Monday, January 03, 2022

Please

find below our latest Weekly Trend Report covering major asset

classes and currencies.

Have

a nice week ahead and good luck going into the new year.

Marc

Bentin

2021: An Exceptional Year …

Last year was exceptional and wild in many respects,

driven by the pandemic and Western deficit spending explosions, exceptional monetary

easing, historic (but relatively narrow with GAFA’s leading the way) stock

markets performance, soaring commodities and the somewhat associated inflation

running hotter and possibly not on a so “temporary basis”, all at the same

time.

·

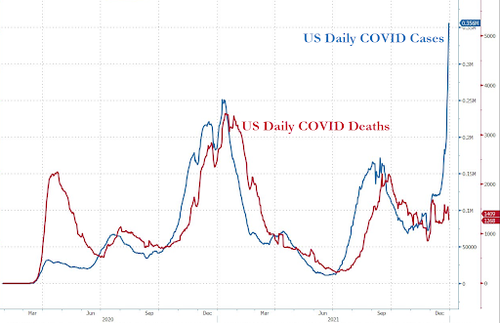

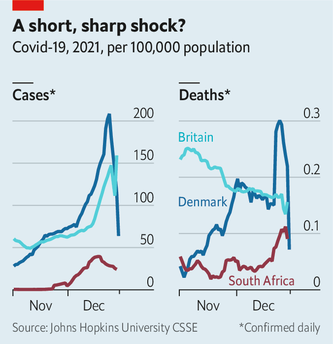

While there were

more deaths from covid in 2021 than in 2020 and while the late December surge

in daily cases exploded to 2mn globally, markets did not seem to want to care

too much, delivering a powerful late Christmas rally, seemingly reassured by the

Omicron Tsunami not translating into a concomitant acceleration in the number

of daily casualties (giving people some hopes (at least) that 2022 will be the year

when covid finally fades away. This has the potential to be the good news.

Source: Bloomberg

Source: The Economist

·

Taking the US

as a reference, 2021 US federal fiscal deficit reached USD2.77trn, bringing the

cumulated 2-year shortfall to an historic USD5.9trn, matching the total amount

of debt of accumulated since 2006 and leaving Treasuries/GDP ratio at 105%

(from 41% in Q42007). The same happened in Europe.

·

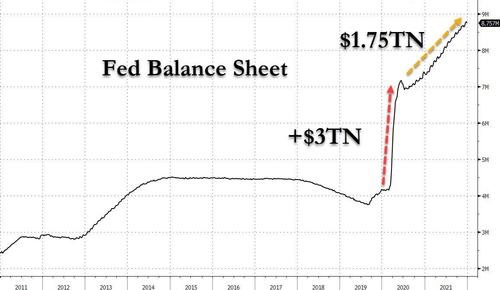

Debt

monetisation and ZIRP combined were the main policy choices to fund deficits

(holding the rationale of a temporary spike in inflation for most of the year) and

drive equity markets through 70 consecutive new highs late last year. Investors

were left with no other choices than piling on equities driven by TINA (“there is

no alternative”) and the most powerful magnet of all, FOMO (“fear of missing

out”). Investors (among them a new breed of investors and speculators trading “meme”

stocks on Robinhood for a living and who do not want to go back to work, at

least not at the same salary) bought more stocks (USD1trn) last year than over

the past 19 years combined while large corporations, already winning from the

pandemic (apple, msft…) continued to buy back shares

only too happy to substitute debt to equity as a source of cheap capital. Others

delisted for the same reason with leverage buyouts. Now that inflation, set to

rise on a confluence of factors (asset inflation, supply chain disruptions,

geopolitical tensions, accelerated and sometimes awkward Green transition policies)

has become more entrenched, with lasting second round effects (salary inflation,

rents, second hand cars etc…), there is a need to lift the foot from the

accelerator and push on the brake (should Omicron permit). It is going to be a delicate

balancing act with wide ranging implications (for bonds, stocks, FX and

precious metals).

Source: Bloomberg, ZH

Source Bloomberg, ZH

·

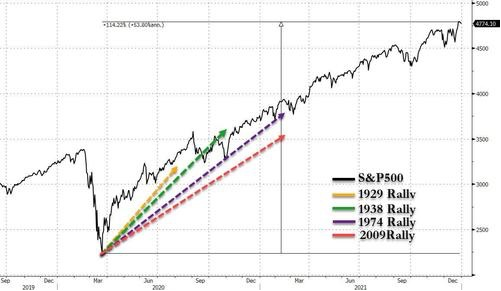

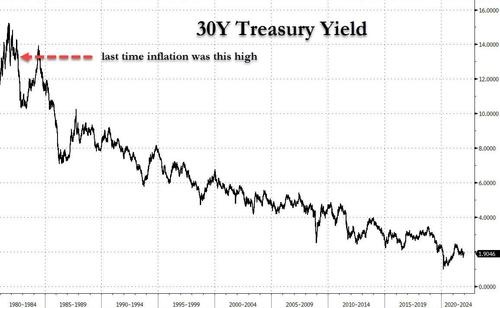

Despite solid

rising inflation and heavy fiscal issuance, bond yields dropped, real yields cratered

(also and primarily in Europe) and yield curves flattened because of debt

monetisation. If monetisation stops, other policy relays will be necessary to

keep the status quo. I do not quite see which one, baring a sharp stock market

correction or a resumption of QE (ultimately my guess). This seems to be the scenario

shared by F. Zulauf, a member of the Barron’s

roundtable for 20 years, (who correctly anticipated the 1987 and 2007 “corrections”.

