Sunday, April 19, 2020

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a pleasant week end.

Marc

Bentin

Bentinpartner GmbH

{kind=link}

{kind=link}

Trend

Status Update

After dropping rather precipitously on Wednesday as D. Trump vowed to

act in violation of the US constitution to force US Governors to end

confinement and as oil prices failed to stabilize, equity markets rallied on

Thursday night and then again on Friday on a mostly constructed bullish

narrative. First was a press conference promising that many states would soon

be “freed” (meaning taken out of confinement). Second was a rumour (later

downplayed by the company itself) that a Gilead trial for its drug Remdesivir would turn out to be an effective treatment in

fighting Covid-19. Last but not least on Friday came news that Boeing would

soon restart production. This was welcome news for 27k workers going back to

work but the unanswered question remains where those planes will be stored

because few people need more planes as few

people will buy them with very few people flying and those who do probably rather

flying on something else than a 737max… Boeing which is already on life saving

support from the US government most likely did what it was told to do which is

to restart building planes. Boeing shares rallied 14%. In the afternoon on

Friday, the market zig-zagged with aapl a bit weaker

on a downgrade from Goldman Sachs until a ramp job in the last hour boosted the

indices back to the morning highs, leaving investors in a good spirit for the

week end.

Nobody knows where we are and where we go. Those who expected stocks to

further drop last week (Goldman) with S&P forecast at 2000 are now revising

their outlook, expecting the S&P to squeeze towards 3000 before an even

harder fall. In other words, everybody has moved to ‘trend following’ or CTA

driven (those ignoring mass layoffs tracking instead if others are

buying(selling) at which point they too join the buying (selling))…because there is nothing else to do.

As my readers know, I have some sympathy with trend following or

automatic investing (the whole idea behind Trend Model Updates).

Not the whole but the skill part (still accessible to humans) of Trend

Following is to front run some of these trend signal changes across asset

classes before they are triggered so as to beat the robots. This skill can be

applied and has some usefulness when markets trade “continuously” but stops

operating when the speed of adjustment and volume occur too rapidly in no time

nor volume. At this point the market moves “discreetly” as opposed to “continuously”

and ....it is broken. When it does so on a constructive and mostly false

narrative (“We have got a vaccine”, “we end lockdown because the danger is over

or manageable without it”, “Boeing restart producing planes, let’s buy hotels

and tourism names”), it is twice broken, and when it does so on moves of high

amplitude and no volume, it is three times broken.

Unfortunately, that is where we are. We are also right in the middle of a clash

between mostly bullish technicals (CTA trend

followers) and mostly bearish fundamentals (Hedge funds for now), oscillating

between FOMO, horrible fundamentals, no visibility and mostly positive technicals (for now).

In the meantime, we should try to stay away from that bug. If/when we

catch it, we’ll give it the fight as well.

Over the past week, the S&P500 rallied 3,0% (-10,9% YTD) while the Nasdaq100

rallied 7,2% (1,3% YTD). The US small cap index dropped -1,3% (-26,3% YTD).

While stocks rallied on corona related optimism, the overall strength of

the market came mainly from “stay at home” stocks, mostly FANGS (a now 10-year-old

pattern) as investors kept flocking to the same handful stocks.

“With 9% of S&P 500 firms having already reported Q1 earnings

including all of the major banks, results have generally disappointed relative

to already tepid expectations. 43% of companies have missed consensus

expectations, on pace for the highest rate since at least 1998 with earnings

set to drop by 15% Y/Y, but it's Q2 where the real pain will be with Goldman

now expecting S&P 500 to plunge by a record 123% plunge”, ZH reported.

CBOE Volatility Index sold off by -8,4% (176,9% YTD) to 38,15.

The Eurostoxx50 gained 1,3% (-22,4%), underperforming the S&P500

by-1,8%.

