Sunday, April 12, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

I

wish you all a happy week end and peaceful Eastern.

Marc

Bentin

Bentinpartner GmbH

{kind=link}

{kind=link}

Trend

Status Update

Over the past week, risk appetite responded to the avalanche of

liquidity, backstop and fiscal stimulus measures announced in the US, China,

Europe, Japan or pretty much everywhere else. On Thursday, in an historic

moment, the Fed went full circle, announcing that it would also start buying

junk bonds or rather ETF’s invested in them as part of the backstop measures

aimed at fighting the corona recession /depression.

The next step would be for the Fed to step in and

buy cash equities directly (a la Japan). For now, this may not be necessary

given that equity markets act as a derivative of credit markets and that the

option of propping up the S&P and Nasdaq futures markets remains in the

arsenal (cfr. Christmas 2018). Yesterday’s measure,

for as necessary as it might have been, looked to us like crossing the Rubicon

of monetary policy orthodoxy and sealing the fate of free markets all together.

This may be a temporary feature, just like the confinement that half the world

lives in, but we doubt it and sit in the camp of those looking for the Fed

balance sheet to hit 10-12trn at some point in a not too distant future

(currently USD6trn).

Just ten years ago, the Fed’s balance sheet stood around USD800bn. Ten

years later, at the beginning of the year, it was USD4.5trn. Over the past 5

weeks alone, it increased by another USD1.5trn and expectations are now for the

Fed’s balance sheet to reach USD10trn-USD12trn in a not too distant future.

The rubber will likely meet the road when the actual components of the

HYG and JNK ETF’s that squeezed on Thursday in response to the Fed’s latest

policy move (similarly to LQD, a couple

of weeks’ back) will start defaulting in line with what should be expected in

consequence of an economic recession, sharp degradation of earnings and still

unsustainably low oil prices (many HY bonds are shale oil producers that are

dead in the water at current oil prices). By the time this happens, if the Fed

keeps buying these specific ETF’s, without buying the underlying debt (which it

might ultimately have to do as well, hence our call on the Fed’s balance

sheet), these funds will start trading at a big premium to Nav. As of the close

on Thursday HYG and JNK traded already at a premium of 4.7%.

What happens next, we will find out, but I invite readers to read the

note below from Degussa written by somebody knowledgeable about what happened

in the 30’s in Germany. The hope is indeed that history does not repeat itself

and only rhythmes.

http://news.degussa-goldhandel.de/marketreport/newsletter/86SH26KSO9.pdf

(Excerpts are reproduced below)

“...when market forces have the space to restore

the economy to equilibrium. However, neither politicians, bankers,

entrepreneurs, nor employees want this to happen. This gives a Carte Blanche to

governments and their central banks – supported by a public who is becoming

increasingly fearful of job losses and personal ruin – to go ahead and do away

with what little is left of the free market system.

To escape the bust, the free market system is

transformed into a Befehlswirtschaft: A system in

which the means of production remain formally in private hands, but in which

the state, and the special interest groups running state, are really in the

driver’s seat by dictating and controlling goods prices, interest rates and

wages, labour conditions and incomes, and even nationalising and managing banks

and entire industries etc. This was the model the German National Socialist

erected in the late 1930s: The state dictated what was to be produced by whom,

when and where, and at what costs.

History does not repeat itself, but sometimes, it

rhymes. The Western world is increasingly, and quite rapidly so, bidding

farewell to the idea of the free market system – driven by the attempt of

fending off the inevitable bust as a consequence of a decade long debt binge

caused and made possible by central banks’ fiat money regime. While this may

indeed keep away the bust for quite some time, it will weaken output and

employment gains. Peoples’ standard of living does no longer improve at an

acceptable clip, or it may even decline; and with it comes impoverishment and

perhaps even social unrest.

These are the very ingredients that facilitate the

rise of the totalitarian state. So the unpalatable

truth is that without allowing for a bust, a big crash, the fiat money system

and with it all the forces working towards the aggrandisement of the state are

here to stay and will predictably get worse. The hefty price of upholding the

current boom and the economic and social structure it has brought about is the

end of the free market society as we knew it.”