He does not expect too much of a conflicted situation…until 2024, however. Hence

his relatively benign medium-term outlook for stocks for this year.

Bloomberg, Zerohedge

·

2022 was also

the year, despite a rocky last couple of months, when a broader range of investors

started to consider that cryptos were worth investing 2% or 3% of their assets

into, “just in case fiat money goes to hell”, to paraphrase T. Peterfly, the billionaire founder of Interactive Brokers. I

could not bite into the narrative that cryptos could constitute a valid long

term inflation hedge (the last 6 months of the year where inflation really took

off did not coincide with the best part of the year for the bulk of bitcoin’s 60%

YTD gain) but cryptos took gold lunch last year. They could remain well worth

investing the money we can afford to lose. The fact that cryptos can be negatively

correlated with everything one day and positively correlated with anything the

next also make cryptos a useful diversifier in portfolio construction (which is

a reason why many hedge funds also own some). The key risks for cryptos (besides

the interest of the underlying technology) are that unlike fiat currencies,

they are not backed by anything, not even the sovereign taxation power. They

are also intrinsically worthless (unlike gold and silver), highly volatile,

hence unfit as a means of payment for most, exposed to the risk of being

regulated away (as they are mostly in China, India, Russia and “officially” critically

viewed elsewhere). As outlined by Robert McCauley, in a recent FT article, bitcoin could also be viewed (beyond its huge ecologic footprint) as worse than a Madoff-style Ponzi Scheme and a mere “pump and dump” scheme. History will judge

but cryptos have certainly been a powerful “pump” scheme and a great way for

intermediaries (crypto exchanges) to make lots of money on the back of retail

investors who pay heavy transaction costs (much more than an stocks, bonds, FX)

and face heavy roll down costs for those owning cryptos via futures backed ETF’s.

Some of the

key risks ahead?

Making forecasts is a difficult exercise but one that can hardly be

avoided at this time of the year. We can at least identify the major risks.

-

High and

rising inflation rates (we will cover the subject in some more details tomorrow

…and expectations. This is a key risk because a little bit of inflation always benefits

everybody but too much of it for too long invariably becomes toxic economically,

fiscally, financially, socially and ultimately politically)

-

the ways that

will be deployed (or not) to contain inflation (Fed tapering and tightening)

will define the favourable or unfavourable outcome.

-

geopolitical tensions.

The risks of things going “mad” in either Taiwan or Ukraine are almost

impossible to hedge and will remain as hard left tail risks to the global

outlook. Cool heads will most likely prevail.

But debates and conflicting economic and geopolitical interests will remain heated

with elevated military tensions and the risks of accidents not inexistent.

-

Social tensions

derived from the “all round” asset inflation coupled to rising food and energy inflation

if not contained could increase the social divide with risks of mounting populism.

Some are arguing that we are witnessing the first innings of Orwelian crackdown on civil liberties by governments everywhere.

But I am not going there… and I hope the end of the pandemic situation will bring

back our lives more or less where they were before

(NB: most YTD scores were reset over the week end)

Over the past week, the S&P500 gained 0,9% (26.9%

YTD) while the Nasdaq100 gained 0,2% (0,0% YTD). The US small cap index gained

0,2% (0,0% YTD). Biotech dropped -2.3% (-3.8%YTD).

Cboe Volatility Index dropped -4,1% (0,0% YTD) to

17,22.

The Eurostoxx50 gained 0,7% (0,0%), underperforming

the S&P500 by-0,2%.

Diversified EM equities (VWO) gained 0,6% (0,0%),

underperforming the S&P500 by-0,4%.

The Dollar DXY Index (UUP) measuring the USD performance vs. other G7 currencies

dropped -0,4% (0,0%, Z-score -2,2) while the MSCI EM currency index

(measuring the performance of EM currencies vs. the USD) gained 0,0% (0,0%).

10Y US Treasuries dropped 2bps (60bps) to 1,51%.

10Y Bunds climbed 7bps (39bps) to -0,18%. 10Y Italian BTPs underperformed

rising 6bps (63bps) to 1,17%, outperforming Bunds by 0bps.

US High Yield (HY) Average Spread over Treasuries

climbed 0bps (-77bps) to 2,83%. US Investment Grade Average OAS dropped -3bps

(-2bps) to 1,00%.

In European credit markets, EUR 5Y Senior Financial

Spread dropped -1bps (0bps) to 0,55%.

Gold

gained 1,0% (0,0%, Z-score 2,2) while Silver gained 1,3% (0,0%). Major Gold Mines

(GDX) rallied 2,3% (0,0%).

Goldman Sachs Commodity Index dropped -0,9% (0,0%).

WTI Crude gained 1,9% (55,0%).