Diversified EM equities (VWO) rallied 2,3% (-19,9%), outperforming the

S&P500 by -0,7%. CSI300 Chinese equity index (ASHR) gained 1,0% (-9,0%),

still the top performer in this year’s difficult markets. Indian shares (EPI)

gained 2,0% (-29,8%). Russian shares (RSX) sold off by -2,1% (-26,4%), dragged

down by ever lower oil prices but with losses that were mostly contained.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7

currencies gained 0,2% (4,0%) while the MSCI EM currency index (measuring the

performance of EM currencies vs. the USD) dropped -0,5% (-6,0%). EURUSD dropped

-0,6% (-3,0%). EURCHF dropped -0,5% (-3,1%). EURJPY dropped -1,4% (-4,0%). EURGBP

dropped -1,0% (2,8%).

The euro weakened slightly and across the board with debt mutualisation

still not flying (corona bonds) and a small spread widening in Italy wrongly portrayed

as a potential EU breaker, or clamoured to be as such, including by a EU core

country (France) that was never really able to vow or show restraint at the first place and now wants

debt mutualisation at all costs to ease off pressure on Italy while keeping an

eye at potential threats on its own signature. The ECB will keep buying these

national signatures as long and as much as needed as a short-term relief. Rules

of the stability pact should and will be eased to account for the situation

(debt/GDP ratio target of 60%; national deficit of 3% max) but collective debt

issuance is what profligate states have wanted all along and the Corona crisis

should not be seen as the excuse to throw (past and future) restraint under the

bus. On Friday, Bundesbank President J. Weidmann praised

euro-area governments for “significant, impressive” spending in the fight

against the coronavirus, but warned that they’ll need to tighten their budgets

once the emergency has passed, Bloomberg reported.

Dollar bulls should also not think too hard about what a potentially 20%

US fiscal deficit this year (to be monetized by the Fed) and further debt

monetisation of junk bonds (all shale oil producers at current oil prices)

could do to the intrinsic and future nominal value of the USD (knowing that it

constitutes 60%+ of world reserves). The value of the USD is an accident waiting

to happen and the moment to diversify is now, in our view, with some trading

required around core positions as an indispensable risk mitigating strategy if

this diagnostic fails to be wrong on timing. The same idea is still floating of

a big synthetic short position from EM countries that have borrowed in USD that

should prevent the dollar from weakening. It could be relieved two ways; by either

waiting for the USD to weaken or, if under too much pressure due to a rising

dollar, by defaulting on foreign debt which would extinguish this USD liability…and

the need to have to buy it back. Maybe this is the cure awaiting half the

nations asking for an IMF bailout. Perhaps it would be easier to pursue debt

relief (which Western countries will apply to themselves at the first place

with 0% debt funding and central bank monetisation) than ever higher SDR funded

IMF bailouts.

10Y US Treasuries rallied -8bps (-128bps) to 0,64%. 10Y Bunds dropped

-13bps (-29bps) to -0,47%. 10Y Italian BTPs underperformed rising 20bps (38bps)

to 1,79%, outperforming Bunds by -4bps.

US High Yield (HY) Average Spread over Treasuries dropped -80bps

(369bps) to 7,05%. US Investment Grade Average OAS dropped -18bps (102bps) to

2,03%. US High yields looked at rallying stocks for sentiment rather than the

cratering oil prices last week, supported by the ongoing high yield debt

monetisation efforts.

In European credit markets, EUR 5Y Senior Financial Spread climbed 7bps

(50bps) to 1,02%.

Gold dropped -0,8% (10,9%) while Silver sold off by -2,5% (-15,0%).

Major Gold Mines (GDX) rallied 3,4% (2,3%).

Goldman Sachs Commodity Index sold off by -4,6% (-41,4%).

