Monday, April 06, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Please

note that our upload server (in Singapore) is down and that we could not update

files and pictures as a result.

We

created a Dropbox links for Friday’s snapshot and the Global Chartbook.

{kind=link}

Have

a nice week ahead.

Marc

Bentin

Bentinpartner GmbH

Trend

Status Update

After expanding international swap agreements, exchanging USD for

foreign currencies (cross currency swaps now suggest the desired effect was reached), the Fed announced last week a new program

allowing central banks to borrow against Treasuries held in custody at the New

York Fed in a supplementary effort to boost liquidity and prevent further selling

by foreigners of US Treasuries which were reported last week to have dropped by

USD109bn in March (mainly countries dependent on oil exports). This did not prevent the USD to gain further as

concerns remained about EM denominated debt being as high as USD5.8trn and constituting

a so called synthetic short USD position from this part of the world.

{kind=link}

The dollar also gained with more speculative interest (from COMEX) being

wrong footed and outright long EUR since a few weeks ago (after being short) and

now taking the proverbial salon door on their positions (as the euro declined).

On Friday, the US job numbers came much worse than expected with a 701k (from

-100k expected) bringing the unemployment rate to 4.4%. Unemployment for April

is expected to jump to 12%.

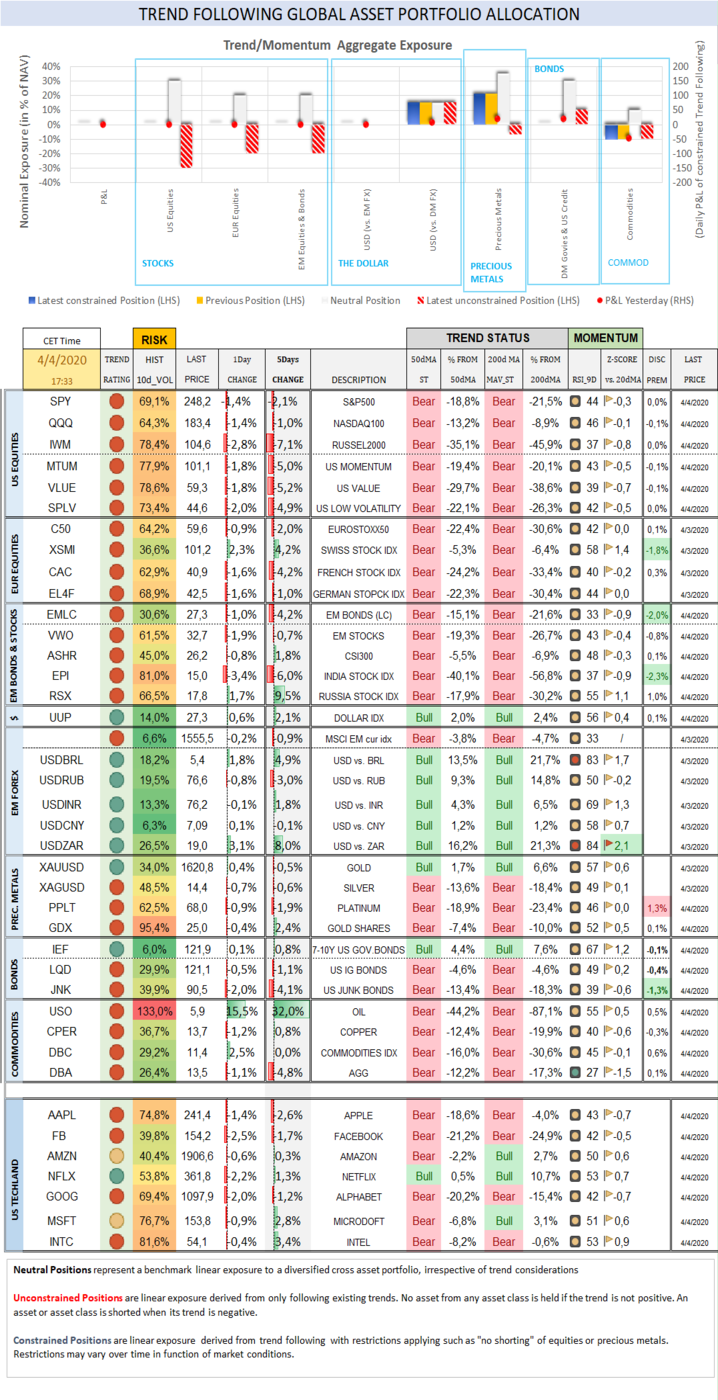

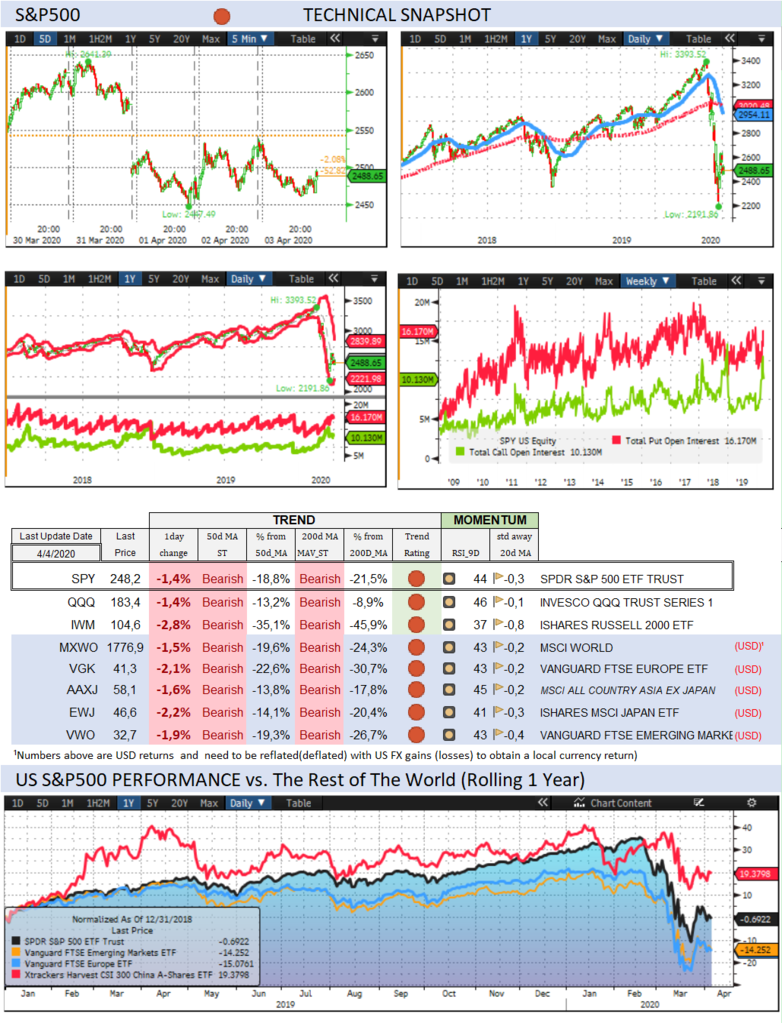

Over the past week, the S&P500 sold off by -2,1% (-22,9% YTD) while

the Nasdaq100 dropped -1,0% (-13,8% YTD). The US small cap index sold off by

-7,1% (-36,9% YTD). CBOE Volatility Index sold off by -28,6% (239,6% YTD) to

46,8.

Tech traded in disperse order. AAPL dropped by -2,6% (-17,8%). FB

dropped -1,7% (-24,9%). LYFT sold off by -20,3% (-48,9%). AMZN gained 0,3%

(3,2%). NFLX gained 1,3% (11,8%). GOOG dropped -1,2% (-17,9%). MSFT rallied

2,8% (-2,5%). INTC rallied 3,4% (-9,6%).

Banks remained the weakest spot along with real estate. XLF (FINANCIAL

SELECT SECTOR SPDR) sold off by -6,5% (-36,2%). EUFN (ISHARES MSCI EUROPE

FINANCIA) sold off by -10,3% (-40,8%). XHB (SPDR S&P HOMEBUILDERS ETF) sold

off by -13,5% (-41,8%). IYR (ISHARES US REAL ESTATE ETF) sold off by -8,5%

(-31,0%).

