed in this report represents

the opinions of Marc Bentin and should not be construed as guarantee

of performance with respect to any referenced sector. We remind you that past

performance is not necessarily indicative of future results. Although BentinPartner llc

believes the information and content included in this report have

been obtained from sources considered reliable, no representation or

warranty, express or implied, is provided in relation to the accuracy,

completeness or reliability of such information. This Report is also not

intended to be a complete statement or summary of the industries, markets or

developments referred to in the Report.

#fx #forex #investing #markets

#riskmanagement #bankingindustry #finances #money #traders #quants