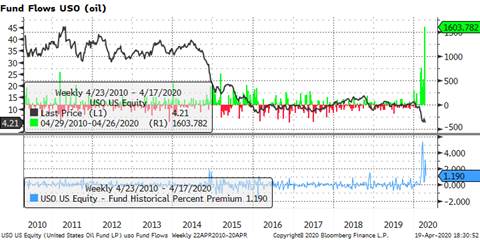

Oil fell sharply in particular WTI crude by -19,7% (-70,1%) despite last week end’s historical(cally ineffective)

OPEC++ deal to cut production by 9.7m bd. With demand destruction of USD29mn bd

and storage capacity reaching saturation, the odd man out in last week’s constructed

narrative remained tumbling oil prices which dropped a further 14% on Friday. With

the chart below in mind, one should perhaps imagine some invisible hand buying

millions of barrels of oil or associated ETF’s which saw the highest inflows ever

on… collapsing prices last week. Rolling oil futures would be equally

ineffective and costly (this would not matter if it could be effective) in an

oversupplied cash market (rolling the crude oil curve looks like jumping off a cliff), making intervening in oil prices a more challenging endeavour than stocking more 0 and 1’s on a custody account after

intervening in bonds and high yield ETF’s (and equity futures).

{kind=link}

Global demand for oil in April is forecast to drop by a record 29M bbl/day to levels not seen in a quarter century, the

International Energy Agency said, part of a set of dire estimates that

executive director F. Birol called

"staggering." "When we look back on 2020, we may well see it was

the worst year in the history of global oil markets, [and] April may well have

been the worst month," F. Birol said following

the IEA's release of its monthly oil report.

DBA dropped -0,9% (-17,6%).

Over the week end…

France will unveil within two weeks a plan to

progressively lift restrictions on travel and business that aimed to curb the

coronavirus epidemic, Prime Minister Edouard Philippe said on Sunday. “Our lives won’t be exactly the same as before,”

Philippe warned.

Marking an interesting U turn and switch of mind, D.

Trump has decided that a muscular U.S. currency is a good thing after all.

“The dollar is very strong,” he told a press conference on Friday. “And dollars

-- strong dollars are overall very good.”

