Sunday, January 12, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice start of the week.

Marc

Bentin

Bentinpartner GmbH

{kind=link}

{kind=link}

{kind=link}

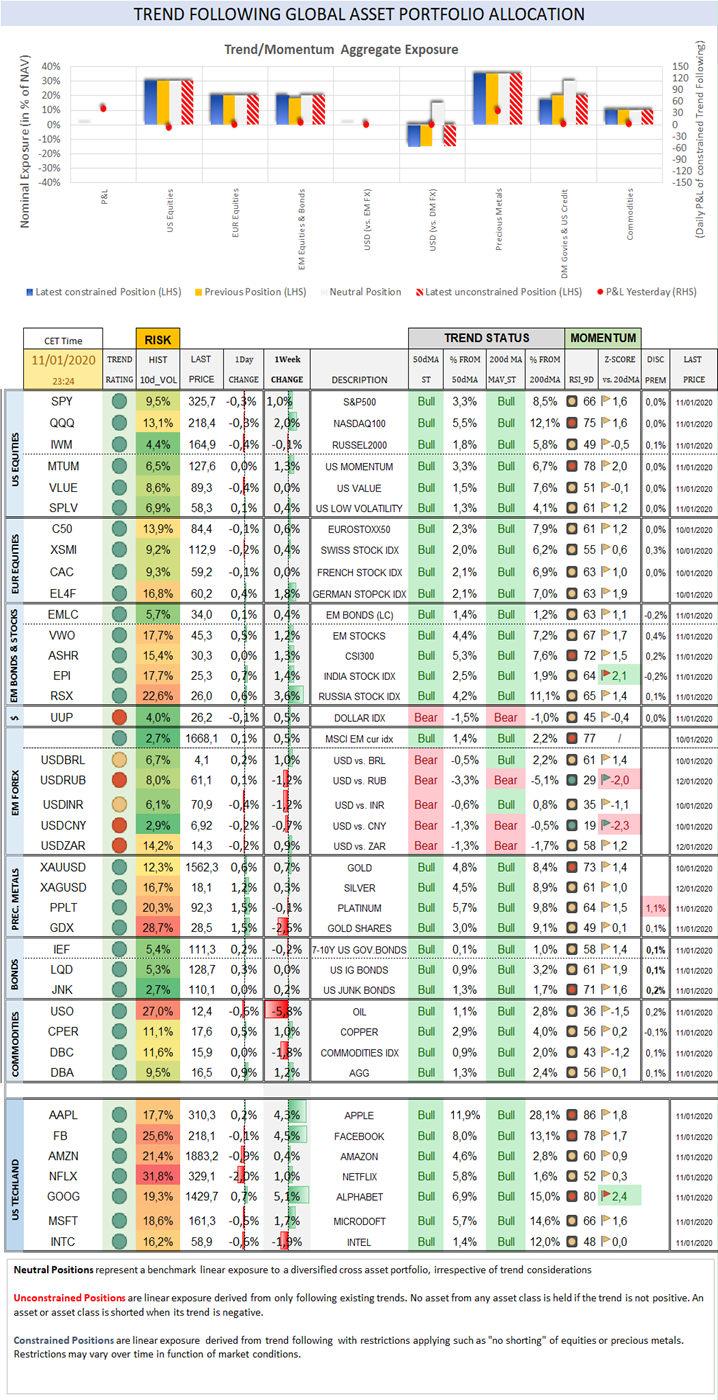

Trend

Status Update

Over the past

week, the S&P500 gained 1,0% (1,2% YTD) while the Nasdaq100 gained 2,0%

(2,7% YTD). The US small cap index dropped -0,1% (-0,5% YTD). Soft payrolls data offered a reason for a mild correction

ahead of the week end after US benchmarks hit fresh records earlier last week.

The Eurostoxx50 gained 0,6% (1,5%), underperforming the S&P500

by-0,4%. Investors flocked into Fangs again with most of them rallying strongly on the

week.

{kind=link}

AAPL rallied 4,3% (5,7%). FB added

4,5% (6,2%). LYFT rallied 6,6% (7,1%). AMZN gained 0,4% (1,9%). NFLX gained

1,0% (1,7%). GOOG rallied

5,1% (6,9%, Z-score 2,4). The CEO of GOOG just received a strong

incentive in getting his stock price higher with the SEC approved that his

performance bonus would be tied this year and next not on the share price itself

but on its outperformance vs. the S&&P500. The concentration of performance

of US indices on just a few names is at its highest since the late 1990’s with

the top 5 companies of the S&P500 (1%) making up 18% of the total market

cap of the index. The percentage of US listed companies losing money over the

past 12 months is now also close to 40%, its highest level since the

concentration peak of 1999 and a situation that could only get worse in a

recessionary scenario. At the same time,

the issuance of high yield issuance is red hot and even stronger than last

year. The profit season is kicking off this week and should show some

improvement vs. last quarter but it is not a stretch of the imagination to

consider that today’s situation is …stretched and reminiscent of historic

extremes. In the meantime, and probably for that reason, although major US

indices returned more than 30% last year, Ray Dalio reported

his first annual loss since 2000 with its Pure Alpha fund returning -0.5% in

2019. Crispin Odey, another famed Hedge Fund manager

finished down 10% last year.

