Sunday, December 08, 2019

Please

find below our latest Weekly Trend Update Report covering major

asset classes and currencies.

Have

a nice week end.

Marc

Bentin

{kind=link}

{kind=link}

{kind=link}

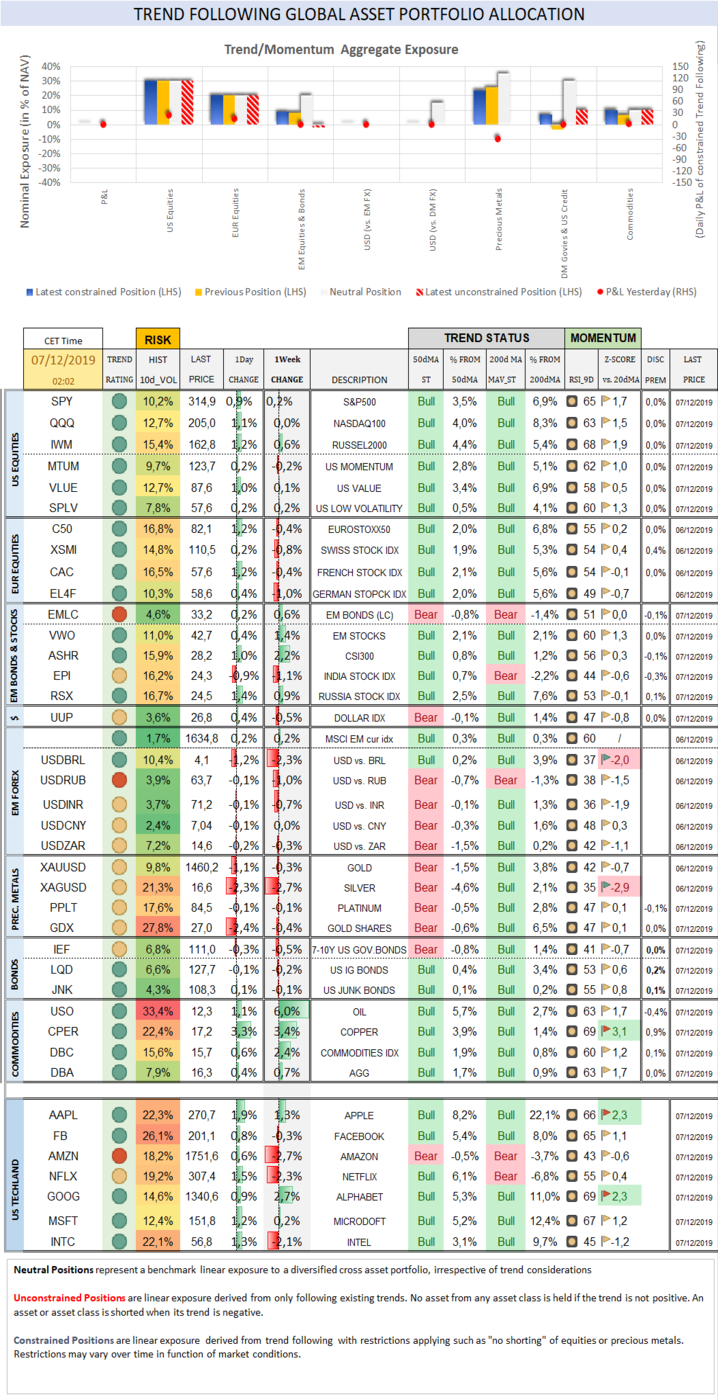

Trend

Status Update

The second punch came last week with D. Trump declaring that he was

willing to wait until after next year’s presidential election to strike a

limited trade deal with China, casting doubt on expectations for the upcoming

Phase I of the US /China trade deal supposed to prevent the escalation of new

tariffs on December 15th. He

added perhaps disingenuously that he was not there to support stock prices…The

following day, as a relief to stock markets, he inferred the exact opposite that the US and China were

moving closer to agreeing on the amount of tariffs that would be rolled back in

a phase-one trade deal despite tensions over Hong Kong. It was said that D.