Overnight in Asia,,,

Ø S&P500 +13points; Nikkei -0.4%; CSI300 +0.4%

Ø Oil edged higher as Libyan supply

tightened ahead of an OPEC+ meeting on Tuesday to discuss production policy for

February.

Ø U.S. equity futures gained, while Asian stocks were

mixed. China Evergrande Group shares were suspended in Hong Kong.

10 Days In Charts…

{kind=link}

{kind=link}

{kind=link}

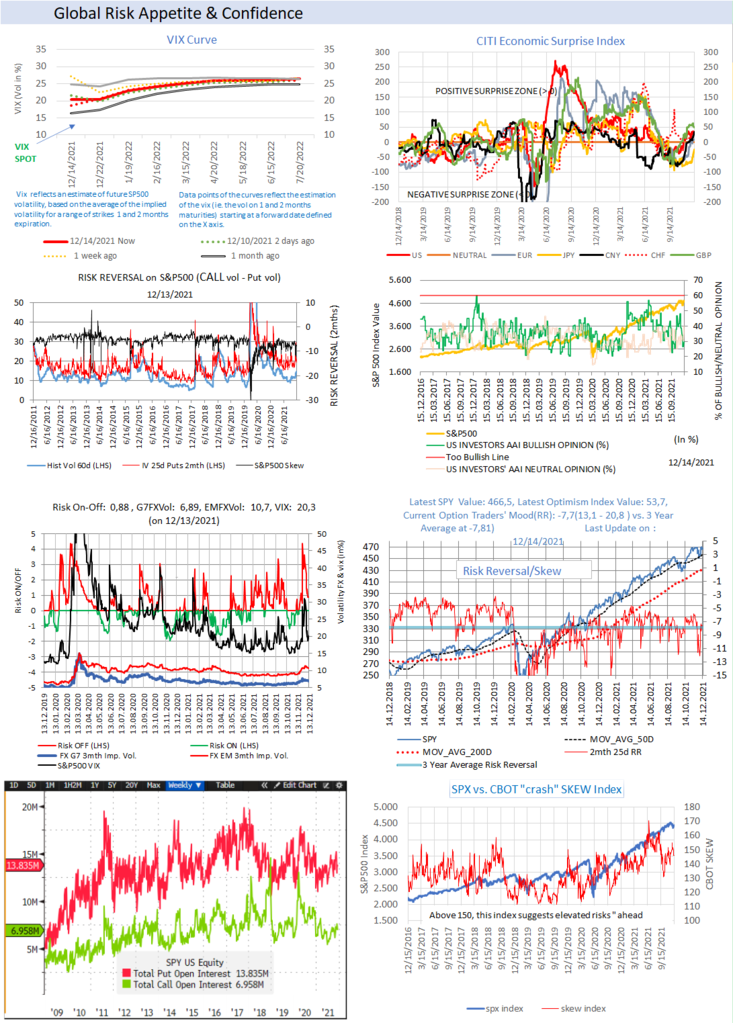

Global

Risk Appetite & Confidence

Check out different gauges of Risk Appetite .

{kind=link}

Check China … (Stock

Indices, CNY…and Evergrande)

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and rule-based trend following investment

approach can serve as an effective portfolio insurance technique.

To receive a Daily Trend Status Update and round the

clock market and economic instant notifications, join the free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio

Management and Advisory Services

Zero and sub-zero

interest rates are here to stay. As a private individual, a pension fund or a

foundation, we all share the same challenge!

To see how we can help

you secure your financial independence over the long term, meet your

obligations and mitigate tail risks,

Check our Pitch

and our FAQ’s.

BentinPartner GmbH is

an registered Swiss Financial Adviser

delivering professional portfolio management and research.

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc. This

communication is provided for information purposes only and for the recipient's

sole use. Please do not forward it without prior authorization. It is not

intended as a recommendation, an offer or solicitation for the purchase or sale

of any security or underlying asset referenced herein or investment advice.

Investors should seek financial advice regarding the suitability of any

investment strategy based on their objectives, financial situation, investment

horizon and particular needs. This report does not include information tailored

to any particular investor. It has been prepared without any regard to the

specific investment objectives, financial situation or particular needs of any

person who receives this report. Accordingly, the opinions discussed in

this Report may not be suitable for all investors. You should not consider any

of the content in this report as legal, tax or financial advice. The data and

analysis contained herein are provided "as is" and without warranty

of any kind. BentinPartner llc, its employees, or any

third party shall not have any liability for any loss sustained by anyone who

has relied on the information contained in any publication published by BentinPartner

llc. The content and views expressed in this report

represents the opinions of Marc Bentin and should not be construed as

guarantee of performance with respect to any referenced sector. We remind you

that past performance is not necessarily indicative of future

results. Although BentinPartner llc believes

the information and content included in this report have been

obtained from sources considered reliable, no representation or

warranty, express or implied, is provided in relation to the accuracy,

completeness or reliability of such information. This Report is also not

intended to be a complete statement

or summary of the industries, markets or developments referred to in the

Report.

#fx #forex #investing #markets #riskmanagement #bankingindustry

#finances #money #traders #quants