Last week, more emails were made public from Boeing personnel who qualified

the 737 Max as a plane “designed by clowns and certified by Monkies”,

which in a colourful fashion further compromised the future of this airplane.

The company announced last week that it would stop the production of the plane generating

the largest part of its income as of next month and start firing employees.

Diversified EM equities (VWO) gained 1,2% (1,8%), supported by continued

strong inflows in China, CNY breaking higher and the CSI300 trading in positive

trend mode and near the top of its Bollinger band (see China’s snapshot). Noticeably at a time when many investors fret

over excess leverage in China, China’s CDS is now only 30bps, a fresh low and

half the level where it was at the same time last year. XHB (SPDR S&P HOMEBUILDERS ETF) gained 1,6% (1,4%, Z-score 2,0).,

supported by a further decline in US mortgage rates.

{kind=link}

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies gained 0,5% (1,0%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) gained 0,5% (0,2%). We continue to

expect more currency instability this year and were hard pressed, like many observers,

to see the way the dollar (and to a lesser extent the yen) reacted to the spike

in risk off last week (that briefly propelled gold above USD1600) in the aftermath

of the US/Iranian spat. This, coupled to ongoing strength in EM currencies and a

possible further easing by the Fed, coupled to fiscal slippage and a diminishing

appetite of foreigners for US Treasuries, could take its toll on the USD throughout

the year.

10Y US Treasuries dropped 3bps (-10bps) to 1,82%. 10Y Bunds climbed 8bps

(-1bps) to -0,20%. 10Y Italian BTPs dropped -3bps (-9bps) to 1,32%, out-performing

Bunds by -4bps. US High Yield (HY) Average Spread over Treasuries dropped -8bps

(-9bps) to 3,27%. US Investment Grade Average OAS was unchanged (4bps) to

1,05%. Former Fed Chair B. Bernanke pushed back last week the notion that

central banks have lost their influence on the economy and may be out of ammunition.

Former Treasury Secretary L. Summers dismissed Bernanke’s optimism and referred

to the current situation as being the “last hurrah for central bankers” as he

argued that monetary policy will not be able “to do it the next time”, given

that in past recessions, the Fed usually cut by 5% whilst interest rates are

currently below 2%. “We’ll have to rely on putting money in people’s pockets”,

he said as he also discarded the possibility of putting in place semi-automatic

stabilisers that would bypass Congress. Economic data published last week were

mostly subdued in the US, Germany and Japan. Prior to the weaker US jobs

report, Japan services sector saw its deepest contraction in more than three

years in December (Services PMI dropped to 49.3 from 50.3 in November). German

industrial orders fell unexpectedly on weak foreign demand, confirming the

manufacturing slump. The World Bank also trimmed its global growth forecast for

2019 and 2020 due to a slower than expected recovery in trade and investment

despite a cooling in trade tensions. At the same time, in Europe inflation

across the eurozone rose to a six-month high of 1.3% (from the previous month

at 1%) even before the recent jump in oil prices, still below the ECB target

goal of just below 2%.

In European credit markets, EUR 5Y Senior Financial Spread dropped -3bps

(-1bps, Z-score -2,1) to 0,50%.

Gold gained 0,7% (3,0%) while Silver gained 0,3% (1,5%). Major Gold

Mines (GDX) sold off by -2,5% (-2,8%). The correlation analysis between Gold

and stocks continue to show the attractive diversification (hedging) potential of gold vs. risky assets despite cross asset correlation

recently increasing above their 5year, 1year and 1 month averages.

{kind=link}

Goldman Sachs Commodity Index sold off by -3,2% (-1,4%). Gold rallied

past USD1600 on geopolitical tensions before ebbing back following the

accidental shooting down of a passenger jet during the Iranian shelling operation

of the US military base in Iraq. WTI

Crude sold off by -6,4% (-3,3%). NGA (NATURAL GAS FUTR Feb20) rallied 3,4% (0,6%).

Over the week end….

Iran confirmed over the week end the accidental shooting down of a Ukrainian

civil aircraft that took 140 lives, neutralizing by the same count, and at

least for a while, the potential for more Iranian (and US!) military escalation.

This week will witness a (theatrical?) signature of the phase I China/Us trade

deal…and if that does not hold the market up, there will likely be Presidential

tweets about a Phase 2 deal progress. This is also helping Chinese markets.

D. Trump took it to Tweeter in Arabic overnight, saying that “sanctions

and protests have put Iran under great pressure and force them to negotiate.” Perhaps,

his language skills will appeal to

Iranians.

Trend Score Card

Click here for technical annotations.