Mhhh…

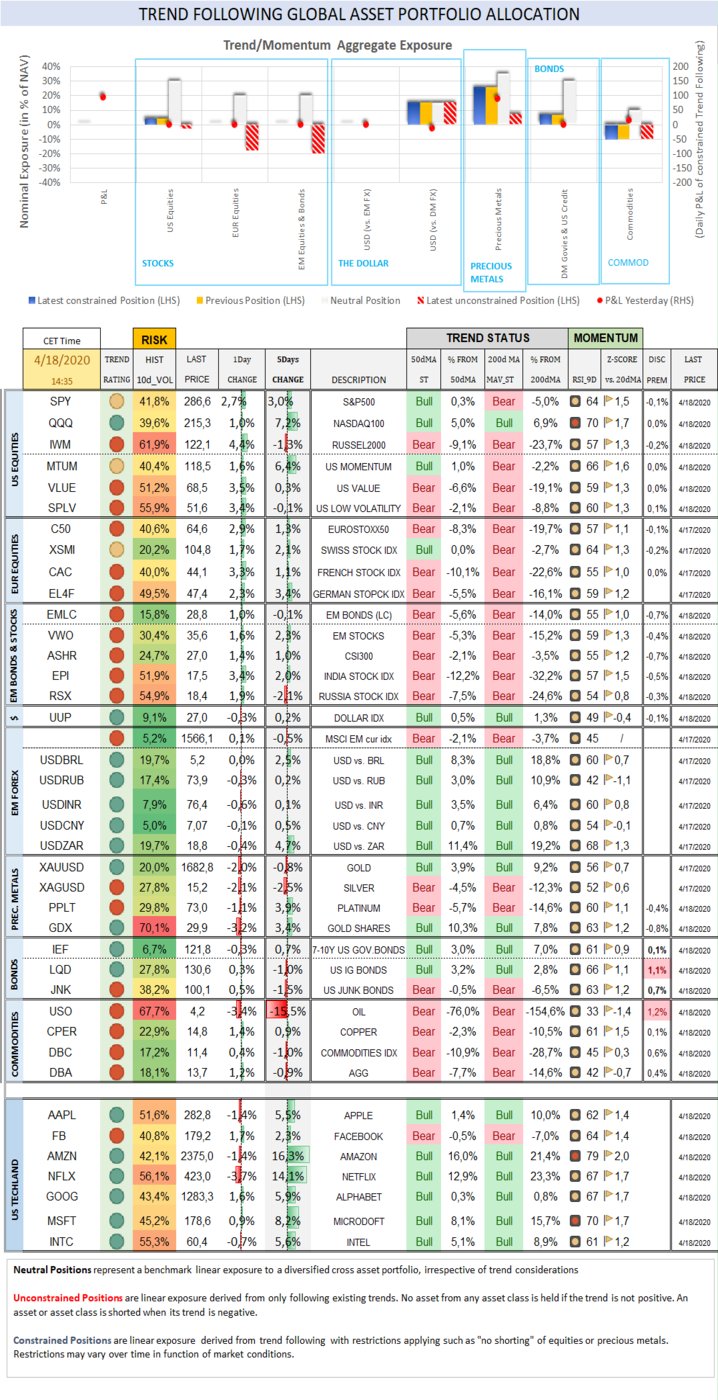

Trend Score Card

Click here for technical

annotations.

{kind=link}

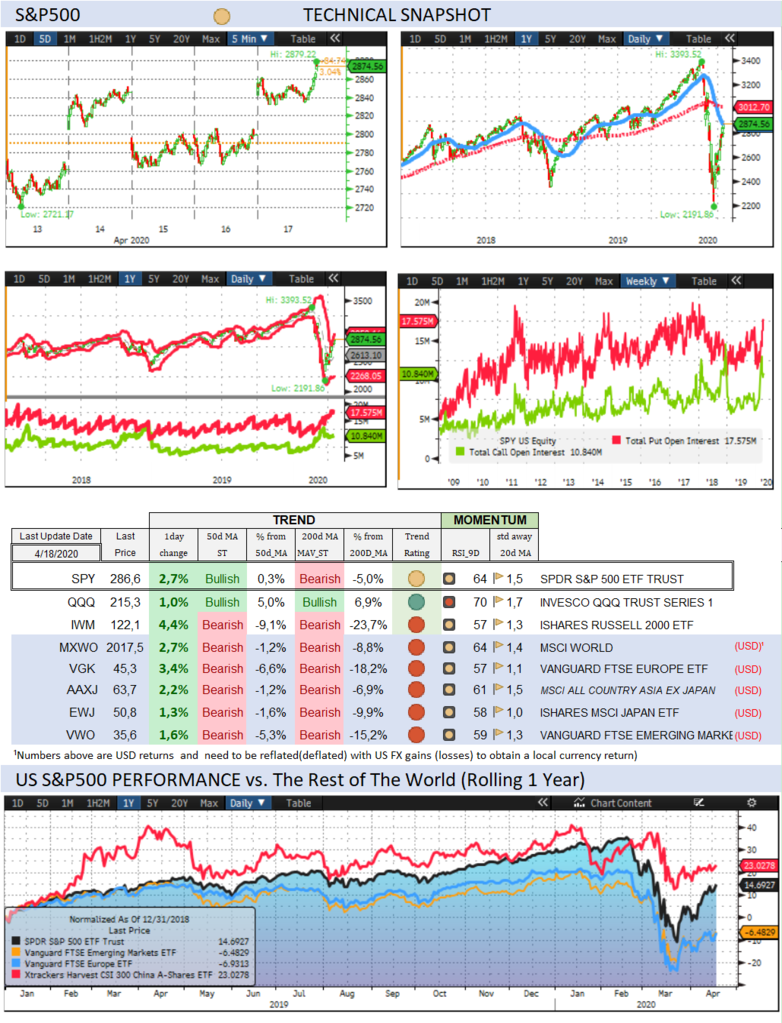

US

& International Equities

Check out US and International Stocks’ Technical

Trend Status.

