Please find today’s installment of the Bentin Daily.

Have a nice day ahead.

Marc Bentin

CIO, Bentinpartner GmbH

Wednesday, March 14, 2018

The White House Purge

Continues

US Stocks started

with a Goldilocks jolt higher as the US CPI report showed a monthly gain of

0.2% in line with expectations but much lower than last month’s 0.5% push which

had triggered inflationary and therefore rate hike fears and lower stocks. The

announcement of US Secretary Rex Tillerson being summarily dismissed and to be

replaced by CIA Director Mike Pompeo (who is also the former director of a CIA

prison which practiced torture, according to national French national TV

yesterday and which is totally opposed to Iran’s nuclear deal (this ZH

article is not too engaging),

was all but a diplomatic appointment. The manner by which Tillerson was fired

by a public tweet while he was out in Africa recovering from a bug and mourning

the passing away of his father a few days back, was about as low class a form

of management as we will ever get to see but it was not enough to sour equity

market sentiment in the early going yesterday. As regards the replacement of G.

Kohn as Chief economic advisor, D. Trump said “I’m looking at Larry Kudlow very

strongly”. L. Kudlow is a loyal supporter of D. Trump from day 1 and a lively

character, known so for his opiniated (and unconventional) views as a CNBC

economic commentator.

Despite the early push

higher in US equities, European markets did not pick up that ball and stayed

lower, most likely in response to what looks like an upcoming confrontation

between the US and Europe which, as it appears, is the primary target (along

with China, see politico

article)

of D. Trump’ s protectionist measures. European negotiators and European

politicians reacted with France's Minister of the Economy Bruno Le Maire

telling CNBC on Monday that the EU will join forces with foreign jurisdictions

(China?) to counter the US protectionist and discriminating stance. Germany

likely understands that it needs to play the European card and avoid a too

direct response as this could tempt D. Trump to talk about “bad, really bad

people” again... In any case, Europe is now getting the chance to speak with

one voice and push back on US unilateralism and divide to reign (exceptions to

the tariffs) tactics. Later in the afternoon, the dollar

showed signs of fatigue which pushed the German Dax to end the day, nursing a

2% loss. Leadership from the narrow list of US leading tech shares could not

hold the tape together as tech shares were weakened after D. Trump blocked the

Qualcomm deal, driving its share price down by 5%, dampening appetite for tech

shares more generally. GE also received a thumb’s down from a JPMorgan analyst questioning

the credibility of the company’s profit guidance which also pushed GE share

price into a loss of 4% for the day (to 14.43 with the same analyst expecting

GE share price to further fall to 11).

After being resilient

for most of the day despite weaker European markets, US stocks finally

surrendered to bears towards the close, following a press conference of Tillerson

who saw him appear both exhausted and shaken by emotions. This provided more

evidence of the chaos reigning at the White House and of an accelerating trend to

fire or let experts in their respective fields escape to the benefit of

ideologists close to the thinking of the US President who are unlikely to

contradict him as he starts to focus on mid-term elections. This is of poor

omen ahead of key international negotiations on the economic and geopolitical

front and one that paves the way for more confrontation, possible military

escalation and certainly less diplomacy. These developments are likely to be

toxic for risk appetite.

Gold

which started the day lower recovered and closed slightly higher as equities

and the dollar traded lower. Bonds were generally stronger with yields dropping

4bps on risk aversion and after inflation remained contained.

Dollar developments

offered a mixed picture with dollar liquidity shortage finding (at the same

time as EURUSD rallied) their latest expression in tensions on USD/HKD peg

which traded at the lowest point of its allowed band, triggering corrective

action by the HKMA that said it is fully prepared to take appropriate action if

the USD/HKD exchange rate reaches 7.85.

Nikkei 225

-1%

, S&P500 -7 points

ECB President M. Draghi

is due to speak today with US retail sales and PPI also due out today.

Daily Snapshot

{kind=link}

{kind=link}

{kind=link}

Also

check

Daily Equity Sector Performance

{kind=link}

Risk Appetite+Style Performance+Last

2 weeks intraday

{kind=link}

The News Room

Check

the latest Markets stories…

Leaders,

Laggards & Z-scores

…and

what is breaking out!

(More explanation for Z-scores)

Models Positioning

Please refer to the technical note here for a description on how “implied views” are

defined and monitored and what they mean. In essence, all our views are expressed as a

percent of a global risk budget which is deployed taking into consideration the

volatility of each market exposure prior to translating them into size

positions.