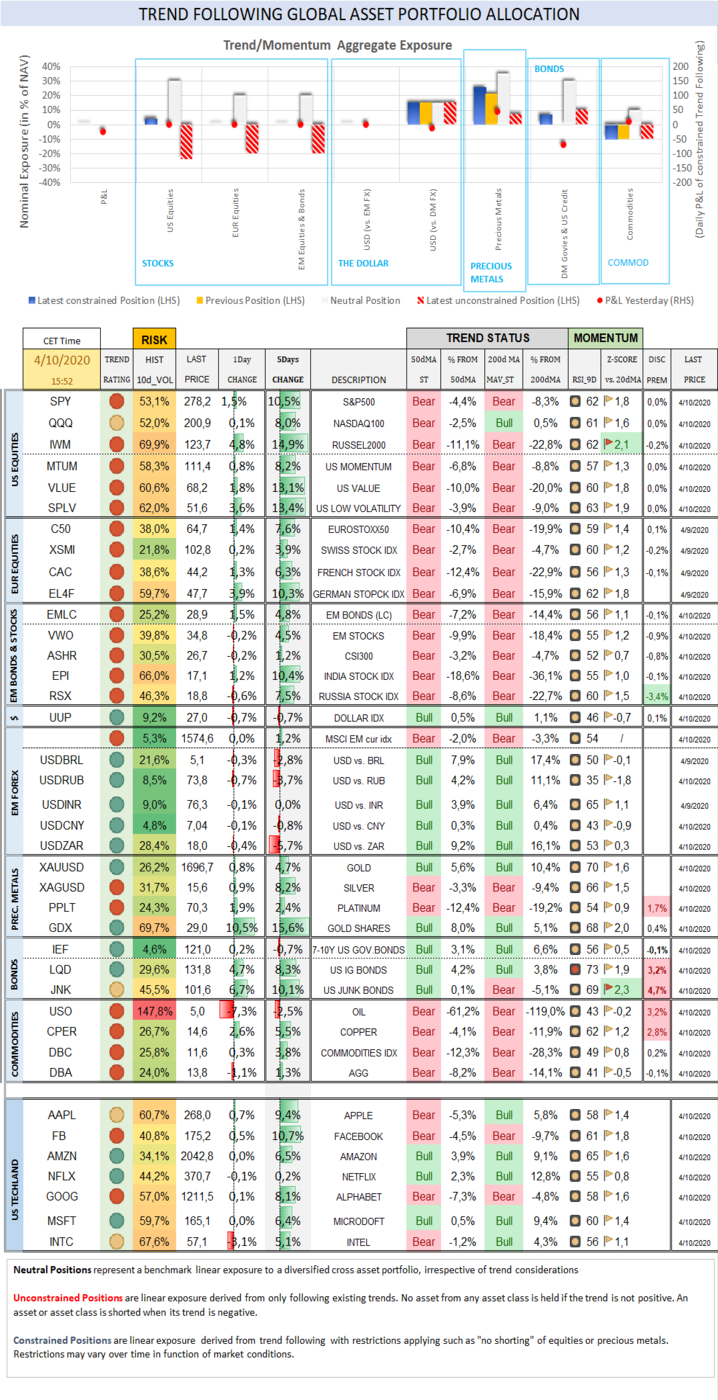

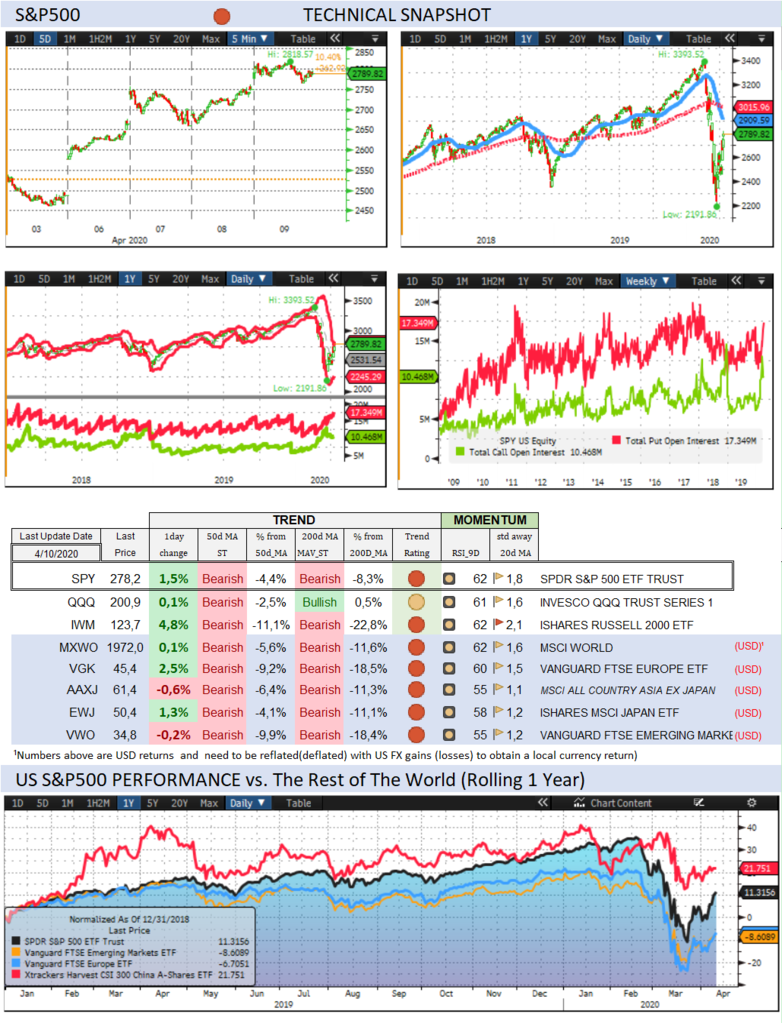

CBOE Volatility Index sold off by -18,1% (202,4% YTD) to 41,67.

The Eurostoxx50 rallied 7,6% (-22,2%), underperforming the S&P500

by-2,9%.

Diversified EM equities (VWO) rallied 4,5% (-21,7%), underperforming the

S&P500 by-5,9%. CSI300 Chinese equity index (ASHR) gained 1,2%

(-9,9%), still leading for the year. Indian shares (EPI) rallied 10,4%

(-31,2%). Russian shares (RSX) rallied 7,5% (-24,8%).

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies dropped -0,7% (3,8%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) gained 1,2% (-5,4%).

The Euro strengthened as the dollar weakened. EURUSD gained 1,3%

(-2,5%). EURCHF gained 0,1% (-2,6%). EURJPY gained 1,2% (-2,6%). EURGBP dropped

-0,2% (3,8%).

Acting as a reliable “risk on/risk off” indicator, AUDUSD rallied 5,9%

(-9,6%) while AUDNZD rallied 2,1% (0,2%).

EM currencies staged a powerful turnaround, independently from oil still

trading on shaky ground but in full expectations of an historic oil production

cut deal between OPEC++ (including the US and other G20 oil producing