Airbnb said that its valuation which was last estimated to be worth

USD40bn at the end of last year is now closer to USD26bn, adding that it had

lost USD400mn in the period “preceding” the corona virus outbreak. Some of

these unicorns will never hit the IPO stage and might be months or weeks from an

existential crisis as well. For what it is worth, last week the FT reported

that “some of the most powerful groups on Wall Street are pressing the Trump

administration to allow private equity-owned companies to access hundreds of

billions of dollars in loan funds earmarked for US small businesses hit by the

coronavirus pandemic… Congress last week authorised the Small Business

Administration to dispense $350bn worth of rescue loans to companies with fewer

than 500 workers that have been affected by the coronavirus pandemic.”

On the other hand of the performance spectrum and for a change, energy

outperformed on the back of late last week’s oil price squeeze. RSX (VANECK

RUSSIA ETF) rallied 9,5% (-28,8%). XLE (ENERGY SELECT SECTOR SPDR) rallied 5,3%

(-50,3%). Health care also outperformed; LV (HEALTH CARE SELECT SECTOR) rallied

2,1% (-14,8%).

The Eurostoxx50 dropped -2,0% (-28,4%), outperforming the S&P500 by

0,1%.

Diversified EM equities (VWO) dropped -0,7% (-26,5%), outperforming the

S&P500 by 1,3%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies rallied 2,1% (5,1%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) dropped -0,9% (-6,6%).

EM FX performance was weaker with ZAR trading worst while RUB managed to

gain, supported by a recovery in oil prices on which MXN could not capitalize

however. USDBRL rallied 4,9% (32,9%). USDRUB

sold off by -3,0% (23,6%). USDMXN rallied 7,2% (32,2%). USDINR gained 1,8%

(6,7%). USDCNY dropped -0,1% (1,8%). USDZAR rallied 8,0% (36,0%, Z-score 2,1). EURUSD sold off by

-3,1% (-3,7%).

10Y US Treasuries rallied -8bps (-132bps) to 0,59%. 10Y Bunds climbed

3bps (-26bps) to -0,44%. 10Y Italian BTPs underperformed rising 22bps (14bps)

to 1,55%, underperforming Bunds by 9bps. Morgan Stanley recently estimated the US

deficit will total at least $3.7trn in 2020 and an additional $3trn in 2021, suggesting

a nearly $5trn extra deficit spending in the next two years, financed by the

sale of Treasuries, largely to the Federal Reserve.

US High Yield (HY) Average Spread over Treasuries climbed 21bps (606bps)

to 9,42%. US Investment Grade Average OAS dropped -10bps (173bps) to 2,74% as

intervention pressure intensified. M. El Erian argued

over the week end that Falling Angels (downgrades from investment grade to high

yield) would remain a feature of this crisis as the economy slows and as the

number of credit downgrades has never been that high. This is what the logic of

free markets would dictate but the Fed’s plan to underwrite credit markets has

changed all that and the last thing the Fed wants is to see a further deterioration

in these markets. Recent Flows and the price action on LQD (IG investment grade

ETF) best illustrated the safeguarding efforts of the Fed and the squeeze it enacted on this ETF that was on the verge of failing after trading with

a discount as large as 7% to NAV, with investors trying to hedge or speculate on

the risk that M. El. Erian highlighted.

In European credit markets, EUR 5Y Senior Financial Spread climbed 19bps

(79bps) to 1,31%.

Gold dropped -0,5% (6,8%) while Silver dropped -0,6% (-19,4%). Major

Gold Mines (GDX) rallied 2,4% (-14,8%).

Goldman Sachs Commodity Index rallied 4,8% (-37,9%). WTI Crude rallied

31,8% (-53,6%). DBA (INVESCO DB AGRICULTURE FUND)sold off by -4,8% (-18,8%).

