Monday, February 10, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice week and good luck.

Marc

Bentin

Bentinpartner GmbH

{kind=link}

{kind=link}

Trend

Status Update

Some analysts argued that, at least semantically, the corona virus is

not a Black Swan because an outbreak of some sort was inevitable and

predictable, not fitting the definition of “unknown unknown” of unquantifiable

consequences. We are no specialist in epidemiology and won’t improvise

ourselves as such. As everybody else, we look at the number of casualties going

up and spreading, hoping that the vaccine and containment measures in China and

elsewhere will prove effective. In the meantime, the official death toll

surpassed that of SARS (at 813), new cases were confirmed outside of China and

the massive release of sulfur dioxide gas from the

outskirts of Wuhan suggested that the official tally may be underestimated. It

is the passing away of Dr Li, a 34 year old medical doctor (who became famously

popular as a whistle blower of the disease outbreak) last week that elevated

concerns (I noticed people crossing the street as a child coming in the

opposite direction was coughing in Basel yesterday to reflect on the mounting

worldwide paranoia) but not sufficiently to unsettle the sentiment on Wall

Street which remained focussed on Tesla going off chart, reasonably good

earnings and economic reports (Friday’s US job report came in better than

expected) and the overwhelming impression that the Central Banks’ put remains

firmly in place. What made the situation highly unusual last week was a feeling

of dual panic. On the one hand, the possible spreading of the disease and of

its economic consequences (China is now 18% of World GNP from 5% in 2003 with a

world economy much more dependent on Chinese exports for its supply chain with 170mn

Chinese travellers criss-crossing the world, more than 10 times their numbers

at the time of the SARS outbreak) had many worried. On the other hand, the

impossibility of getting any correction on any bad news froze the blood of

shorts and those under weighed in risky assets. Perhaps, if a Black Swan does

not scare anyone, the Grey Rhino getting at us with a highly probable big

impact ultimately will... For the

moment, the only vaccine comes from the Fed’s “non-QE”.

Elsewhere in US politics, the debacle of the Iowa Primaries was a real

blow for Democrats in general (allowing D. Trump to clamour something to the

tune that if Democrats cannot handle a primary, their management of the country

would be even worse) and for J. Biden, in particular. If J. Biden stumbles next

week in New Hampshire (as is likely), M. Bloomberg might still emerge as the

sole credible alternative to D. Trump. In our view, Sanders is the Corbyn of US

politics and E. Warren, a “socialist” under the influence of deep French accent

socialist ideologues à la Picketty (whose arrogance

on Bloomberg TV last week was off the chart) who will come as a liability for

her. Mocking Pete Buttigieg for his (German)

unpronounceable name was not strikingly courteous from D. Trump but it won’t

help him for sure (Issur Danielovitch

Demsky became more popular when he changed his name

to Kirk Douglas). Neither will his lack of following among the black community

or his gender preferences. Baring a miraculous comeback of J. Biden, (the

latest poll shows Sanders and Buttigieg leading with 28% to 21% over J. Biden

and E. Warren coming in third and fourth with 12% and 9%, respectively), “mini”

(as mocked by D. Trump) Bloomberg could well end up drawing the long straw as

the ultimate challenger to D. Trump whose support, according to Gallup’s most

recent poll, stands at a rather exceptional 49%.

Mike Pompeo went to Belorussia last week, suggesting that the US could

sell oil to the country. Nobody listened, too busy with the corona virus and

the Tesla squeeze. V. Putin did not

respond to the provocation either.

One of the remaining investment themes (along with the value proposition

of EM markets that was placed back on the shelter for now) remains “sustainable

and green” investing. So, we decided to look into this theme (beyond taking

public transportation, scrapping plastic bags in our shopping, switching to

heat pumps and waiting for an attractive and still affordable enough suggestion

to replace our history filled and still perfectly running German 13-year-old

diesel car) to tilt our investment strategy towards greener. In our search we started screening for ETF’s

