Monday, March 02, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice week.

Marc

Bentin

Bentinpartner GmbH

{kind=link}

{kind=link}

Trend

Status Update

The economic impact will be considerable although hard to gauge but a

growing number of analysts now consider the growing likelihood that the world

economy will fall into recession this year, bowing under the nourished fire of a

heavy supply (disrupted supply chains) and demand (stalling tourism and

discretionary spending) shock. Equity and credit markets were sent into

disarray, still leaving investors with the hope that central banks will come to

the rescue to deliver more of the same posology of lower rates and more asset

monetisation. It is difficult to imagine how effective these measures will be to

resuscitate investment bubbles that were punctuated by a melt up phase that was

itself caused by excessive easing delivered at a time when it was not necessary.

More of the same is still forthcoming with up to three rate cuts now expected

by the Federal Reserve for the rest of the year. A first move will likely

happen inter-meeting or at the next Fed March 18th FOMC gathering

(Goldman now expects a 50bps cut this month). ECB President Christine Lagarde

cautioned on Thursday that additional measures were not necessary just yet,

implicitly admitting that there is not much else she can do beyond calling for coordinated

fiscal easing. There were some early signs on Wednesday that Germany was getting

ready to open the purse strings. D. Trump called for a press conference on

Wednesday in an effort to prop up markets but his incantations fell flat as did

his doubts about the spreading of the virus on US soil coupled to his intimate

conviction that a vaccine will soon be found. Both expectations and hope ran against

the opinion of the CDC cautioning the former could likely still happen and the

latter not before a year or a year and a half. Equity markets fell globally

into “correction” mode (the step before a bear market) will all major indices and

sectors dropping by 10+%. Credit spreads widened across the board, especially

the worse High Yield segment which saw its risk premium widen faster than US

Treasuries could rally. 10 Year Treasury yields dropped 32bps to an all-time

low of 1.15% while HY spreads widened 141bps, causing the global credit machine

(UD2.6trn international bond market) to grind to a halt. Surprisingly perhaps

and even as EM currencies suffered, the dollar index failed to capitalize on this

risk off week and it was funding currencies that rallied the most starting with

JPY, CHF but also EUR as traders were forced out to deleverage on carry trades.

Gold dropped sharply on Friday as traders hurried to sell winners and cover

losses elsewhere, purging some of the excess positions. Although more

volatility is warranted over the near term, it should not take too long for

precious metals to reassert themselves as the most natural safe haven when

policy rates and so called risk free bond yields all converge to 0 while central banks roll over additional rate cuts

and boost QE with governments likely to spend more including possibly with a

broader adoption of MMT (Modern Monetary Theory). If history is any guide, gold

has more leeway on the up than downside in our view. Speculators may have been

long and too long but typical investment portfolios have rarely 5% invested in

precious metals and this is likely change, in our view.