countries). USDBRL sold off by -2,8%

(26,9%). USDRUB sold off by -3,7% (19,1%). USDMXN sold off by -6,8% (23,2%). USDINR

was unchanged (6,9%). USDCNY dropped -0,8% (1,0%). USDZAR sold off by -5,7%

(28,3%).

10Y US Treasuries underperformed with yields rising 12bps (-120bps) to

0,72%. 10Y Bunds climbed 9bps (-16bps) to -0,35%. 10Y Italian BTPs climbed 4bps

(18bps) to 1,59%, outperforming Bunds by 4bps.

US High Yield (HY) Average Spread over Treasuries dropped -134bps

(449bps) to 7,85%. US Investment Grade Average OAS dropped -49bps (120bps) to

2,21%, boosted by the Fed’s decision on Thursday to add the purchase of High Yield

bonds (or at least ETF’s trading them) to its backstopping list.

In European credit markets, EUR 5Y Senior Financial Spread dropped

-36bps (43bps) to 0,95%.

Precious metals continued to power ahead, making new highs vs. GBP, EUR

and JPY, ending the week with Gold vs. CHF just 1.5% away from its own all time

high. Gold rallied 4,7% (11,8%) while Silver rallied 8,2% (-12,8%) with silver

outperforming (for a notable change). Major Gold Mines (GDX) stormed higher

gaining 15,6% (-1,1%).