focussed on that theme and what we found first was four letter word ETF of

which the AUM more than doubled since January and was multiplied by 10 since

last September, now totalling more than USD7bn. We were a little puzzled to see

this ETF paying less than 1% dividend compared to the slightly less mediocre

1.7% available on the S&P500. But who needs an old-fashioned dividend these

days? Investing in this ETF is for good cause anyway and an act of philanthropy

from those managing other people’s money. What unsettled us more was to see

that the top holdings of this ETF were the exact same Microsoft, Apple, Amazon,

Facebook, Alphabet composing the top holdings of the S&P500 of which the

performance is driven, for the most part, by the same four or five names. We

have no problem with any of those specifically, nor with the fact that the same

old names that drive demand into US markets should drive what has become an

exploding demand for “green investing” vehicles or managers, just as if any of

these names should be seriously associated with green investing. For what it is

worth what currently drives growth for “all” of these companies (with the

exception perhaps of Apple) is the cloud business which is a heavily carbonated

activity serving the purpose of storing -for the most part- old pictures and

emails for over 15 years, in an exponentially rising fashion (including for the

people that have passed away). Most of this data is stored on millions of

electricity consuming servers that are cooled with fresh waters from the

oceans, actively contributing to warm up the oceans, heat up and disrupt the

climate, for the sole purpose of having robots parse every mail that we write,

remember links that we click to serve our internet experience with tailor made

ads that we neither want, nor need, nor can get rid of and in violation of our

privacy rights (except of course that we keep signing disclaimers that discharge

anybody of being accused to do so).

Even Microsoft which outsmarts most in its peers in its investors’ communication

strategy, vowed to become carbon “negative” by 2030 and to take back all the

CO2 that it produced since its creation by 2050. That is a very laudable

intention. But the way it will work is mostly through “replacement” by planting

trees in compensation for the CO2 emitted. Should everybody decide to proceed

the same way, we will run out of arable land soon to plant those trees…

Every problem should be taken and treated at its root.

Developing the cloud, as all these companies, sold to us as being

“green”, are now doing is not the long-term solution. There are many reasons to

want to buy these names (Trump twitter feed pushing up the S&P at any

downturn (and upturn), trend, momentum, buy backs and rates heading to zeros

being the main ones) but there is no need to add a “green label” to them so as

to also give investors a good conscience on a less than convincing argument.

The solution is to change/force people’s behaviour in their every day’s life

(even if you delete your emails diligently somebody might store them somewhere

for some reasons but you can delete the pictures or better store then on one or

two hard drives at homes that do no harm) not in buying an ETF filled with

names that earned a green label only too often for the merit of not being a car

or oil related company. In some ways, it is just another way of feeding Wall

Street, twisting markets and fuelling … “just” bubbles with the manipulation of

the masses rather than addressing the problem at its core.

