Sunday, November 03, 2019

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice week end.

Marc

Bentin

{kind=link}

{kind=link}

{kind=link}

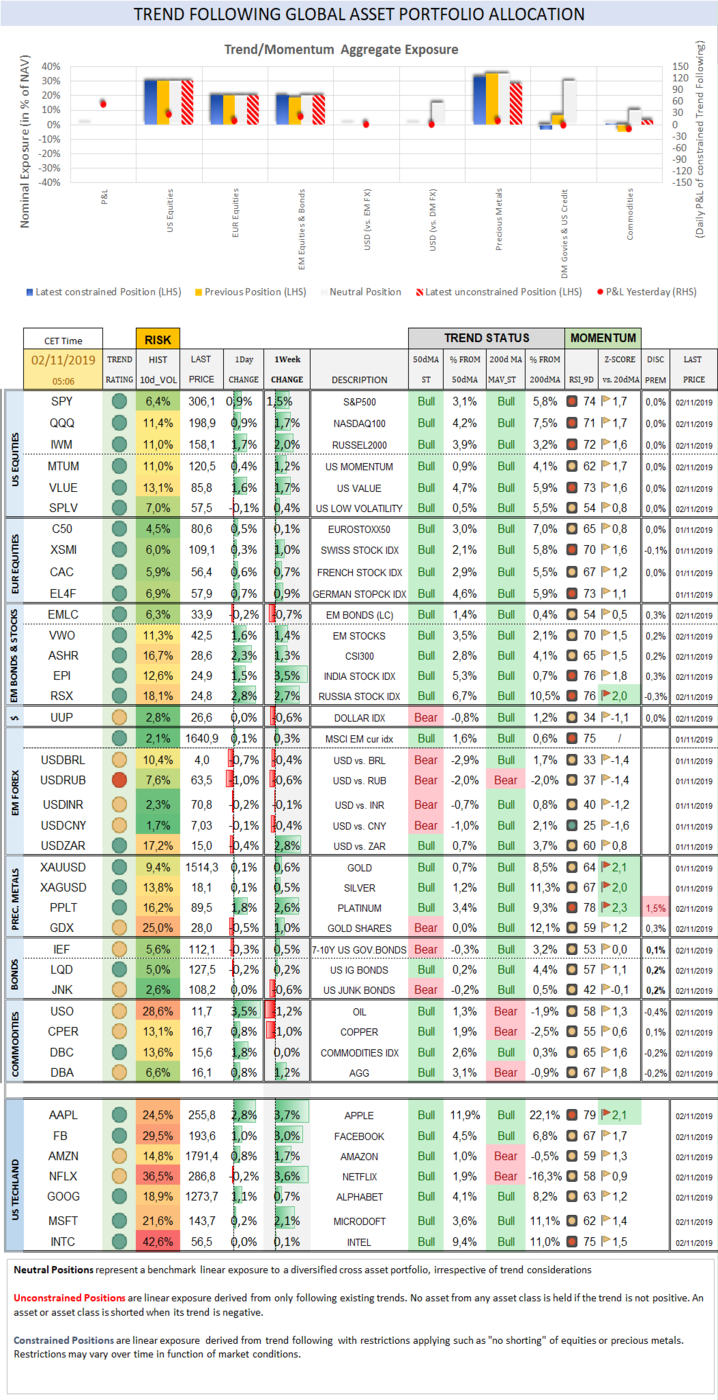

Trend

Status Update

Apple, Microsoft and FB posted a solid (further) rally, supported by

good earnings reports. The latest global equity rally is taking place in low

volumes with investors still largely reluctant to embrace it amidst economic

and political uncertainties (impeachment proceedings). AAPL rallied 3,7% (62,2%, Z-score 2,1); MSFT rose 2,1% (41,5%)

and FB rallied 3,0% (47,7%). The US small cap index gained 2,0% (18,1% YTD).

Semis were extremely strong as well with XSD (SPDR S&P SEMICONDUCTOR ETF) rallied 5,6% (49,5%,

Z-score 2,6). Biotech XBI (SPDR

S&P BIOTECH ETF) rallied 2,8% (16,6%) and IBB (ISHARES NASDAQ BIOTECHNOLOGY

+4,0% (13,9%), suggesting that last Friday was also a grab for beta with

investors loading tactically on some highest beta sectors in an effort to catch

up for lost time. CBOE Volatility Index dropped -2,8% (-51,6% YTD) to 12,3.

The Eurostoxx50 added 0,1% (23,4%), underperforming the S&P500 by

-1,4%. Diversified EM equities (VWO) gained 1,4% (11,5%), outperforming the

S&P500 by -0,1%. CSI300 Chinese equity index (ASHR) gained 1,3% (30,2%),

still leading the way this year behind Russian shares (RSX) which rallied 2,7% (32,0%, Z-score

2,0). Investors grabbed the chance to take part in China’s largest

convertible bond sale (Shangai Pudong Development

Bank) oversubscribing 330 times an issued amount of USD7bn.