Trump’s comments on Tuesday downplaying the urgency of a deal shouldn’t have

been understood to mean that talks were stalling as he was speaking off the

cuff… The stock market subsequently rallied, recovering all it had lost in the

first two days of the week. The Chinese commerce ministry did say that tariffs

must be cut if China and the United States are to reach an interim agreement on

trade, sticking to a stance that some US tariffs must be rolled back for a

phase One deal but the markets and the week ended on a strong note with

sentiment further jolted on Friday by

the better than expected US job report, itself comforted by US shoppers spending

$9.4bn online on Cyber Monday, up almost 20% from a year ago. This outweighed evidence of a further slowing in US

manufacturing for which D. Trump blamed the Fed (“Manufacturers are being held

back by the strong Dollar, which is being propped up by the ridiculous policies

of the Federal Reserve - Which has called interest rates and quantitative

tightening wrong from the first days of Jay Powell!”).

Beyond the V shape recovery of stocks which remain in “Fomo & Tina” mode, the other “take away” from last week was the Federal Reserve saying it was considering introducing a rule that would let inflation

run above its 2% target, a potentially significant shift in its interest rate

policy which basically equates the central bank to consider a promise that when

it misses its inflation target, it will then temporarily raise that target, to

make up for lost inflation… This may translate into the Fed likely cutting one

more time, probably not this year (after Friday’s job report, it would be odd)

but next year and even more likely not reversing course at the first sign of the

battle against deflation being won. If the Fed adopts this so-called ‘make-up

strategy’, it would mark the biggest shift in interest rate policy since it

began to target 2% inflation in 2012, the WSJ reported. Last Friday’s job

numbers also showed tensions building in employment costs and commodities are

doing a little bit more than stirring in the water as well which might challenge

bond yields next year. Tariffs, deglobalisation, mounting wage pressures and

rising commodities are not a recipe for continued deflation.

At stock markets aim at breaking the ceiling, Morgan Stanley published a

study last week arguing that more than a third of S&P 500 companies posted

a year-over-year decline in earnings in 2019 which was last seen in 2009, 2008

and 2002, when the broader economy and the stock market fell. This time (with

near zero interest rates and central banks balance sheet expansion) will be

different and we can only assume that multiple expansion will be the only way

forward to justify higher stock prices. For what it is worth, analysts are also

slashing projections for Q4 earnings at a fast pace, making it more likely that

a profit recession will hit Corporate America for the first time in four years with

a drop of almost 1% from a year ago following a 1.3% decline for the previous

quarter.