This of course did not close our search for truly green stocks…

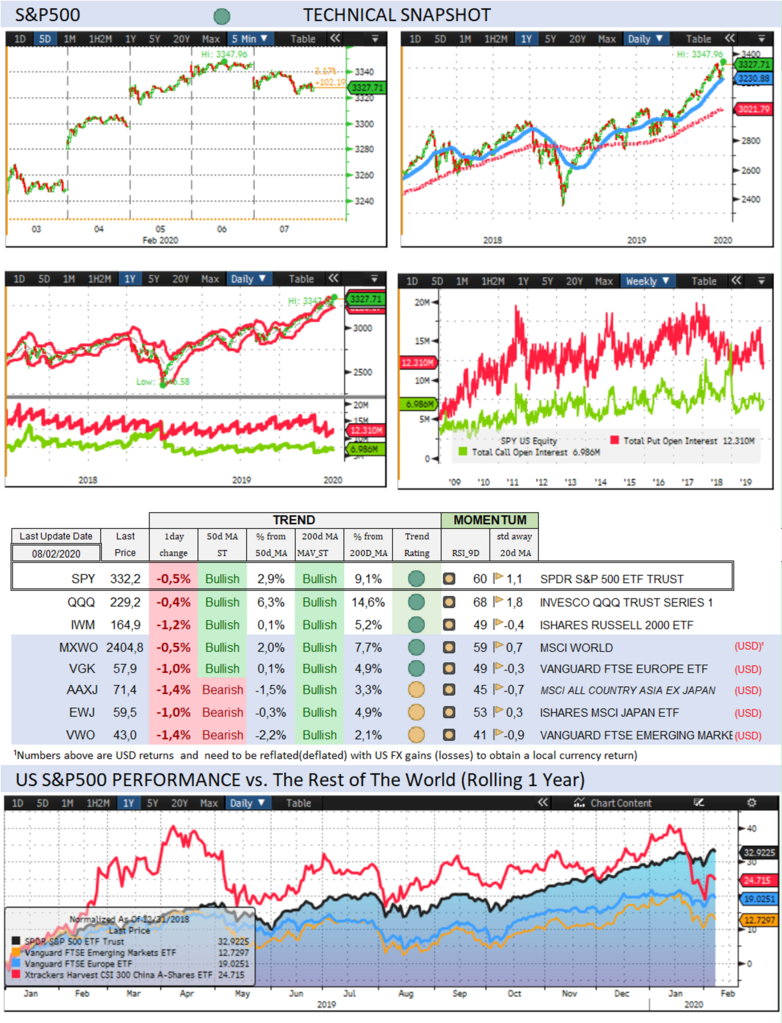

Over the past week, the S&P500 rallied 3,3% (3,2% YTD) while the

Nasdaq100 rallied 4,6% (7,8% YTD). The US small cap index rallied 2,7% (-0,5%

YTD). CBOE Volatility Index sold off by -17,9% (12,3% YTD) to 15,47. AAPL rallied

3,4% (9,0%). FB rallied 5,2% (3,4%).

LYFT rallied 5,1% (16,0%, Z-score 2,2). AMZN rallied 3,5% (12,5%). NFLX rallied

6,3% (13,4%). GOOG rallied 3,1% (10,6%). MSFT rallied 8,0% (16,6%, Z-score 2,0). INTC

rallied 3,3% (10,3%). IBB (ISHARES NASDAQ BIOTECHNOLOGY)rallied

6,8% (0,8%).

The Eurostoxx50 rallied 4,5% (2,0%), outperforming the S&P500 by

1,3%.

Diversified EM equities (VWO) recovered 2,2% (-3,4%), outperforming the

S&P500 by -1,0%.

The Dollar DXY Index (UUP)

measuring the USD performance vs. other G7 currencies gained 1,4% (2,7%,

Z-score 2,2) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) dropped -0,2% (-1,3%). EURUSD dropped -1,3% (-2,4%,

Z-score -2,1).

10Y US Treasuries underperformed with yields rising 8bps (-33bps) to

1,58%. 10Y Bunds climbed 5bps (-20bps) to -0,39%. 10Y Italian BTPs climbed 1bps

(-47bps) to 0,94%, matching Bunds.

US High Yield (HY) Average Spread over Treasuries dropped -36bps (18bps)

to 3,54%. US Investment Grade Average OAS dropped -7bps (5bps) to 1,06%. In

European credit markets, EUR 5Y Senior Financial Spread dropped -5bps (-3bps)

to 0,49%.

Gold dropped -1,2% (3,5%) while Silver dropped -1,9% (-0,8%). Major Gold

Mines (GDX) sold off by -3,7% (-4,6%).

Goldman Sachs Commodity Index dropped -0,8% (-11,6%). WTI Crude sold off

by -2,4% (-17,6%).