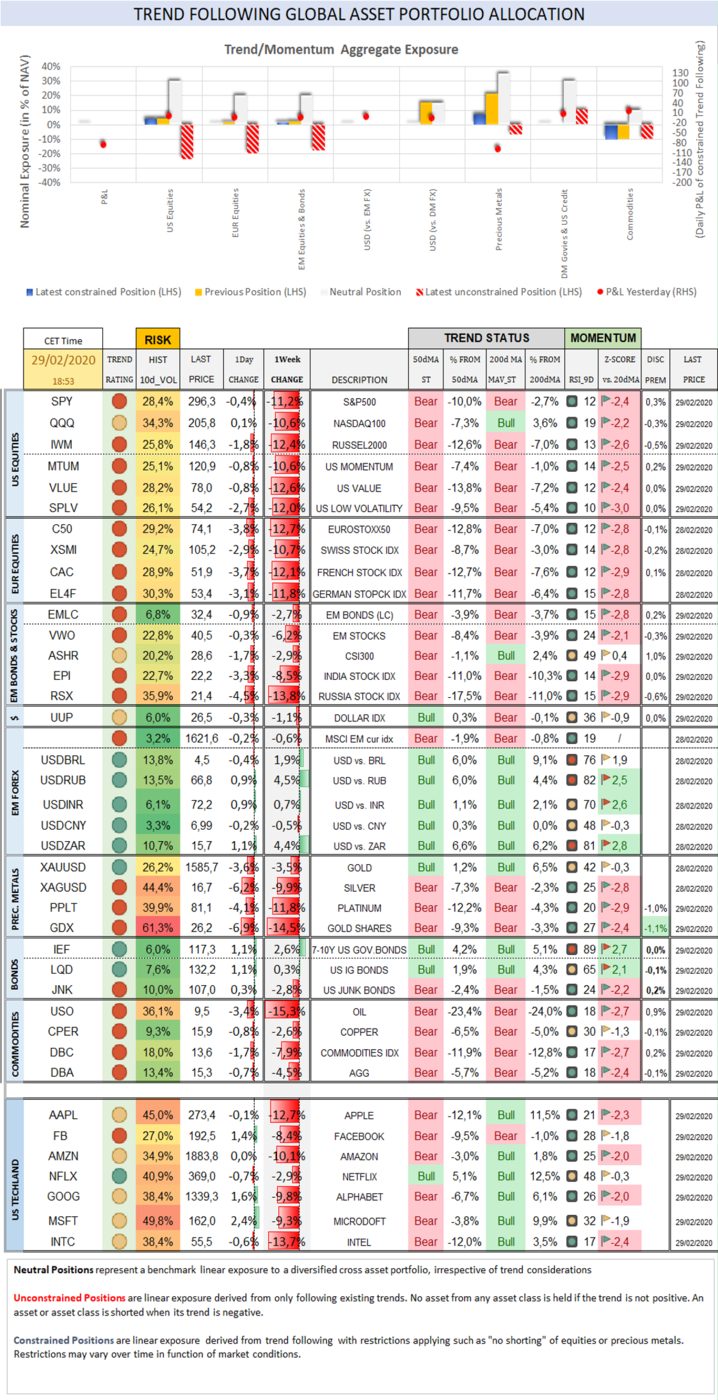

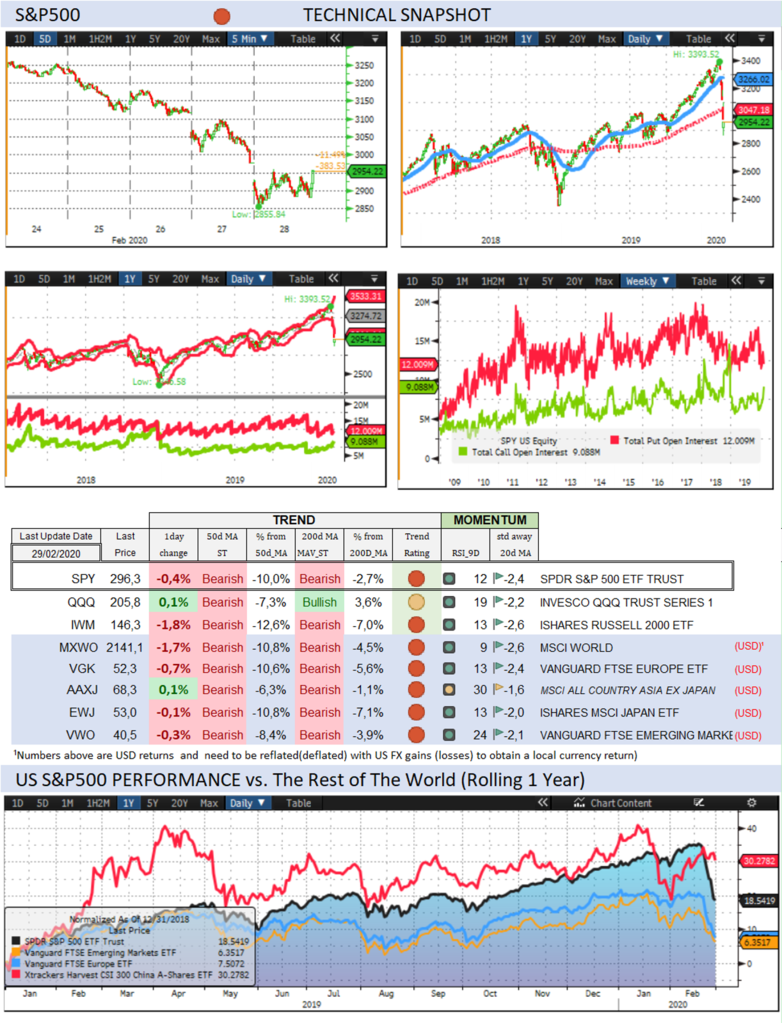

Last week, the S&P500

sold off by -11,2% (-8,0% YTD, Z-score -2,4) while the Nasdaq100 sold off by -10,6%

(-3,2% YTD, Z-score -2,2). The US small cap index sold off by -12,4% (-11,7% YTD,

Z-score -2,6).

CBOE Volatility Index

rallied 134,8% (191,1% YTD, Z-score 2,6) to 40,11.

The Eurostoxx50

sold off by -12,7% (-11,0%, Z-score -2,8), underperforming the

S&P500 by-1,6%.

Diversified EM

equities (VWO) sold off by -6,2% (-8,9%, Z-score -2,1), outperforming

the S&P500 by 4,9%. India’s growth expanded at 4.7% in Q4, the slowest pace

of growth in 6 years.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies dropped -1,1% (2,2%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) dropped -0,6% (-2,6%).

10Y US Treasuries rallied

-32bps (-77bps, Z-score -2,6) to 1,15%. 10Y Bunds dropped -18bps (-42bps,

Z-score -2,7) to -0,61%. 10Y Italian BTPs underperformed rising 19bps

(-31bps, Z-score 2,8) to 1,10%.