The Dollar DXY Index (UUP) dropped -0,6% (4,4%) while the MSCI EM

currency index (measuring the performance of EM currencies vs. the USD) gained

0,3% (1,6%). USDBRL dropped -0,4% (2,8%). USDRUB dropped -0,6% (-8,4%). USDMXN

gained 0,3% (-2,7%). USDINR dropped -0,1% (1,5%). USDCNY dropped -0,4% (2,3%).

USDZAR rallied 2,8% (4,8%). Doubts about the merits of negative interest rates

are becoming more pressing. ECB Vice President Louis de Guindos joined a

growing contingent of officials at the ECB and other central banks starting to

worry about the side effects (by way of misallocating capital, fuelling bubbles

that foster potential instability, enriching the few and mining pension funds

of all). The more rates stay where they are (they will unfortunately) the more

MMT will become a necessity and a self-defeating mechanism for economic freedom

and capitalism with far reaching consequences, in our view. Sweden for one said

last week it was eager to get rid of negative rates altogether with Riksbank Governor S. Ingves reiterating

that it’s likely that the Swedish central bank will raise the repo rate in

December.

AUDUSD recovered 1,2% (-2,1%), encouraged by risk appetite, favourable

Chinese data and the firming up of the bearish dollar set up (DXY dropped below

its 50dma and 200dma just as EM FX broke in bull trend with the exact opposite

configuration.

10Y US Treasuries rallied -8bps (-97bps) to 1,71%. 10Y Bunds dropped

-2bps (-62bps) to -0,38%. 10Y Italian BTPs climbed 4bps (-175bps) to 0,99%,

underperforming Bunds by 4bps. US

Investment Grade Average OAS climbed 2bps (-51bps) to 1,21%. As equities

rallied, high yields sold off in the latter part of the week with the US High

Yield (HY) Average Spread over Treasuries climbing 25bps (-141bps) to 3,85%.

Low tiered US High Yield (HY) Caa Average Spread over

Treasuries fared even worse, climbing + 54bps on the week (-22bps) to 9,67%.

Last week, Federal Government debt reached USD23trn. This is just one of these

numbers except that it increased by USD9.5trn since 2008. As a rule of thumb,

the US Federal debt remains on target to double with each passing 8-year termed

President. This is an unsustainable or rather unbearable path unless bond

yields are driven all the way to zero (which is where D. Trump want them to be)

and the cost of holding debt along with it. The US is going there but Japan

showed the way a while back and Europe is at the forefront now. Several Central

banks are not only obliging but signalling that interest rates won’t be

increased any time soon even if there is a pick-up in inflation (which will be said

to be temporary). In our view the bond bubble is only too obvious and the risks

going forward lie at the periphery of credit markets where investors are piling

up risks (price and investment flows wise) in a gasp for yield.

Precious metals participated in last week’s liquidity push driving Gold 0,6% higher (18,1%, Z-score

2,1) while silver

gained 0,5% (17,0%, Z-score 2,0). Major Gold Mines (GDX) rose 1,0%

(32,8%). Bitcoin gained 7,4% on the week (150,7%), still gradually eroding part

of the 30% gap higher triggered by some misinterpretation of what China plans

to do with its focus on investing in blockchain technology (which has nothing

to do with adopting bitcoins). China does not tolerate bitcoin and likely never

will (nor will it accept libra in all likelihood) but it is vowing to widely

adopt the underlying technology of distributed ledger for other purposes, but

also possibly to introduce a cryptocurrency of its own.

Last week’s market configuration looked suspect and artificial but should not necessarily be fought because

the “data driven” nature of central banks (and government) policies are also

now focussed on preventing equity markets corrections at all costs (a 0.3% drop

on Thursday caused a near panic and an official rush to announce (unaverred)

trade negotiations progress that the Chinese did their best to throw cold water

on. However, there is no point fighting equity markets (D. Trump will do

everything now that he runs the risk to be impeached to drive them higher) and

as always, credit markets will be the judge of how genuine the economic

improvement is. The VC market for unicorns is clogged (hence in our view the

lingering liquidity problems which requires constant daily infusion) and needs

to unclog before an impression of normality can be restored. In that sense, a

further stock market rally would help…

Over the week end

The Trump administration may not need to put tariffs on imported

automobiles later this month after holding “good conversations” with automakers

in the European Union, Japan and elsewhere, Commerce Secretary Wilbur

Ross said. “We’ve had very good conversations with our European friends,

with our Japanese friends, with our Korean friends, and those are the major

auto producing sectors,” Ross said. Last

May in the midst of equity market turmoil, D. Trump had agreed to delay them by

6 months, causing an instant gap higher in major indices. W. Ross also

expressed optimism the U.S. would reach a “Phase One” trade deal with China

this month.

Trend Score Card

Click here for technical annotations.