Over the week end…

After rallying more than 30% from their lows late last week, oil retreated

by 6% (also taking MXN down with it) this morning after the planned OPEC+ meeting

was delayed and tentatively scheduled for Thursday. The bone of question must be

the US so far refusal to participate to a global effort to resorb the global oil

savings glut, initially triggered by a spat between Russia and Saudi Arabia to

cut supply but structurally caused by the US relentless grab of market share from

OPEC+ over the past 5 years. If the US is part of the of the problem, it must

be part of the solution…and that is (most likely) why the “done” deal presented

on Friday to have OPEC+ reducing supply by 10mn bd will have to wait until till

Thursday. Specialists also argued over the week end that to avoid “real” prices

to return to where they were in practice (around USD10/barrel), supply should

be curtailed by 15 or even 20mn/d barrel.

Still, US futures rallied 3% overnight, holding a defiant stance. This move

may create an impression to start the week but does not seem totally substantiated.

There was some good news on the corona front with less cases of death reported in

Italy and New York (for the first time) but the news flow was mixed at best.

More cases were found in Singapore (biggest daily increase in new cases) and Japan

after a spike hinted at the possibility of a national state of emergency being declared

as early as tomorrow to impose broader lock downs. UK Prime Minister was admitted

to hospital yesterday which created a small dip in GBP. There are about 48k averred cases in the UK

with more than 4k deaths and an unusually high mortality rate.

Trend Score Card

Click here for technical

annotations.

{kind=link}

{kind=link}

US

& International Equities

Check out US and International Stocks’ Technical

Trend Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and when

they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their

trend, expected Fed rate moves and speculative positioning in 10-year Treasury

Futures.

{kind=link}

US

Recession Risk Radar

A comprehensive list of

economic indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs. G7

and EM counterparts.

{kind=link}

Precious Metals

Check out where precious

metals stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and futures

traders’ sentiment (non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the

Stock market correlate with each other and speculative futures positioning

on Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and rule-based

trend following investment approach can serve as an effective portfolio

insurance technique.

To receive a Daily Trend

Status Update and round the clock market and economic instant notifications, join the

free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio Management and Advisory Services

BentinPartner GmbH is a

Swiss registered independent financial adviser. We offer four different

portfolio management mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an

optimized strategic benchmark. This allocation delivers the “beta” (or markets

related) performance of your portfolio while we seek to generate additional

“alpha” (“skills related) performance with tactical adjustments, using a

predefined maximum “value at risk” envelope. Most of the portfolio’s

performance is derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or benchmark)

and pursues a “total” as opposed to “relative” return objective. With this

mandate, we seek to beat the best of “cash” or of the MSCI World Equity index,

applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage

(not exceeding 100% of NAV). You control the portfolio allocation (which can be

a pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the recipient's

sole use. Please do not forward it without prior authorization. It is not

intended as a recommendation, an offer or solicitation for the purchase or sale

of any security or underlying asset referenced herein or investment advice.

Investors should seek financial advice regarding the suitability of any investment

strategy based on their objectives, financial situation, investment horizon and

particular needs. This report does not include information tailored to any

particular investor. It has been prepared without any regard to the specific

investment objectives, financial situation or particular needs of any person

who receives this report. Accordingly, the opinions discussed in this

Report may not be suitable for all investors. You should not consider any of

the content in this report as legal, tax or financial advice. The data and analysis

contained herein are provided "as is" and without warranty of any

kind. BentinPartner llc, its

employees, or any third party shall not have any liability for any loss

sustained by anyone who has relied on the information contained in any

publication published by BentinPartner llc. The content and views expressed in this report

represents the opinions of Marc Bentin and should not be construed as

guarantee of performance with respect to any referenced sector. We remind you

that past performance is not necessarily indicative of future results. Although

BentinPartner llc believes

the information and content included in this report have been obtained from

sources considered reliable, no representation or warranty, express or

implied, is provided in relation to the accuracy, completeness or reliability

of such information. This Report is also not intended to be a complete

statement or summary of the industries, markets or developments referred to in

the Report.

#fx #forex #investing

#markets #riskmanagement #bankingindustry

#finances #money #traders #quants