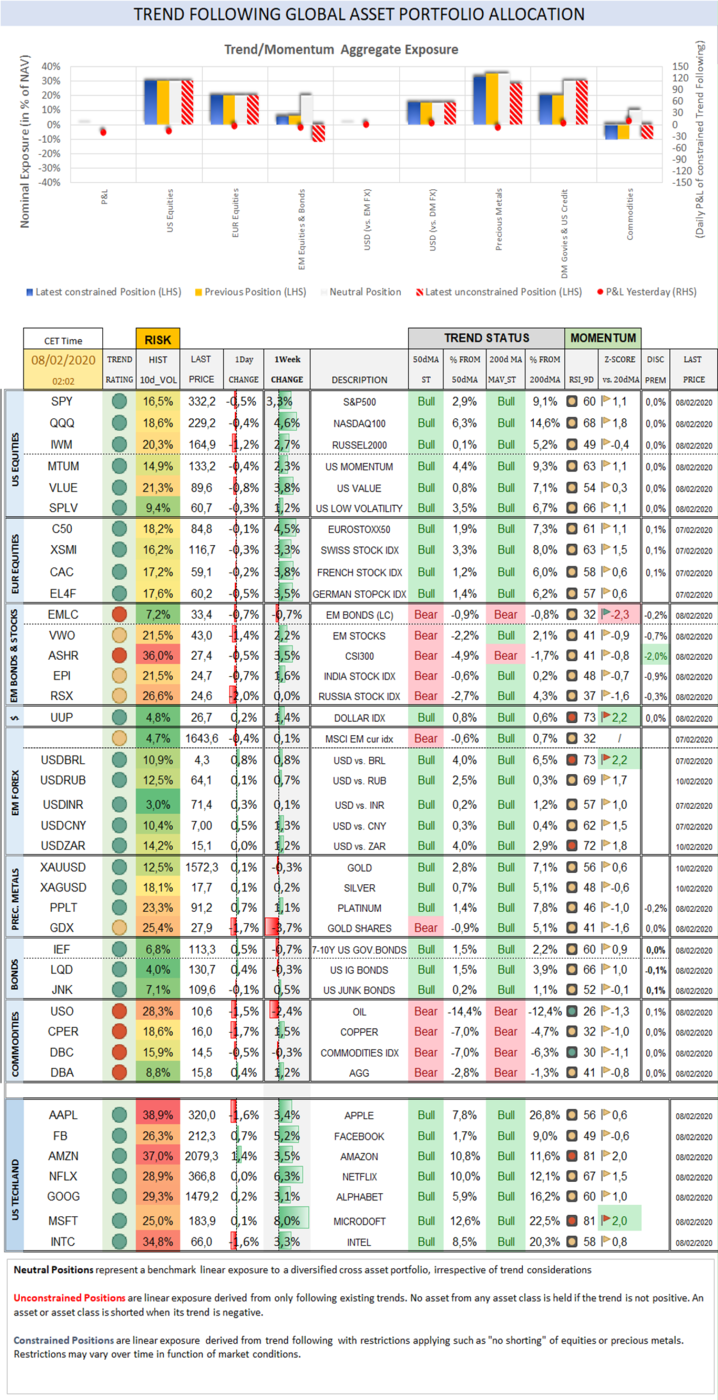

Trend Score Card

US

& International Equities

Check out US and International Stocks’ Technical

Trend Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and when

they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their

trend, expected Fed rate moves and speculative positioning in 10-year Treasury

Futures.

{kind=link}

US Recession

Risk Radar

A comprehensive list of

economic indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs. G7

and EM counterparts.

{kind=link}

Precious Metals

Check out where precious

metals stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and

futures traders’ sentiment (non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the

Stock market correlate with each other and speculative futures positioning

on Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and rule-based

trend following investment approach can serve as an effective portfolio

insurance technique.

To receive a Daily Trend

Status Update and round the clock market and economic instant notifications, join

the free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery preferences:

https://www.bentinpartners.ch/subscribe

Portfolio Management Services

BentinPartner GmbH is a

Swiss registered independent financial adviser. We offer four different

portfolio management mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an

optimized strategic benchmark. This allocation delivers the “beta” (or markets

related) performance of your portfolio while we seek to generate additional

“alpha” (“skills related) performance with tactical adjustments, using a

predefined maximum “value at risk” envelope. Most of the portfolio’s

performance is derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or

benchmark) and pursues a “total” as opposed to “relative” return objective.

With this mandate, we seek to beat the best of “cash” or of the MSCI World

Equity index, applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage

(not exceeding 100% of NAV). You control the portfolio allocation (which can be

a pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the

recipient's sole use. Please do not forward it without prior authorization. It

is not intended as a recommendation, an offer or solicitation for the purchase

or sale of any security or underlying asset referenced herein or investment

advice. Investors should seek financial advice regarding the suitability of any

investment strategy based on their objectives, financial situation, investment

horizon and particular needs. This report does not include information tailored

to any particular investor. It has been prepared without any regard to the

specific investment objectives, financial situation or particular needs of any

person who receives this report. Accordingly, the opinions discussed in

this Report may not be suitable for all investors. You should not consider any

of the content in this report as legal, tax or financial advice. The data and

analysis contained herein are provided "as is" and without warranty

of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss

sustained by anyone who has relied on the information contained in any

publication published by BentinPartner llc. The content and views expressed in this report

represents the opinions of Marc Bentin and should not be construed as

guarantee of performance with respect to any referenced sector. We remind you

that past performance is not necessarily indicative of future results. Although

BentinPartner llc believes

the information and content included in this report have been obtained from

sources considered reliable, no representation or warranty, express or

implied, is provided in relation to the accuracy, completeness or reliability

of such information. This Report is also not intended to be a complete

statement or summary of the industries, markets or developments referred to in

the Report.

#fx #forex

#investing #markets #riskmanagement #bankingindustry #finances #money #traders #quants