{kind=link}

{kind=link}

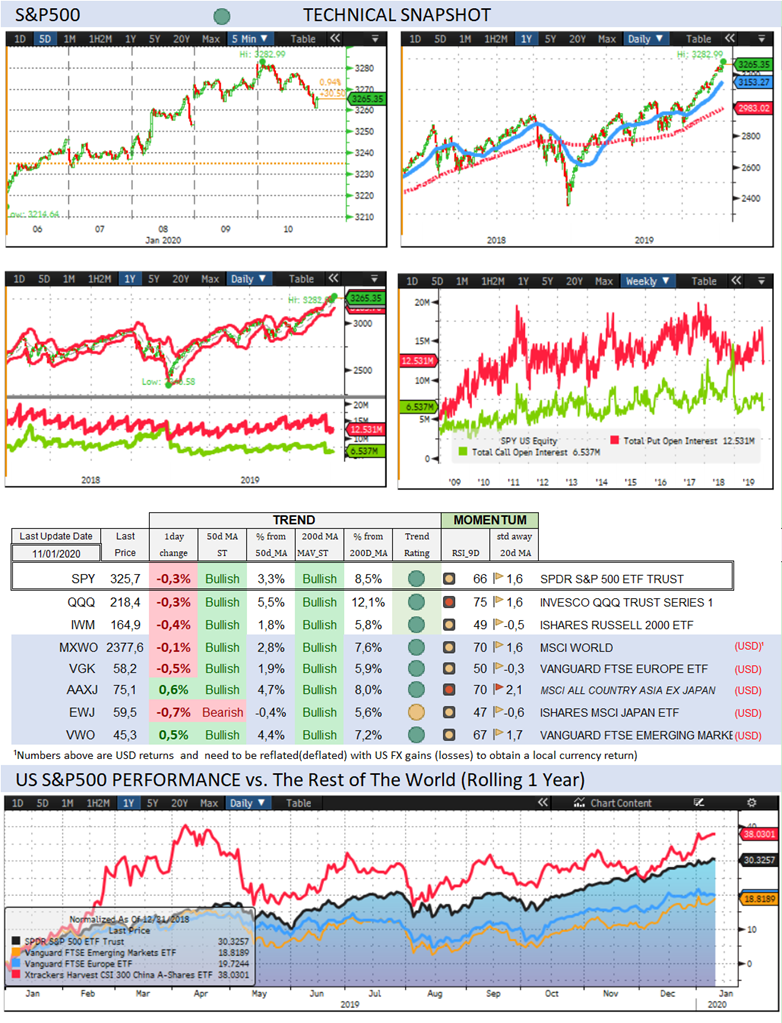

US

& International Equities

Check out US and International Stocks’ Technical

Trend Status.

{kind=link}

Sector

Trend & Momentum (revised)

Check out equity sectors’ trend and performance

…and when they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their

trend, expected Fed rate moves and speculative positioning in 10-year Treasury

Futures.

{kind=link}

US Recession

Risk Radar

A comprehensive list of

economic indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs.

G7 and EM counterparts.

{kind=link}

Precious Metals

Check out where precious

metals stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and

futures traders’ sentiment (non-commercials open positions).

{kind=link}

Why Trend Following Matters and How It Can Help

You?

The last months of 2018

illustrated how fast and furious markets can fall. Trend following offers

guidance as to when to join and when to leave an asset class with changing

trend characteristics. A disciplined and rule-based trend following investment

approach can serve as an effective portfolio insurance technique. Our purpose,

beyond tracking economic, political and monetary developments is to assist

readers investing in global markets with a keen focus on trend formation

covering all important asset classes.

To receive a Daily Trend

Status Update and much more, join a

free trial of our premium research.

To learn more about our premium research:

https://www.bentinpartners.ch/research

Feel free to join our free trial and choose your

delivery preferences:

https://www.bentinpartners.ch/subscribe

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the

recipient's sole use. Please do not forward it without prior authorization. It

is not intended as a recommendation, an offer or solicitation for the purchase

or sale of any security or underlying asset referenced herein or investment

advice. Investors should seek financial advice regarding the suitability of any

investment strategy based on their objectives, financial situation, investment

horizon and particular needs. This report does not include information tailored

to any particular investor. It has been prepared without any regard to the

specific investment objectives, financial situation or particular needs of any

person who receives this report. Accordingly, the opinions discussed in

this Report may not be suitable for all investors. You should not consider any

of the content in this report as legal, tax or financial advice. The data and

analysis contained herein are provided "as is" and without warranty

of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss

sustained by anyone who has relied on the information contained in any

publication published by BentinPartner llc. The content and views expressed in this report

represents the opinions of Marc Bentin and should not be construed as

guarantee of performance with respect to any referenced sector. We remind you

that past performance is not necessarily indicative of future

results. Although BentinPartner llc believes the information and content included in

this report have been obtained from sources considered reliable,

no representation or warranty, express or implied, is provided in relation to

the accuracy, completeness or reliability of such information. This Report is

also not intended to be a complete statement or summary of the industries,

markets or developments referred to in the Report.

#fx #forex

#investing #markets #riskmanagement #bankingindustry #finances #money #traders #quants