{kind=link}

{kind=link}

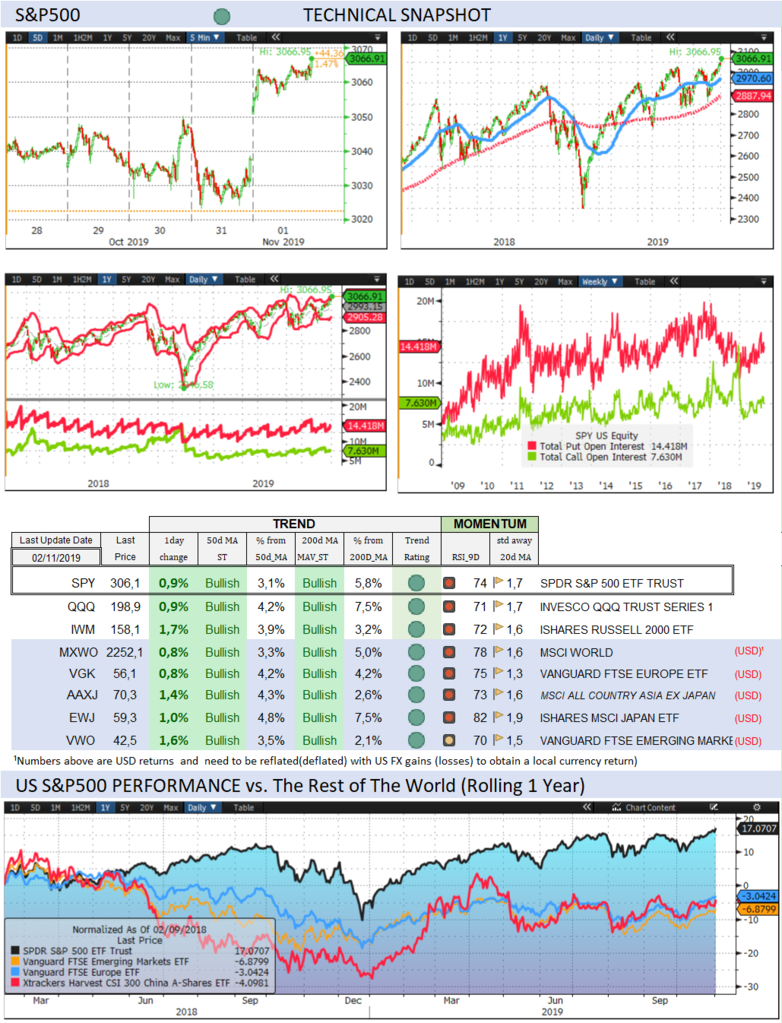

US

& International Equities

Check out US and International Stocks’ Technical

Trend Status.

{kind=link}

Sector

Trend & Momentum (revised)

Check out equity sectors’ trend and performance

…and when they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their

trend, expected Fed rate moves and speculative positioning in 10-year Treasury

Futures.

{kind=link}

US

Recession Risk Radar

A comprehensive list of

economic indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs.

G7 and EM counterparts.

{kind=link}

Precious Metals

Check out where precious

metals stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and

futures traders’ sentiment (non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the

Stock market correlate with each other and speculative futures positioning

on Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

The last months of 2018

illustrated how fast and furious markets can fall. Trend following offers

guidance as to when to join and when to leave an asset class with changing

trend characteristics. A disciplined and rule-based trend following investment

approach can serve as an effective portfolio insurance technique. Our purpose,

beyond tracking economic, political and monetary developments is to assist

readers investing in global markets with a keen focus on trend formation

covering all important asset classes.

To receive a Daily Trend

Status Update and much more, join a

free trial of our premium research.

To learn more about our premium research:

https://www.bentinpartners.ch/research

Feel free to join our free trial and choose your

delivery preferences:

https://www.bentinpartners.ch/subscribe

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the

recipient's sole use. Please do not forward it without prior authorization. It

is not intended as a recommendation, an offer or solicitation for the purchase

or sale of any security or underlying asset referenced herein or investment

advice. Investors should seek financial advice regarding the suitability of any

investment strategy based on their objectives, financial situation, investment

horizon and particular needs. This report does not include information tailored

to any particular investor. It has been prepared without any regard to the

specific investment objectives, financial situation or particular needs of any

person who receives this report. Accordingly, the opinions discussed in

this Report may not be suitable for all investors. You should not consider any

of the content in this report as legal, tax or financial advice. The data and

analysis contained herein are provided "as is" and without warranty

of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss

sustained by anyone who has relied on the information contained in any

publication published by BentinPartner llc. The content and views expressed in this report

represents the opinions of Marc Bentin and should not be construed as

guarantee of performance with respect to any referenced sector. We remind you

that past performance is not necessarily indicative of future

results. Although BentinPartner llc believes the information and content included in

this report have been obtained from sources considered reliable,

no representation or warranty, express or implied, is provided in relation to

the accuracy, completeness or reliability of such information. This Report is

also not intended to be a complete statement or summary of the industries,

markets or developments referred to in the Report.

#fx #forex

#investing #markets #riskmanagement #bankingindustry #finances #money #traders #quants