US High Yield (HY) Average

Spread over Treasuries climbed 141bps (164bps, Z-score 2,9) to 5,00%. US

Investment Grade Average OAS climbed 26bps (35bps, Z-score 3,0) to 1,36%.

In European credit markets, EUR 5Y Senior Financial Spread climbed 26bps (23bps, Z-score 3,1) to

0,74%.

Gold sold off by -3,5% (4,5%) while Silver sold off by -9,9% (-6,7%,

Z-score -2,8). Major

Gold Mines (GDX) sold off by -14,5% (-10,5%, Z-score -2,4).

Gold revised its Gold forecast higher to USD1800, citing global risk

aversion.

Goldman Sachs Commodity

Index sold off by -10,5% (-18,5%, Z-score -2,7). WTI Crude sold off by -16,1%

(-26,7%, Z-score -2,8)

Over the week end…

Federal Reserve Chairman Jerome Powell said on Friday that the

US central bank is prepared to cut interest rates while former Fed Chair Yellen

took issue with MMT saying at an Asian investors’ conference hosted by Credit

Suisse in Hong Kong. “That’s a very wrong-minded theory because that’s how you

get hyper-inflation.” She also said that yield-curve inversion happens very

easily and doesn’t alone signal a US recession is imminent, though it can

signal that Fed might at some point need to cut interest rates.

Infections in Italy jumped 50% in a day, a dozen new cases were

reported in the U.K. and the first infections broke out in the German financial

capital.

Acting White House Chief of Staff Mick Mulvaney said school

closings in the U.S. are likely.

China’s February manufacturing activity gauge plunged to its lowest

level on record over the week end.

Australia is all-but certain to cut rates Tuesday, according to

Bloomberg.

J. Biden won a South Carolina primary over the week end, boosting his

campaign ahead of a likely decisive “super Tuesday”. At the same time P.

Buttigieg chose to drop out of the race.

Trend Score Card

Most Asset

classes saw their trend signalling reverse last week, leading most sectors to

return to neutral gear.

Click here for technical annotations.

{kind=link}

US

& International Equities

Check out US and International Stocks’ Technical Trend

Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and

when they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their trend,

expected Fed rate moves and speculative positioning in 10-year Treasury Futures.

{kind=link}

US

Recession Risk Radar

A comprehensive list of economic

indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs.

G7 and EM counterparts.

{kind=link}

Precious Metals

Check out where precious metals

stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and

futures traders’ sentiment (non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the Stock

market correlate with each other and speculative futures positioning on

Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and

rule-based trend following investment approach can serve as an effective

portfolio insurance technique.

To receive a Daily Trend Status

Update and round the clock market and economic instant notifications, join

the free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery

preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio Management and Advisory Services

BentinPartner GmbH is a Swiss

registered independent financial adviser. We offer four different portfolio

management mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an

optimized strategic benchmark. This allocation delivers the “beta” (or markets

related) performance of your portfolio while we seek to generate additional

“alpha” (“skills related) performance with tactical adjustments, using a

predefined maximum “value at risk” envelope. Most of the portfolio’s

performance is derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or

benchmark) and pursues a “total” as opposed to “relative” return objective.

With this mandate, we seek to beat the best of “cash” or of the MSCI World

Equity index, applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage

(not exceeding 100% of NAV). You control the portfolio allocation (which can be

a pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at +41615444310.

We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the list,

please send us an email by clicking here, mentioning “unsubscribe” in

the title.

To ensure that our emails reach

your inbox and not your spam folder, please consider adding Marc.Bentin@BentinPartner.ch,

Marc.Bentin@BentinPartners.ch and our alternate address Bentinpartner@gmail.com

to your safe address book. If you are using Microsoft Outlook, simply right

click on our email address, choose "add to Outlook contacts" and then

"save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the

recipient's sole use. Please do not forward it without prior authorization. It

is not intended as a recommendation, an offer or solicitation for the purchase

or sale of any security or underlying asset referenced herein or investment

advice. Investors should seek financial advice regarding the suitability of any

investment strategy based on their objectives, financial situation, investment

horizon and particular needs. This report does not include information tailored

to any particular investor. It has been prepared without any regard to the

specific investment objectives, financial situation or particular needs of any

person who receives this report. Accordingly, the opinions discussed in

this Report may not be suitable for all investors. You should not consider any

of the content in this report as legal, tax or financial advice. The data and

analysis contained herein are provided "as is" and without warranty

of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss sustained

by anyone who has relied on the information contained in any publication

published by BentinPartner llc.

The content and views expressed in this report represents the opinions

of Marc Bentin and should not be construed as guarantee of

performance with respect to any referenced sector. We remind you that past

performance is not necessarily indicative of future results. Although BentinPartner llc believes the

information and content included in this report have been

obtained from sources considered reliable, no representation or

warranty, express or implied, is provided in relation to the accuracy,

completeness or reliability of such information. This Report is also not

intended to be a complete statement or summary of the industries, markets or

developments referred to in the Report.

#fx #forex

#investing #markets #riskmanagement #bankingindustry #finances #money #traders #quants