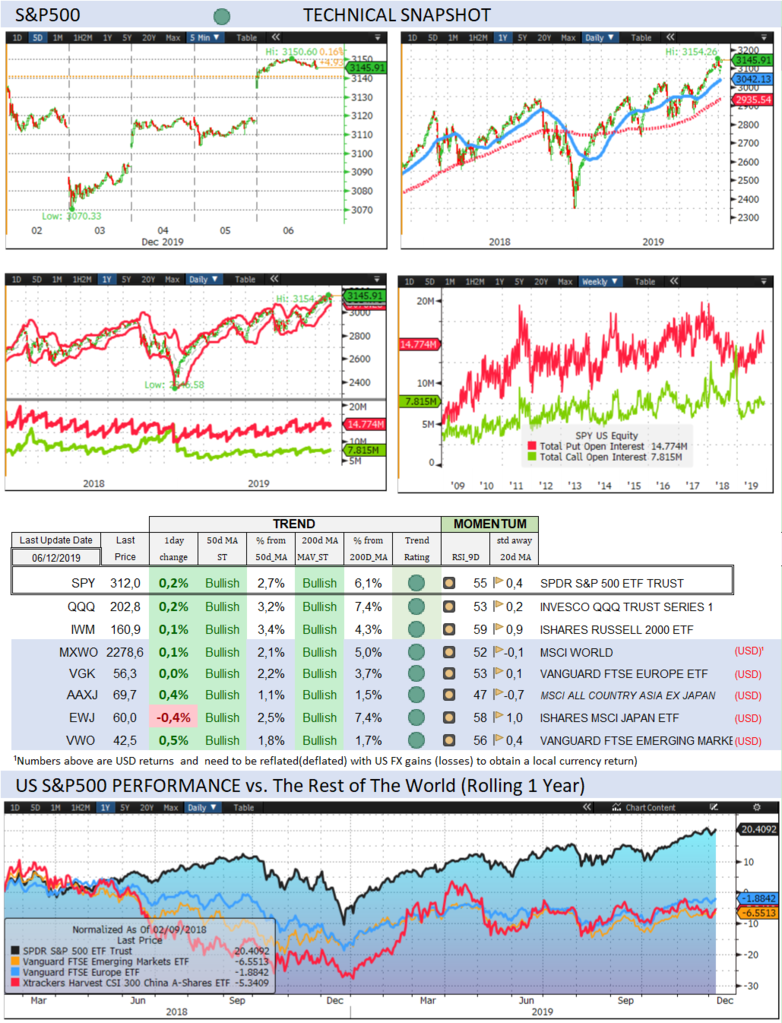

Over the past week, the S&P500 added 0,2% (26,0% YTD) while the

Nasdaq100 closed unchanged on the week (32,9% YTD). The US small cap index

gained 0,6% (21,6% YTD). In terms of sectorial performance, a shift occurred

again favouring tech and growth over value with Apple and Google both ending

the week in breakout mode. The Eurostoxx50 dropped -0,4% (25,7%),

underperforming the S&P500 by-0,6%. XLF (FINANCIAL SELECT SECTOR SPDR) gained 0,7% (27,5%,

Z-score 2,3) despite Moddy’s downgrading the sector outlook. Diversified

EM equities (VWO) gained 1,4% (11,9%), outperforming the S&P500 by 1,2%. CSI300 Chinese equity index (ASHR) rallied 2,2%

(28,5%). Indian shares (EPI) dropped -1,1% (-2,1%). Russian shares (RSX) gained

0,9% (30,5%). EWJ (ISHARES MSCI JAPAN ETF) responded favourably to the stimulus package,

rallying 2,1% (19,7%, Z-score 2,9).

The Dollar DXY Index (UUP) dropped on the week by -0,5% (5,2%) while the

MSCI EM currency index (measuring the performance of EM currencies vs. the USD)

gained 0,2% (1,2%). EM currencies were mostly stronger. USDBRL

sold off by -2,3% (6,6%, Z-score -2,0). USDRUB dropped -1,0% (-8,2%). USDMXN dropped -1,1%

(-1,8%). USDINR dropped -0,7% (2,1%). USDCNY was unchanged (2,3%) while USDZAR

dropped -0,3% (1,9%). The performance of the euro was mixed; EURUSD gained 0,4% (-3,5%). EURCHF dropped -0,6%

(-2,7%). EURJPY dropped -0,4% (-4,5%) and EURGBP dropped -1,2% (-6,4%, Z-score -2,6) as

opinion polls showed the UK Prime Minister B. Johnson still holding 10 points

lead for next week’s elections. Japan’s Prime Minister Abe announced stimulus

measures to support growth in an economy affected by an export slump, natural

disasters and a recent sales tax increase. The total stimulus package amounted

to around 26 trillion yen ($239bn) spread over the coming years. The stimulus could

boost growth by about 1.4%, the draft document said, driving Japanese stocks to

the top of the z-score report on Friday, also supporting the yen despite a

global “risk on” wave. The euro remains the currency that nobody wants to own

because it loses money standing still but it is interesting to note that the

euro zone is emerging as the new global provider of liquidity to the

international financial system, slowly replacing the dollar as more and more

companies want to issue debt in euros. Our outlook remains bearish for the

dollar going into next year (including against the euro) but it might not be worth

trading just yet, as opposed to higher yielding non-USD alternatives from the EM

space.

10Y US Treasuries underperformed with yields rising 6bps (-85bps) to

1,84%. 10Y Bunds climbed 7bps (-53bps) to -0,29%. 10Y Italian BTPs

underperformed rising 12bps (-139bps) to 1,35%. US High Yield (HY) Average

Spread over Treasuries dropped -10bps (-166bps) to 3,60%. US High Yield (HY) Caa Average Spread over Treasuries dropped -35bps (-45bps)

to 9,44% with the accumulated underperformance of the past few weeks still

striking and showing a lasting differentiation and distanciation

of investors away from the worse credits. US Investment Grade Average OAS dropped -4bps (-61bps, Z-score -2,5) to

1,11%. In European credit markets, EUR 5Y Senior Financial Spread

dropped -1bp (-54bps) to 0,56%.

Gold dropped -0,3% (13,9%) while Silver shed -2,7% (7,0%, Z-score -2,9). Major Gold

Mines (GDX) dropped -0,4% (27,9%). Bitcoin shed -3,1% (103,3%).

The right way to gauge the rationale for holding gold is as a hedge

against inflation, a dollar reversal and occasional equity market corrections. In

the current environment, we view gold as a good substitute to cash and bonds that

could be held in unusually large proportions, coupled with equally large long equity

markets exposure as the ongoing rally is an artificial liquidity pushed rally

that will continue to erode the value of money (or their bond proxies) over

time.