(Explanation for our Implied Views)

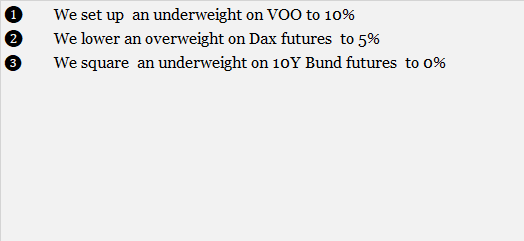

The following changes were

brought to our model portfolios’ positioning (all expressed in % of 10%

independent tracking error; for ex. a 10% overweight in S&P500 means adding

1% independent tracking error on the S&P500):

(Important Methodological Explanation)

Model Positioning

Change and Review:

- We further hedge out our

equity exposure, lifting some bond short as well.

|

FX

Overlay |

Global

Tactical (FX

& Non-FX) |

Our Advisory Services

Our

Investment approach relies on a three-pillar “All Weather” strategy:

- First, we

invest your portfolio in an optimally chosen strategic asset allocation. We do

so focussing on highly liquid and cost-efficient instruments or

first-generation derivatives enabling your portfolio to always remain liquid.

- Then, we

add a layer of tactical management, hedging or emphasizing certain elements of

the strategic asset allocation, drawing on a portfolio specific risk budget.

Our tactical overlay management offers the potential to supplement the

strategic asset allocation return while enabling dynamic hedging in volatile

periods.

- We offer

transparent, professional, tailor-made, and competitive asset management

services, fulfilling our fiduciary duty at all times.

Results and

volatility parameters of strategic balanced Benchmarks in the snapshot picture

above do not constitute a track record. They serve as an indication of what to

expect from a balanced portfolio, passively managed, automatically rebalanced,

diversified and optimized for meeting a “balanced” investment risk profile.

We offer two

types of mandates:

-With a “Global Strategic” (GS) mandate, the chosen benchmark

delivers the portfolio’s “beta” performance while the tactical deviation aims

to deliver some additional “alpha” performance and an “all weather” investment

solution.

-With a

“Global Tactical” (GT) mandate, we consider cash and stocks as dual benchmarks,

undertaking positions solely based on tactical considerations with no core

underlying strategic asset allocation. With both mandates, the potential

maximum risk undertaken at the overall portfolio level is contractually defined

in VAR terms and is a function of the client risk profile and investment

preferences.

Let us help

helping you. Visit our web site or call

us at +41612044665. We’d love to hear from you and see how we can further

assist you.

Bentin Daily PDF Reports Suite

|

|

|

|

|

|

|

|

|

|

|

|

Some

Live Prices

(free

Bloomberg registration required)

|

|

|

|

|

|

|

10Y US Yield |

|

|

|

10Y Bunds |

|

|

|

|

Please visit our web site or call us at +41615444310. We’d love to hear

from you and see how we can further assist you.

Join us on Linked In

To be removed from the list, please send us an

email by clicking here, mentioning “unsubscribe” in the title.

To ensure that our emails reach your inbox and not

your spam folder, please consider adding Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch

and our alternate address Bentinpartner@gmail.com to your safe address book. If

you are using Microsoft Outlook, simply right click on our email address,

choose "add to Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc. This communication is provided for information

purposes only and for the recipient's sole use. Please do not forward it

without prior authorization. It is not intended as a recommendation, an offer

or solicitation for the purchase or sale of any security or underlying asset

referenced herein or investment advice. Investors should seek financial advice

regarding the suitability of any investment strategy based on their objectives,

financial situation, investment horizon and particular needs. This report does

not include information tailored to any particular investor. It has been

prepared without any regard to the specific investment objectives, financial

situation or particular needs of any person who receives this report. Accordingly,

the opinions discussed in this Report may not be suitable for all

investors. You should not consider any of the content in this report as legal,

tax or financial advice. The data and analysis contained herein are provided "as

is" and without warranty of any kind. BentinPartner llc, its employees, or

any third party shall not have any liability for any loss sustained by anyone

who has relied on the information contained in any publication published by

BentinPartner llc. The content and views expressed in this report represents the

opinions of Marc Bentin and should not be construed as guarantee of

performance with respect to any referenced sector. We remind you that past performance

is not necessarily indicative of future results. Although BentinPartner llc

believes the information and content included in this report have been

obtained from sources considered reliable, no representation or warranty,

express or implied, is provided in relation to the accuracy, completeness or

reliability of such information. This Report is also not intended to be a

complete statement or summary of the industries, markets or developments

referred to in the Report.