{kind=link}

Sector

Trend & Momentum

Check equity sectors’ trend and performance …and when

they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their

trend, expected Fed rate moves and speculative positioning in 10-year Treasury

Futures.

{kind=link}

US

Recession Risk Radar

A comprehensive list of

economic indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs. G7

and EM counterparts.

{kind=link}

Precious Metals

Check out where precious

metals stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and futures

traders’ sentiment (non-commercials open positions).

{kind=link}

Check out how precious metals, the dollar and the

Stock market correlate with each other and speculative futures positioning

on Gold and the Dollar.

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and rule-based

trend following investment approach can serve as an effective portfolio

insurance technique.

To receive a Daily Trend

Status Update and round the clock market and economic instant notifications, join

the free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio Management and Advisory Services

BentinPartner GmbH is a

Swiss registered independent financial adviser. We offer four different

portfolio management mandates:

- The “Global

Strategic” (GS) mandate invests your portfolio according to an

optimized strategic benchmark. This allocation delivers the “beta” (or markets

related) performance of your portfolio while we seek to generate additional

“alpha” (“skills related) performance with tactical adjustments, using a

predefined maximum “value at risk” envelope. Most of the portfolio’s

performance is derived from the strategic Benchmark (beta).

- The “Global

Tactical” (GT) mandate

invests your portfolio without tracking a strategic asset allocation (or benchmark)

and pursues a “total” as opposed to “relative” return objective. With this

mandate, we seek to beat the best of “cash” or of the MSCI World Equity index,

applying mostly tactical considerations,

using a

predefined maximum “value at risk” envelope and targeting not to exceed a

predetermined overall portfolio volatility.

- The “Trend/Momentum”

(TM) mandate, builds a diversified “All Weather” investment portfolio and

applies a rule-based Trend/Momentum methodology to adjust this “trend neutral”

allocation. We track trends across asset classes on a daily basis and adjust

your portfolio in a semi automatic (there is always a pilot in the plane)

fashion applying trend changes signals.

- The “Currency Overlay” (CO) mandate

seeks to generate “alpha” applying a currency overlay with a limited leverage

(not exceeding 100% of NAV). You control the portfolio allocation (which can be

a pool of cash, stocks, bonds or gold) and we manage in overlay the FX exposure

of your portfolio, seeking to add a total FX return of 4% to 7%.

For more information on our risk management and

investment methodology, please check our web site.

We deliver transparent, professional, tailor-made,

and competitive asset management services, seeking to fulfill our fiduciary

duty at all times.

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the recipient's

sole use. Please do not forward it without prior authorization. It is not

intended as a recommendation, an offer or solicitation for the purchase or sale

of any security or underlying asset referenced herein or investment advice.

Investors should seek financial advice regarding the suitability of any investment

strategy based on their objectives, financial situation, investment horizon and

particular needs. This report does not include information tailored to any

particular investor. It has been prepared without any regard to the specific

investment objectives, financial situation or particular needs of any person

who receives this report. Accordingly, the opinions discussed in this

Report may not be suitable for all investors. You should not consider any of

the content in this report as legal, tax or financial advice. The data and analysis

contained herein are provided "as is" and without warranty of any

kind. BentinPartner llc, its

employees, or any third party shall not have any liability for any loss

sustained by anyone who has relied on the information contained in any

publication published by BentinPartner llc. The content and views expressed in this report

represents the opinions of Marc Bentin and should not be construed as

guarantee of performance with respect to any referenced sector. We remind you

that past performance is not necessarily indicative of future results. Although

BentinPartner llc believes

the information and content included in this report have been obtained from

sources considered reliable, no representation or warranty, express or

implied, is provided in relation to the accuracy, completeness or reliability

of such information. This Report is also not intended to be a complete

statement or summary of the industries, markets or developments referred to in

the Report.

#fx #forex #investing

#markets #riskmanagement #bankingindustry

#finances #money #traders #quants