Goldman Sachs Commodity Index is playing catch up for the year and

rallied 3,3% on the week (11,5%). WTI Crude also rallied strongly by 7,3%

(30,4%), supported by OPEC’s decision to further curtail supply late last week. CPER

rallied 3,4% (4,8%, Z-score 3,1) as reflation trade ideas resurfaced. More evidence

of growing cooperation between China and Russia crystallized last week with the

inauguration of an 1,800-mile pipeline delivering Russian natural gas to China.

The $55bn pipeline is a feat of infrastructure and political engineering. It is

also Russia’s most significant energy project since the collapse of the Soviet

Union. The Siberia pipeline is also a seal of physical bond strengthening

between China and Russia.

Next week…

Next week will bring its dose of things to cheer or lament about…

German export and import data will be published on Monday (expected to

decline by 0.3% MoM). The UK GDP and German ZEW survey come on Tuesday. The

outcome of the Fed meeting comes on Wednesday along with the US CPI.

ECB President C. Lagarde will chair her first policy meeting on

Thursday.

The UK elections will also be held on Thursday.

US November retail sales come on Friday (+0.4% MoM expected).

Towards the end of the week, D. Trump is also likely to take a decision to

slap (or not) 15% additional tariffs on USD160bn Chinese imports.

Trend Score Card

Click here for technical annotations.

{kind=link}

{kind=link}

US

& International Equities

Check out US and International Stocks’ Technical

Trend Status.

{kind=link}

Sector

Trend & Momentum (revised)

Check out equity sectors’ trend and performance

…and when they break out!

{kind=link}

Fixed

Income

Check out 10Y US Treasury and Bund yields, their

trend, expected Fed rate moves and speculative positioning in 10-year Treasury

Futures.

{kind=link}

US Recession

Risk Radar

A comprehensive list of

economic indicators to compare the current situation with previous recessions.

{kind=link}

The

Dollar

Check out where the Dollar stands Trendwise and Breakoutwise vs.

G7 and EM counterparts.

{kind=link}

Precious Metals

Check out where precious

metals stand Trendwise

and Breakoutwise.

Get a sense of options (cumulative open interests on calls and puts) and

futures traders’ sentiment (non-commercials open positions).

{kind=link}

Why Trend Following Matters and How It Can Help

You?

The last months of 2018

illustrated how fast and furious markets can fall. Trend following offers

guidance as to when to join and when to leave an asset class with changing

trend characteristics. A disciplined and rule-based trend following investment

approach can serve as an effective portfolio insurance technique. Our purpose,

beyond tracking economic, political and monetary developments is to assist

readers investing in global markets with a keen focus on trend formation

covering all important asset classes.

To receive a Daily Trend

Status Update and much more, join a

free trial of our premium research.

To learn more about our premium research:

https://www.bentinpartners.ch/research

Feel free to join our free trial and choose your

delivery preferences:

https://www.bentinpartners.ch/subscribe

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc.

This communication is provided for information purposes only and for the

recipient's sole use. Please do not forward it without prior authorization. It

is not intended as a recommendation, an offer or solicitation for the purchase

or sale of any security or underlying asset referenced herein or investment

advice. Investors should seek financial advice regarding the suitability of any

investment strategy based on their objectives, financial situation, investment

horizon and particular needs. This report does not include information tailored

to any particular investor. It has been prepared without any regard to the

specific investment objectives, financial situation or particular needs of any

person who receives this report. Accordingly, the opinions discussed in

this Report may not be suitable for all investors. You should not consider any

of the content in this report as legal, tax or financial advice. The data and

analysis contained herein are provided "as is" and without warranty

of any kind. BentinPartner llc,

its employees, or any third party shall not have any liability for any loss

sustained by anyone who has relied on the information contained in any

publication published by BentinPartner llc. The content and views expressed in this report

represents the opinions of Marc Bentin and should not be construed as

guarantee of performance with respect to any referenced sector. We remind you

that past performance is not necessarily indicative of future

results. Although BentinPartner llc believes the information and content included in

this report have been obtained from sources considered reliable,

no representation or warranty, express or implied, is provided in relation to

the accuracy, completeness or reliability of such information. This Report is

also not intended to be a complete statement or summary of the industries,

markets or developments referred to in the Report.

#fx #forex

#investing #markets #riskmanagement #bankingindustry #finances #money #traders #quants