Goldman Sachs Commodity Index rallied 3,0% (-38,6%). WTI Crude sold off

by -10,1% (-62,7%), awaiting the details …of an historic deal this week end or

later next week.

Over the week end…

Negotiators are still racing to clinch a historic

deal to cut oil supply. The Kremlin warned of “unmanageable chaos” if

negotiations fail. Mexico was asked to make an effort. Trump intermediated and

offered a compromise that was rejected by Saudi Arabia. Talks between Saudi

Arabia and Mexico continued through the weekend. A 10% reduction in worldwide

crude output remains likely and unprecedented but would barely dent the surplus

that continues to build as the virus lockdown spreads, Bloomberg reported. WTI slid more than 9% on Thursday -- as

a deal looked likely -- settling below $23 a barrel. Markets were closed on

Friday.

Trump Doubled Down On Threat To "Hold" $500 Million From WHO

US equity markets will trade on Monday. Europe will

reopen on Tuesday.

Trend Score Card

Click here for

technical annotations.

{kind=link}

US

& International Equities

Check out US and International Stocks’ Technical Trend

Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and

when they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their trend,

expected Fed rate moves and speculative positioning in 10-year Treasury Futures.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs.

G7 and EM counterparts.

{kind=link}

Precious Metals

Check out where precious metals

stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and

futures traders’ sentiment (non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the Stock

market correlate with each other and speculative futures positioning on

Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and

rule-based trend following investment approach can serve as an effective

portfolio insurance technique.

To receive a Daily Trend Status

Update and round the clock market and economic instant notifications, join the

free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery

preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio Management and Advisory Services

BentinPartner GmbH is a

Swiss registered independent financial adviser. We offer four different

portfolio management mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an

optimized strategic benchmark. This allocation delivers the “beta” (or markets

related) performance of your portfolio while we seek to generate additional

“alpha” (“skills related) performance with tactical adjustments, using a

predefined maximum “value at risk” envelope. Most of the portfolio’s

performance is derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or

benchmark) and pursues a “total” as opposed to “relative” return objective.

With this mandate, we seek to beat the best of “cash” or of the MSCI World

Equity index, applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage (not

exceeding 100% of NAV). You control the portfolio allocation (which can be a

pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at +41615444310.

We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the list,

please send us an email by clicking here, mentioning “unsubscribe” in

the title.

To ensure that our emails reach

your inbox and not your spam folder, please consider adding Marc.Bentin@BentinPartner.ch,

Marc.Bentin@BentinPartners.ch and our alternate address Bentinpartner@gmail.com

to your safe address book. If you are using Microsoft Outlook, simply right

click on our email address, choose "add to Outlook contacts" and then

"save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the

recipient's sole use. Please do not forward it without prior authorization. It

is not intended as a recommendation, an offer or solicitation for the purchase

or sale of any security or underlying asset referenced herein or investment

advice. Investors should seek financial advice regarding the suitability of any

investment strategy based on their objectives, financial situation, investment

horizon and particular needs. This report does not include information tailored

to any particular investor. It has been prepared without any regard to the

specific investment objectives, financial situation or particular needs of any

person who receives this report. Accordingly, the opinions discussed in

this Report may not be suitable for all investors. You should not consider any

of the content in this report as legal, tax or financial advice. The data and

analysis contained herein are provided "as is" and without warranty

of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss sustained

by anyone who has relied on the information contained in any publication

published by BentinPartner llc.

The content and views expressed in this report represents the opinions

of Marc Bentin and should not be construed as guarantee of

performance with respect to any referenced sector. We remind you that past

performance is not necessarily indicative of future results. Although BentinPartner llc believes the

information and content included in this report have been

obtained from sources considered reliable, no representation or

warranty, express or implied, is provided in relation to the accuracy,

completeness or reliability of such information. This Report is also not

intended to be a complete statement or summary of the industries, markets or

developments referred to in the Report.

#fx #forex

#investing #markets #riskmanagement #bankingindustry #finances #money #traders #quants